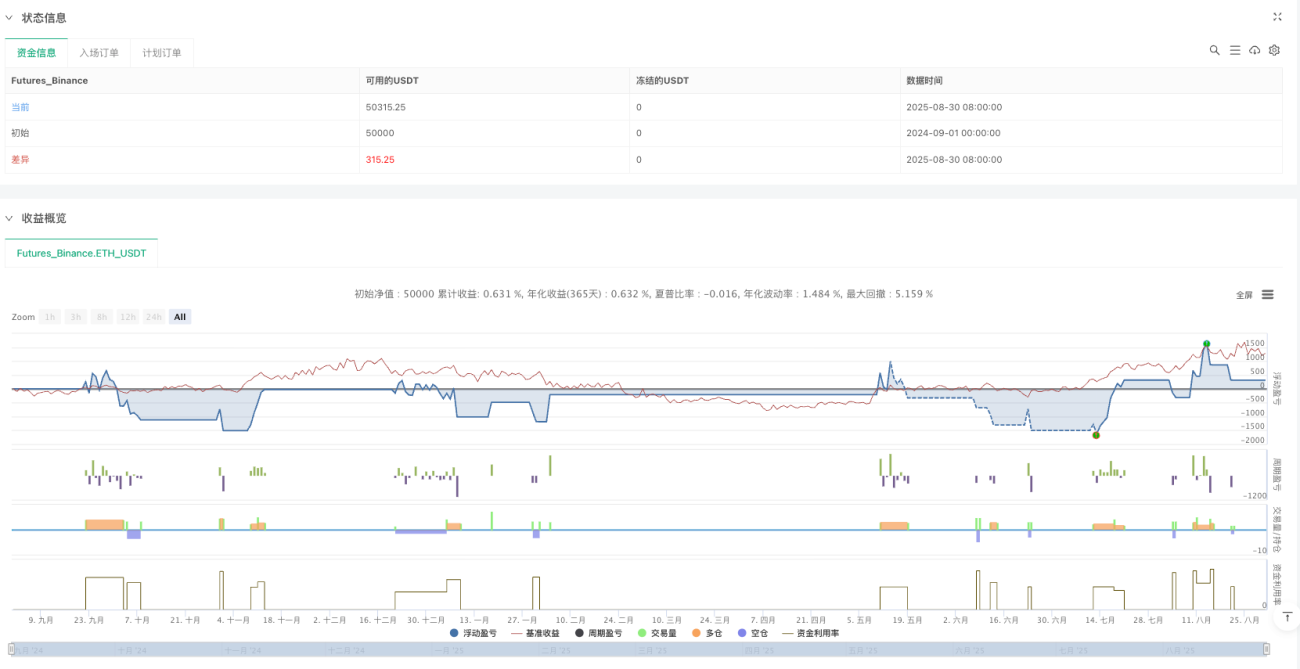

🎯 এই স্ট্র্যাটেজি আসলে কতটা শক্তিশালী?

জানেন কি? বাজারের ৯০% ট্রেডারই দাম বাড়লে কিনে, কমলে বিক্রি করে, কিন্তু প্রকৃত দক্ষ ট্রেডাররা খোঁজেন "দামের শূন্যতা এলাকা"! এই Advanced FVG Strategy Pro+ বিশেষভাবে সেই রহস্যময় ফাঁকগুলো ধরার জন্য তৈরি এক সুপার অস্ত্র 🚀

FVG (Fair Value Gap) মানে সহজ ভাষায় দাম লাফানোর সময় তৈরি হওয়া "ফাঁকা জায়গা", ঠিক যেমন হাঁটার সময় পুকুর এড়িয়ে যাওয়ার মতো—একদিন না একদিন ফিরে এসে সেই ফাঁক পূরণ করতেই হবে। এই স্ট্র্যাটেজি সেই সঠিক সময়ে "ফাঁকের পাশে" লুকিয়ে বসে থাকে মাছ ধরার জন্য!

💡 মূল কথা! তিনটি মূল কোর ব্ল্যাক টেকনোলজি

1. মাল্টি টাইমফ্রেম বিশ্লেষণ 📊

আর শুধু একটি টাইমফ্রেমে সীমাবদ্ধ নয়! স্ট্র্যাটেজি ৫ মিনিটের চার্টে এক্সিকিউট হতে পারে, কিন্তু ১ ঘণ্টার FVG সিগন্যাল ব্যবহার করে—এটা যেন পাহাড় দূর থেকে দেখতে টেলিস্কোপ আর বিস্তারিত দেখতে ম্যাগনিফাইং গ্লাস ব্যবহার করার মতো, দৃষ্টি আরও বিস্তৃত!

2. IIR ট্রেন্ড ফিল্টার 🌊

এটা সাধারণ মুভিং এভারেজ নয়! ইঞ্জিনিয়ারিং-লেভেলের IIR লো-পাস ফিল্টার ব্যবহার করা হয়, যা নিখুঁতভাবে ট্রেন্ডের দিক চিহ্নিত করতে পারে। ভাবুন, এটা যেন আপনার ট্রেডিংয়ে একটি "ট্রেন্ড রাডার" বসানো—শুধু অনুকূল বাতাসেই আক্রমণ!

3. স্মার্ট রিস্ক ম্যানেজমেন্ট 🛡️

শতাংশ ও নির্দিষ্ট পরিমাণ—দুই ধরনের রিস্ক মোড সাপোর্ট করে, পাশাপাশি রয়েছে অ্যাকাউন্ট ধ্বংস প্রতিরোধ মেকানিজম। যেমন গাড়িতে সিটবেল্ট ও এয়ারব্যাগের দ্বৈত সুরক্ষা, তেমনই আপনার অ্যাকাউন্টকে আরও নিরাপদ করে!

🎪 বাস্তব প্রয়োগের দৃশ্যপট

সবচেয়ে উপযোগী এই পরিস্থিতিতে:

- অসিলেটিং মার্কেটে ব্রেকআউটের সুযোগ খোঁজা ⚡

- ট্রেন্ডিং মার্কেটে রিট্রেসমেন্টের এন্ট্রি পয়েন্ট 📈

- গুরুত্বপূর্ণ সাপোর্ট-রেজিস্ট্যান্স এলাকায় নির্ভুল শট 🎯

এড়িয়ে চলার নির্দেশিকা:

- বড় খবরের আগে ব্যবহার বন্ধ রাখুন

- অত্যন্ত কম লিকুইডিটি সম্পন্ন ছোট কয়েনে সাবধান

- বাজারের অস্থিরতা অনুযায়ী রিস্ক প্যারামিটার সমন্বয় করতে মনে রাখবেন

🚀 কেন এই স্ট্র্যাটেজি নির্বাচন করবেন?

প্রচলিত স্ট্র্যাটেজিগুলো হয় খুব কম সিগন্যাল দেয় সুযোগ হারিয়ে, নয়তো বেশি সিগন্যাল দিয়ে মিথ্যা ব্রেকআউটে ফাঁসায়। এই স্ট্র্যাটেজি একাধিক ফিল্টার ব্যবস্থার মাধ্যমে "অল্পেই সঠিক" নীতি অনুসরণ করে!

আর সবচেয়ে ভালো দিক হলো, সব প্যারামিটার কাস্টমাইজ করা যায়—ঠিক যেমন সাউন্ড ইঞ্জিনিয়ার টোন সমন্বয় করে, তেমনই আপনি ভিন্ন বাজার পরিবেশে সবচেয়ে উপযুক্ত ট্রেডিং রিদম "তৈরি" করতে পারেন 🎵

মনে রাখবেন: ভালো স্ট্র্যাটেজি আপনাকে প্রতিদিন ট্রেড করতে বলবে না, বরং সবচেয়ে নিশ্চিত সুযোগে আঘাত করতে শেখায়! এটাই FVG স্ট্র্যাটেজির ম্যাজিক ✨

- 1