মসৃণ জেড-স্কোর ক্রসওভারের উপর ভিত্তি করে মোমেন্টাম অপ্টিমাইজেশন মূল্য পরিসংখ্যান ট্রেডিং কৌশল

সংক্ষিপ্ত বিবরণ

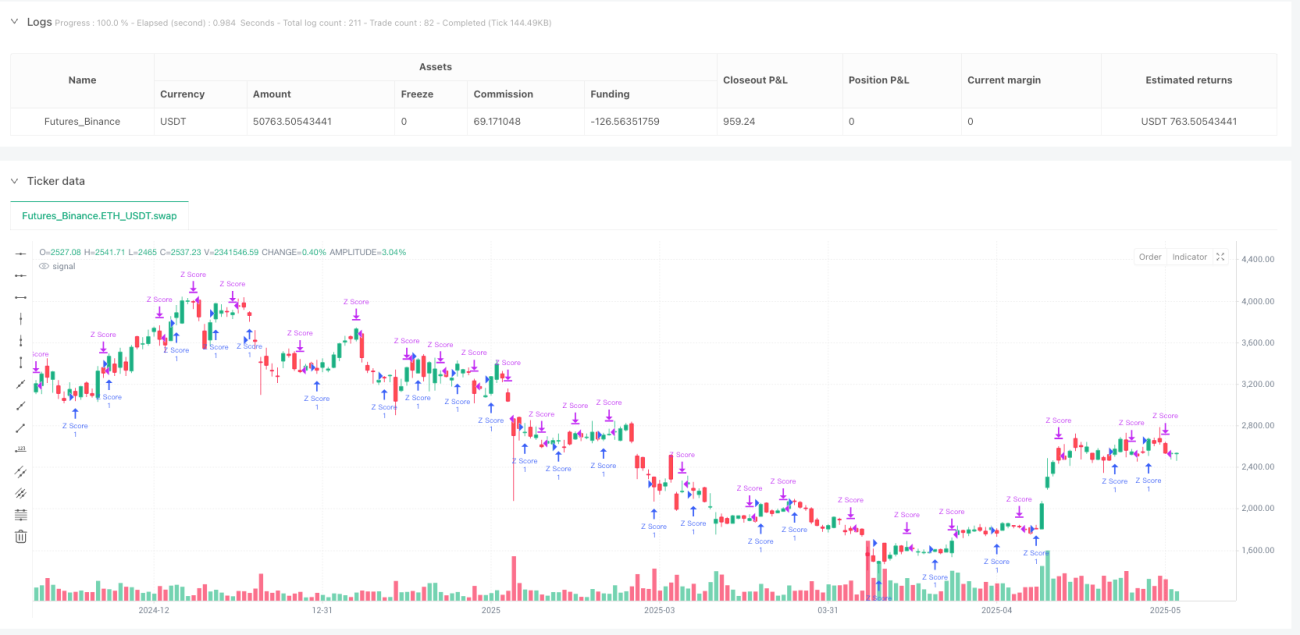

এই কৌশলটি জেড-স্কোর (Z-Score) নামক একটি পরিসংখ্যানগত ধারণার উপর ভিত্তি করে তৈরি, যা এর স্থানীয় গড় মূল্যের সাপেক্ষে মূল্যের পরিসংখ্যানগত বিচ্যুতি চিহ্নিত করতে ব্যবহৃত হয়। কৌশলটি ক্লোজিং প্রাইসের জেড-স্কোর গণনা করে এবং তারপর জেড-স্কোর মানকে মসৃণ করতে স্বল্পমেয়াদী এবং দীর্ঘমেয়াদী মুভিং এভারেজ প্রয়োগ করে। যখন স্বল্পমেয়াদী মসৃণ জেড-স্কোর দীর্ঘমেয়াদী মসৃণ জেড-স্কোরকে ঊর্ধ্বক্রমন করে, তখন লং এন্ট্রি সিগন্যাল তৈরি হয় এবং যখন স্বল্পমেয়াদী মসৃণ জেড-স্কোর দীর্ঘমেয়াদী মসৃণ জেড-স্কোরকে অধঃক্রমন করে, তখন পজিশন ক্লোজ করার সিগন্যাল তৈরি হয়। কৌশলটিতে নয়েজ ট্রেডিং কমাতে সিগন্যাল ইন্টারভাল নিয়ন্ত্রণ এবং মোমেন্টাম-ভিত্তিক ক্যান্ডেল ফিল্টার অন্তর্ভুক্ত রয়েছে।

কৌশলের নীতি

এই কৌশলের মূল কেন্দ্রবিন্দু হলো জেড-স্কোরের গণনা এবং প্রয়োগ। জেড-স্কোর একটি পরিসংখ্যানগত পরিমাপ যা একটি ডেটা পয়েন্ট নমুনা গড় থেকে কতটা বিচ্যুত, তা স্ট্যান্ডার্ড ডেভিয়েশনের এককে পরিমাপ করে। এই কৌশলে, জেড-স্কোর গণনার সূত্রটি হলো:

Z = (ক্লোজিং প্রাইস - SMA(ক্লোজিং প্রাইস, N)) / STDEV(ক্লোজিং প্রাইস, N)

এখানে N হলো ব্যবহারকারীর সংজ্ঞায়িত বেস পিরিয়ড।

কৌশলটির সম্পাদনের ধারা নিম্নরূপ:

- ক্লোজিং প্রাইসের মূল জেড-স্কোর গণনা করুন

- মূল জেড-স্কোরে স্বল্পমেয়াদী মসৃণকরণ (SMA) প্রয়োগ করুন

- মূল জেড-স্কোরে দীর্ঘমেয়াদী মসৃণকরণ (SMA) প্রয়োগ করুন

- যখন স্বল্পমেয়াদী মসৃণ জেড-স্কোর দীর্ঘমেয়াদী মসৃণ জেড-স্কোরকে ঊর্ধ্বক্রমন করে এবং অতিরিক্ত শর্ত পূরণ করে, তখন লং পজিশন খুলুন

- যখন স্বল্পমেয়াদী মসৃণ জেড-স্কোর দীর্ঘমেয়াদী মসৃণ জেড-স্কোরকে অধঃক্রমন করে এবং অতিরিক্ত শর্ত পূরণ করে, তখন পজিশন বন্ধ করুন

অতিরিক্ত শর্তগুলির মধ্যে রয়েছে:

- সিগন্যাল ব্যবধান: একই ধরনের দুটি সিগন্যালের (এন্ট্রি বা এক্সিট) মধ্যে ন্যূনতম সংখ্যক ক্যান্ডেলের ব্যবধান থাকতে হবে

- মোমেন্টাম ফিল্টার: যখন পরপর তিন বা ততোধিক ঊর্ধ্বমুখী ক্যান্ডেল থাকে, তখন এন্ট্রি নিষিদ্ধ; যখন পরপর তিন বা ততোধিক অধঃমুখী ক্যান্ডেল থাকে, তখন এক্সিট নিষিদ্ধ

কৌশলের সুবিধা

- পরিসংখ্যানগত ভিত্তি: জেড-স্কোর একটি পরিণত পরিসংখ্যানগত টুল, যা কার্যকরভাবে মূল্যের তার গড় থেকে বিচ্যুতির মাত্রা চিহ্নিত করতে পারে এবং দামের গড়ে ফিরে আসার সুযোগ ধরা জন্য উপযুক্ত।

- মসৃণকরণ প্রক্রিয়াকরণ: মূল জেড-স্কোরে স্বল্পমেয়াদী এবং দীর্ঘমেয়াদী মসৃণকরণ প্রয়োগ করে, নয়েজ কমিয়ে সিগন্যালের গুণমান উন্নত করে।

- সিগন্যাল ব্যবধান নিয়ন্ত্রণ: ন্যূনতম সিগন্যাল ব্যবধান নির্ধারণ করে, অতিরিক্ত ট্রেডিং এবং পুনরাবৃত্তি সিগন্যাল কার্যকরভাবে হ্রাস করে।

- মোমেন্টাম ফিল্টার: শক্তিশালী ট্রেন্ডের সময় কাউন্টার-ট্রেন্ড ট্রেডিং নিষিদ্ধ করে, শক্তিশালী বাজারের পরিস্থিতিতে অপ্রয়োজনীয় ক্ষতি এড়ায়।

- সরলতা: কৌশলটি শুধুমাত্র ক্লোজিং প্রাইস ডেটা ব্যবহার করে, জটিল ইন্ডিকেটর সমন্বয়ের উপর নির্ভর করে না, বুঝতে এবং বাস্তবায়ন করতে সহজ।

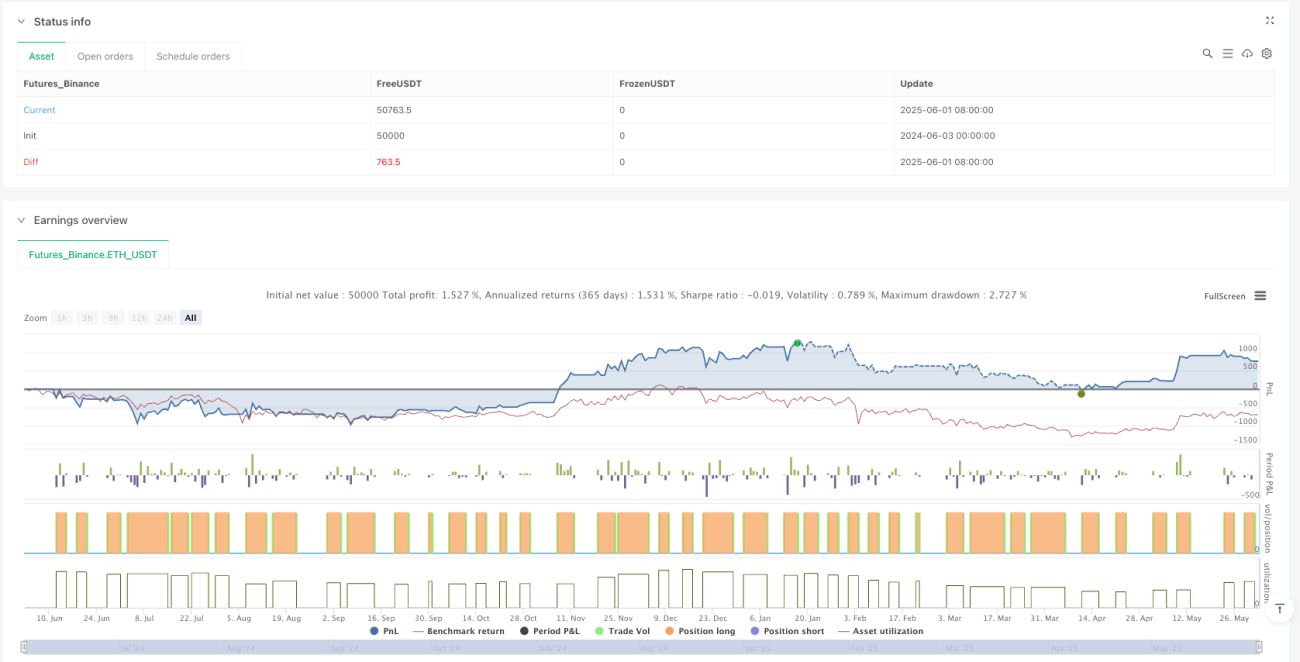

- রিয়েল-টাইম লাভ-ক্ষতি পর্যবেক্ষণ: রিয়েল-টাইমে অপ্রাপ্ত লাভ-ক্ষতি প্রদর্শনের জন্য একটি টেবিল অন্তর্ভুক্ত রয়েছে, যা ট্রেডারদের পজিশনের অবস্থা পর্যবেক্ষণ করতে সহায়তা করে।

- প্যারামিটার নমনীয়তা: ব্যবহারকারীরা বিভিন্ন বাজার এবং টাইমফ্রেম অনুসারে জেড-স্কোরের বেস পিরিয়ড এবং মসৃণকরণ প্যারামিটার সামঞ্জস্য করতে পারেন, অভিযোজন ক্ষমতা বৃদ্ধি করে।

কৌশলের ঝুঁকি

- পরিসংখ্যানগত অনুমানের ঝুঁকি: জেড-স্কোর ধরে নেয় যে মূল্য বন্টন প্রায় স্বাভাবিক বন্টন অনুসরণ করে, অ-স্বাভাবিক বন্টন বাজারের পরিবেশে খারাপ পারফর্ম করতে পারে।

- প্যারামিটার সংবেদনশীলতা: জেড-স্কোরের বেস পিরিয়ড এবং মসৃণকরণ প্যারামিটারের নির্বাচন কৌশলের কর্মক্ষমতার উপর উল্লেখযোগ্য প্রভাব ফেলে, ভুল প্যারামিটার নির্বাচন ওভারফিটিং বা সিগন্যাল বিলম্বের কারণ হতে পারে।

- একক ফ্যাক্টরের সীমাবদ্ধতা: কৌশলটি শুধুমাত্র জেড-স্কোর ক্রসওভারের উপর ভিত্তি করে সিগন্যাল তৈরি করে, অন্যান্য নিশ্চিতকরণ ইন্ডিকেটরের অভাব রয়েছে, যা মিথ্যা সিগন্যালের কারণ হতে পারে।

- বাজার পরিবেশের উপর নির্ভরশীলতা: শক্তিশালী ট্রেন্ড বাজারে, গড়ে ফিরে আসার উপর ভিত্তি করে কৌশলটি ধারাবাহিকভাবে ভুল সিগন্যাল তৈরি করতে পারে।

- সিগন্যাল বিলম্ব: মুভিং এভারেজ মসৃণকরণ ব্যবহারের কারণে, সিগন্যালে বিলম্ব দেখা দিতে পারে, যা সেরা এন্ট্রি বা এক্সিট পয়েন্ট মিস করতে পারে।

সমাধানের উপায়:

- বিভিন্ন বাজার পরিবেশে ব্যাকটেস্ট করে সর্বোত্তম প্যারামিটার কম্বিনেশন খুঁজে বের করুন

- প্রবণতা ফিল্টার যুক্ত করুন, শক্তিশালী ট্রেন্ড বাজারে ট্রেডিং সংখ্যা কমিয়ে বা নিষ্ক্রিয় করুন

- অতিরিক্ত নিশ্চিতকরণ ইন্ডিকেটর যোগ করুন, যেমন ভলিউম বিশ্লেষণ বা অন্যান্য টেকনিক্যাল ইন্ডিকেটর

- অভিযোজিত প্যারামিটার ব্যবহার করার কথা বিবেচনা করুন, বাজারের অস্থিরতা অনুসারে স্বয়ংক্রিয়ভাবে জেড-স্কোর প্যারামিটার সামঞ্জস্য করুন

অপ্টিমাইজেশনের দিকনির্দেশনা

- প্রবণতা সনাক্তকরণ ইন্টিগ্রেশন: একটি প্রবণতা সনাক্তকরণ উপাদান যোগ করুন, স্পষ্ট প্রবণতার দিকের বাজারে কৌশলের আচরণ সামঞ্জস্য করুন। এটি দীর্ঘমেয়াদী মুভিং এভারেজ বা ADX ইন্ডিকেটরের মাধ্যমে বাস্তবায়ন করা যেতে পারে, শক্তিশালী ট্রেন্ডে ভুল গড়ে ফিরে আসার সিগন্যাল এড়াতে।

- অস্থিরতা সমন্বয়: জেড-স্কোর প্যারামিটারের অভিযোজিত সমন্বয় বাস্তবায়ন করুন, বাজারের অস্থিরতা অনুসারে স্বয়ংক্রিয়ভাবে বেস পিরিয়ড এবং মসৃণকরণ প্যারামিটার অপ্টিমাইজ করুন। এটি বিভিন্ন বাজার পরিবেশে কৌশলের দৃঢ়তা (robustness) উন্নত করবে।

- মাল্টিপল টাইমফ্রেম বিশ্লেষণ: নিশ্চিতকরণ হিসাবে উচ্চতর টাইমফ্রেমের জেড-স্কোর সিগন্যাল অন্তর্ভুক্ত করুন, শুধুমাত্র যখন একাধিক টাইমফ্রেমের সিগন্যাল সামঞ্জস্যপূর্ণ হয় তখনই ট্রেড করুন, মিথ্যা সিগন্যাল হ্রাস করুন।

- স্টপ-লস মেকানিজম: জেড-স্কোরের ওঠানামার পরিসরের উপর ভিত্তি করে ডায়নামিক স্টপ-লস বাস্তবায়ন করুন, ঝুঁকি ব্যবস্থাপনার ক্ষমতা উন্নত করুন। উদাহরণস্বরূপ, স্টপ-লসকে এন্ট্রি জেড-স্কোরের একটি নির্দিষ্ট বিচ্যুতি গুণকের সমান সেট করা যেতে পারে।

- আংশিক লাভ গ্রহণ: ধাপে ধাপে লাভ নেওয়ার কৌশল বাস্তবায়ন করুন, যখন জেড-স্কোর একটি নির্দিষ্ট থ্রেশহোল্ডে পৌঁছায় তখন আংশিক পজিশন বন্ধ করুন, অর্থ ব্যবস্থাপনা অপ্টিমাইজ করুন।

- ভলিউম নিশ্চিতকরণ: ট্রেডিং নিশ্চিতকরণ হিসাবে ভলিউম বিশ্লেষণ যোগ করুন, শুধুমাত্র যখন জেড-স্কোর সিগন্যাল ভলিউম দ্বারা সমর্থিত হয় তখনই ট্রেড কার্যকর করুন, সিগন্যালের গুণমান উন্নত করুন।

- ইন্ডিকেটর সমন্বয়: জেড-স্কোরকে অন্যান্য পরিসংখ্যানগত বা টেকনিক্যাল ইন্ডিকেটরের সাথে একত্রিত করুন, যেমন RSI বা বলিঞ্জার ব্যান্ড, একটি মাল্টি-ফ্যাক্টর সিদ্ধান্ত গ্রহণের মডেল তৈরি করতে, কৌশলের নির্ভরযোগ্যতা বৃদ্ধি করুন।

সারসংক্ষেপ

মসৃণ জেড-স্কোর ক্রসওভারের উপর ভিত্তি করে মোমেন্টাম-অপ্টিমাইজড প্রাইস স্ট্যাটিস্টিকাল ট্রেডিং স্ট্র্যাটেজি একটি পরিসংখ্যানগত নীতির উপর ভিত্তি করে সরল ট্রেডিং সিস্টেম, যা তার স্থানীয় গড় থেকে মূল্যের বিচ্যুতি এবং ফিরে আসা ধরার উপর দৃষ্টি নিবদ্ধ করে। মসৃণকরণ, সিগন্যাল ব্যবধান নিয়ন্ত্রণ এবং মোমেন্টাম ফিল্টারের মাধ্যমে, কৌশলটি কার্যকরভাবে নয়েজ ট্রেডিং হ্রাস করে এবং সিগন্যালের গুণমান উন্নত করে। কৌশলটি বিশেষ করে রেঞ্জ-বাউন্ড বাজার এবং গড়ে ফিরে আসার আচরণ স্পষ্ট এমন আর্থিক পণ্যের জন্য উপযুক্ত।

তবে, কৌশলটির কিছু সীমাবদ্ধতাও রয়েছে, যেমন পরিসংখ্যানগত অনুমানের উপর নির্ভরশীলতা, প্যারামিটার সংবেদনশীলতা এবং একক ফ্যাক্টর সিদ্ধান্ত গ্রহণ। প্রবণতা সনাক্তকরণ, অস্থিরতা সমন্বয়, মাল্টি-টাইমফ্রেম বিশ্লেষণ, স্টপ-লস মেকানিজম, ভলিউম নিশ্চিতকরণ এবং মাল্টি-ফ্যাক্টর কম্বিনেশনের মতো অপ্টিমাইজেশন ব্যবস্থা যুক্ত করে, কৌশলের দৃঢ়তা এবং কর্মক্ষমতা উল্লেখযোগ্যভাবে উন্নত করা যেতে পারে।

সামগ্রিকভাবে, এটি একটি শক্তিশালী তাত্ত্বিক ভিত্তি, সহজ বাস্তবায়ন, বুঝতে এবং সম্প্রসারণে সহজ একটি কৌশল কাঠামো, যা ট্রেডিং সিস্টেমের মৌলিক উপাদান বা শিক্ষামূলক টুল হিসাবে ব্যবহারের জন্য উপযুক্ত, ট্রেডারদের ট্রেডিংয়ে পরিসংখ্যানের প্রয়োগ বুঝতে সাহায্য করে।

- 1