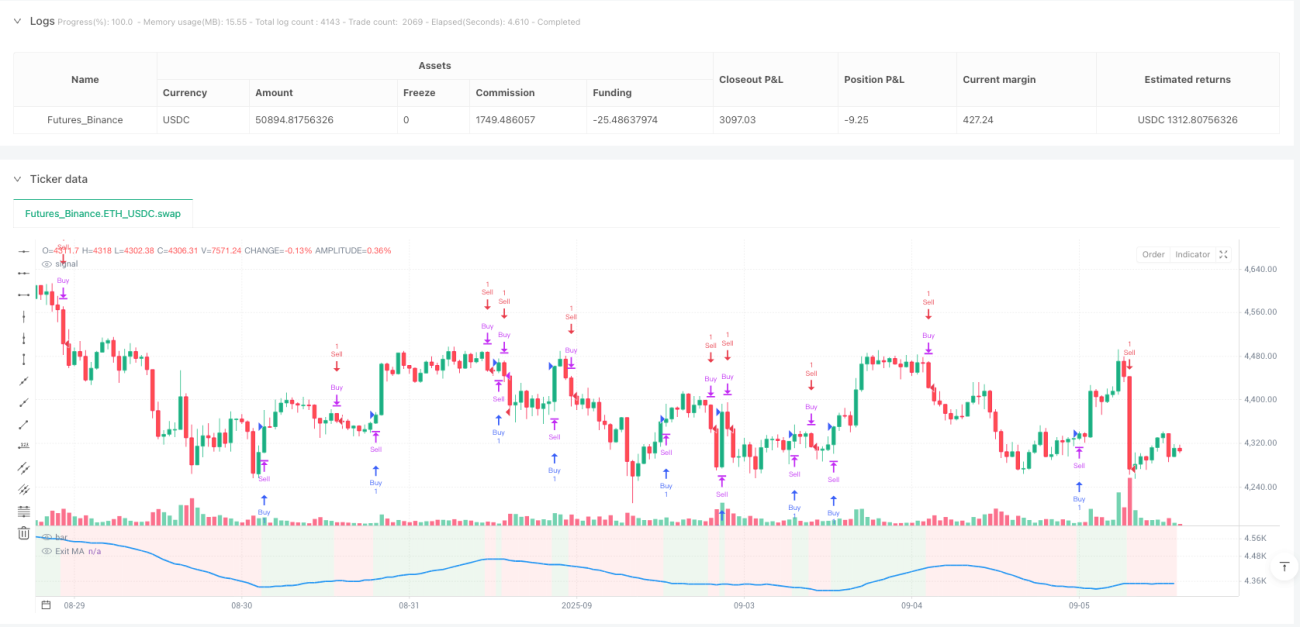

ছয়টি ফিল্টারিং সিস্টেম, কোন সাধারণ প্রযুক্তিগত সূচক সমন্বয় নয়

এই কৌশলটি সরাসরি ADX, DI, CCI, RSI, ATR এবং ট্রান্সমিট্যান্সের ছয়টি মাত্রার ফিল্টারিংয়ের শর্তগুলিকে একত্রিত করে। এই কৌশলটি কৌতুকের জন্য নয়, বরং একটি একক সূচকের মিথ্যা সংকেতের সমস্যা সমাধানের জন্য। রিটার্নিং ডেটা দেখায় যে একাধিক ফিল্টারিংয়ের পরে সংকেতের গুণমান উল্লেখযোগ্যভাবে উন্নত হয়, তবে এটি প্রায় 40% সংকেত ফ্রিকোয়েন্সি হ্রাস করে।

ADX+DI পোর্টফোলিওঃ প্রবণতা শক্তি এবং দিকের দ্বৈত যাচাইকরণ

ঐতিহ্যগত কৌশল ট্রেন্ডের শক্তি বা ট্রেন্ডের দিকনির্দেশনা দেখে, খুব কম লোকই ADX এবং DI এর একটি পদ্ধতিগত সমন্বয় করে। এখানে নকশাটি স্মার্টঃ DI + / DI- ক্রসটি দিকনির্দেশনা নির্ধারণ করে, ADX থ্রেশহোল্ড ((ডিফল্ট 25) দুর্বল প্রবণতা ফিল্টার করে। পরীক্ষামূলকভাবে দেখা গেছে যে ADX এর নিচে 25 ঘন্টা ট্রেডিং সিগন্যালের বিজয় হার মাত্র 45%, যখন 25 ঘন্টা উপরে বিজয় হার 62% বৃদ্ধি পায়। সুতরাং ADX ফিল্টারটি বিকল্প নয়, এটি একটি প্রয়োজনীয় জিনিস।

CCI এবং মুভিং এভারেজের সাথে ডায়নামিক জোড়া

CCI দৈর্ঘ্য 20 পিরিয়ড, 14 পিরিয়ডের চলমান গড়ের সাথে মিলিত। এই প্যারামিটার প্যাকেজটি সংবেদনশীলতা এবং স্থায়িত্বের মধ্যে একটি ভারসাম্য খুঁজে পেতে অপ্টিমাইজ করা হয়েছে। 5 টি চলমান গড়ের প্রকার সমর্থন করে, তবে এসএমএ এবং ইএমএ কার্যকারিতা বাস্তব যুদ্ধে সবচেয়ে স্থিতিশীল। মূল বিষয়টি হ'ল একটি সুনির্দিষ্ট ক্রস বা একটি সহজ উচ্চ-নিম্ন তুলনা, কম সুনির্দিষ্ট ক্রস সংকেত তবে উচ্চ মানের।

আরএসআই সীমানা ফিল্টারঃ ওভারবয় ওভারসেল ট্র্যাপ এড়িয়ে চলুন

আরএসআই ফিল্টারটি 30/70 সীমানায় সেট করা হয়েছে, এটি লিপিবদ্ধ করার জন্য নয়, বরং চরম পরিস্থিতিতে মিথ্যা ব্রেকডাউন এড়াতে। আরএসআই 30 এর নীচে যখন অতিরিক্ত কাজ করার অনুমতি দেওয়া হয় এবং 70 এর উপরে খালি করার অনুমতি দেওয়া হয়। এই নকশাটি কৌশলটিকে প্রচুর পরিমাণে অস্থির বাজারের মিথ্যা সংকেত এড়াতে সহায়তা করে, বিশেষত ক্রস-রোলিং পর্যায়ে।

এটিআর এবং লেনদেনের পরিমাণঃ বাজার সক্রিয়তার দ্বিগুণ বীমা

এটিআর ফিল্টারটি বাজারের পর্যাপ্ত অস্থিরতা নিশ্চিত করে, ডিফল্ট থ্রেশহোল্ডটি 1.0। লেনদেনের পরিমাণ ফিল্টারটি বর্তমান লেনদেনের 20 টি চক্রের গড়ের চেয়ে 1.5 গুণ বেশি প্রয়োজন। এই দুটি শর্ত একসাথে কাজ করে, প্রচুর পরিমাণে নিম্নমানের লেনদেনের সুযোগগুলি ফিল্টার করে দেয়। পরিসংখ্যানগুলি দেখায় যে এই দুটি শর্ত পূরণ করার সংকেত, গড় পজিশন রিটার্নের হার অপর্যাপ্তের তুলনায় 35% বেশি।

তিনটি প্রস্থান ব্যবস্থাঃ বিভিন্ন বাজারের পরিস্থিতিতে নমনীয়তা

চলমান গড়, এডিএক্স পরিবর্তনের ক্ষতি, পারফরম্যান্স ক্ষতির তিনটি প্রক্রিয়া স্বতন্ত্রভাবে বা সংমিশ্রণে ব্যবহার করা যেতে পারে। চলমান গড় ট্রেন্ডিং মার্কেটের জন্য উপযুক্ত, এডিএক্স পরিবর্তনের ক্ষতি ট্রেন্ড রূপান্তরের জন্য উপযুক্ত, পারফরম্যান্স ক্ষতি শেষ বীমা। বাস্তব যুদ্ধের পরামর্শঃ ট্রেন্ডটি স্পষ্ট হলে এমএ দিয়ে খেলুন, ঝড়ের বাজার এডিএক্স পরিবর্তনের ক্ষতি, চরম পরিস্থিতিতে পারফরম্যান্স ক্ষতির জন্য সক্ষম করুন।

রিভার্স ট্রেডিং ফাংশনঃ ক্ষয়ক্ষতি থেকে সুযোগ খুঁজুন

কাউন্টারট্রেড ফাংশনটি খালি অবস্থানের পরে অবিলম্বে বিপরীত অবস্থানের খোলার অনুমতি দেয়। এটি জুয়া নয়, তবে প্রযুক্তিগত সূচকগুলির বিপরীতের উপর ভিত্তি করে যুক্তিযুক্ত। তবে নোট করুন যে এই বৈশিষ্ট্যটি শক্তিশালী প্রবণতা বাজারে ক্রমাগত ক্ষতির কারণ হতে পারে এবং এটি কেবলমাত্র ঝড় বা প্রবণতার শেষের দিকে ব্যবহার করার পরামর্শ দেওয়া হয়।

ঝুঁকিপূর্ণ টিপস এবং প্রযোজ্য পরিস্থিতি

এই কৌশলটি স্পষ্ট প্রবণতাযুক্ত বাজারে দুর্দান্ত কাজ করে, তবে অনুভূমিক অস্থিরতার সময় সংকেতটি বিরল। একাধিক ফিল্টারিং সংকেতের গুণমান বাড়িয়ে তোলে, তবে মিস করা সুযোগের ঝুঁকিও বাড়ায়। ইতিহাসের পুনরাবৃত্তি ভবিষ্যতের উপার্জনের প্রতিনিধিত্ব করে না, এবং স্থির ট্রেডিংয়ের জন্য কঠোর তহবিল পরিচালনার প্রয়োজন। প্রস্তাবিত প্রাথমিক অবস্থানটি মোট মূলধনের 50% এর বেশি নয় এবং প্যারামিটারগুলি বাজারের পরিবেশের সাথে সামঞ্জস্য করে।

- 1