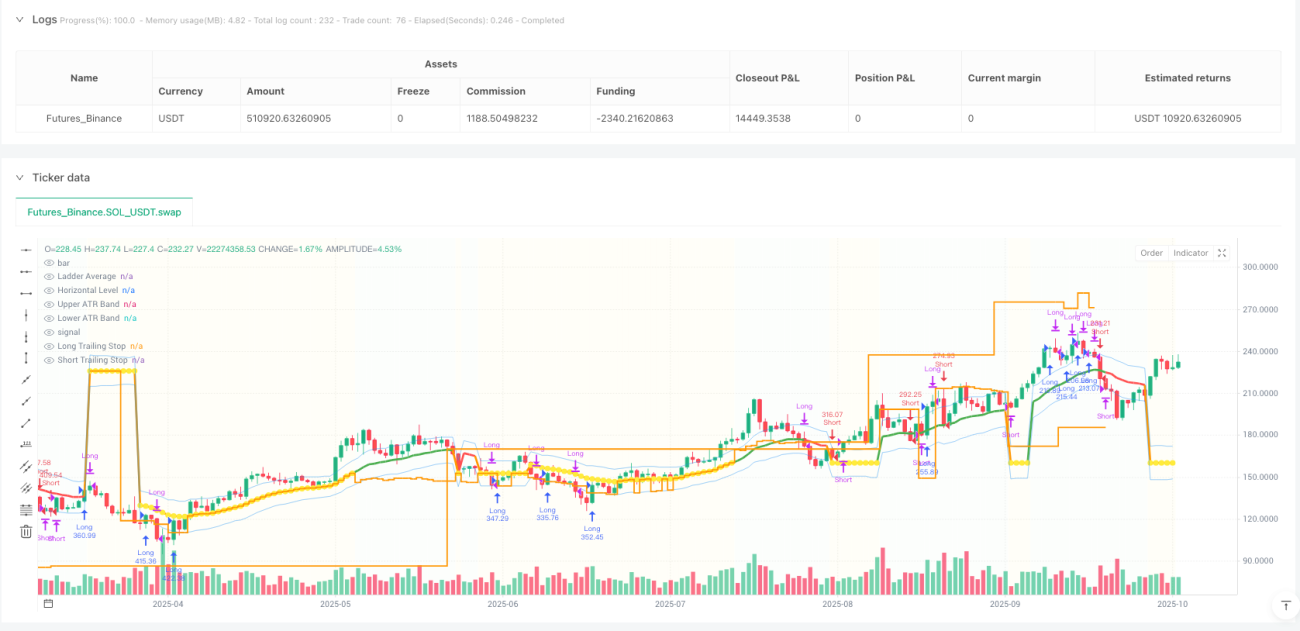

## ট্রেন্ড স্টেপ এভারেজ স্ট্র্যাটেজি: যখন বাজার পাশে ঘুরছে তখন কীভাবে সুন্দরভাবে 'নিষ্ক্রিয় থাকা' যায়?

কেন ঐতিহ্যবাহী ট্রেন্ড ট্র্যাকিং কৌশলগুলি সাইডওয়ে মার্কেটে ঘন ঘন "ব্যর্থ" হয়?

একজন কোয়ান্টিটেটিভ ট্রেডিং পেশাদার হিসেবে, আমাকে প্রায়ই এমন একটি প্রশ্ন করা হয়ঃ কেন সেই কৌশলগুলি, যা ট্রেন্ড মার্কেটে অসাধারণ পারফর্ম করে, সাইডওয়ে মার্কেটে এসে বড় রকমের রিটার্ন দিতে শুরু করে?

উত্তরটি আসলে খুব সহজঃ বেশিরভাগ ট্রেন্ড ট্র্যাকিং কৌশলেরই "ট্রেন্ড বাধ্যতামূলক ব্যাধি" থাকে - তারা সবসময় যেকোনো মার্কেট পরিবেশে উচ্চ-ফ্রিকোয়েন্সি ট্রেডিং চালিয়ে যাওয়ার চেষ্টা করে, কিন্তু একটি মৌলিক সত্য উপেক্ষা করেঃ বাজারের ৭০% সময়ই রেঞ্জবাউন্ড বা সাইডওয়ে অবস্থায় থাকে।

আজ যে "ট্রেন্ড স্টেপড অ্যাভারেজ স্ট্র্যাটেজি" বিশ্লেষণ করব, তা এই সমস্যাটির জন্য একটি মজার সমাধান প্রস্তাব করেঃ ট্রেন্ড মার্কেটে সক্রিয়ভাবে ট্র্যাক করা, আর সাইডওয়ে মার্কেটে "সুন্দরভাবে বিশ্রাম নেওয়া"।

"স্টেপড অ্যাভারেজ" কী? এই ধারণাটি কীভাবে ট্রেন্ড ট্র্যাকিংকে পুনরায় সংজ্ঞায়িত করে?

ঐতিহ্যবাহী মুভিং অ্যাভারেজ কৌশলগুলির একটি মারাত্মক ত্রুটি আছে: তারা সবসময় পরিবর্তিত হয়। বাজার শক্তিশালী ট্রেন্ডে থাকুক বা সাইডওয়ে অবস্থায় থাকুক, মুভিং অ্যাভারেজ দামের ওঠানামার সাথে সাথে ক্রমাগত সমন্বয় করতে থাকে, যার ফলে প্রচুর মিথ্যা সংকেত তৈরি হয়।

"স্টেপড অ্যাভারেজ"-এর মূল ধারণা হলঃ নির্দিষ্ট শর্তে মুভিং অ্যাভারেজকে "হিমায়িত" করা।

প্রয়োগের নির্দিষ্ট যুক্তি নিম্নরূপঃ

-

ট্রেন্ড অবস্থা সনাক্তকরণ: ADX সূচকের মাধ্যমে বাজারের ট্রেন্ড শক্তি নির্ণয়

- ADX > 25: শক্তিশালী ট্রেন্ড বাজার

- মুভিং অ্যাভারেজের ঢাল < 0.3%: সাইডওয়ে বাজার

-

গতিশীল মুভিং অ্যাভারেজ স্যুইচিং:

- শক্তিশালী ট্রেন্ডের সময়: সাধারণত EMA(21) ট্র্যাক করে

- সাইডওয়ে অবস্থায়: মুভিং অ্যাভারেজ অনুভূমিক অবস্থানে "হিমায়িত" হয়, সমর্থন/প্রতিরোধ সৃষ্টি করে

এই ডিজাইনের চতুরতা হলোঃ এটি কৌশলটিকে বিভিন্ন মার্কেট পরিবেশে ভিন্ন "ব্যক্তিত্ব" প্রদর্শন করতে দেয় - ট্রেন্ডের সময় সংবেদনশীল, সাইডওয়ে অবস্থায় স্থিতিশীল।

"ট্রেন্ড ক্যাপচার" সিস্টেম কীভাবে বাস্তবায়ন করা হয়?

মৌলিক স্টেপড অ্যাভারেজ মেকানিজম ছাড়াও, এই কৌশলটি একটি "ট্রেন্ড ক্যাপচার" মডিউলও সংযুক্ত করে, যা আমার মতে সবচেয়ে উদ্ভাবনী অংশঃ

দ্রুত রিভার্সাল মেকানিজম:

- যখন সম্প্রতি ক্লোজ করা পজিশনের বিপরীতে একটি শক্তিশালী ট্রেন্ড দেখা যায়

- ৩ পিরিয়ডের মধ্যে দ্রুত নতুন পজিশন খোলা

- শর্ত: ADX > 30 এবং DI+ ও DI- এর পার্থক্য > 10

এই ডিজাইনটি ঐতিহ্যবাহী কৌশলগুলির একটি গুরুত্বপূর্ণ সমস্যা সমাধান করেঃ কীভাবে ট্রেন্ড রিভার্সালের প্রাথমিক পর্যায়ে দ্রুত পজিশন সামঞ্জস্য করা যায়।

এমন একটি দৃশ্য কল্পনা করুনঃ আপনি সবেমাত্র স্টপ লসে লং পজিশন ক্লোজ করেছেন, অথচ বাজার তৎক্ষণাৎ শক্তিশালী বিয়ারিশ ট্রেন্ডে চলে গেল। ঐতিহ্যবাহী কৌশলগুলির নতুন সংকেত নিশ্চিত হওয়ার জন্য অপেক্ষা করতে হতে পারে, কিন্তু এই "ট্রেন্ড ক্যাপচার" সিস্টেম ৩ পিরিয়ডের মধ্যে দ্রুত শর্ট পজিশন খুলতে পারে।

রিস্ক ম্যানেজমেন্ট: কেন বাজারের অবস্থা আলাদা করতে হবে?

এই কৌশলটির সবচেয়ে শিক্ষণীয় দিক হল এর পার্থক্যপূর্ণ রিস্ক ম্যানেজমেন্ট মেকানিজম:

সাইডওয়ে মার্কেটে রিস্ক কন্ট্রোল:

- স্টপ লস স্টেপড অ্যাভারেজ লাইনের কাছাকাছি সামঞ্জস্য করা

- ATR মাল্টিপল কমানো, স্টপ লস টাইট করা

- টার্গেট সেটিং আরও রক্ষণশীল হওয়া

ট্রেন্ড মার্কেটে রিস্ক কন্ট্রোল:

- স্ট্যান্ডার্ড ATR মাল্টিপল স্টপ লস ব্যবহার

- স্টেপড ট্রেইলিং স্টপ লস চালু করা

- দামের চলাচলের জন্য বেশি জায়গা দেওয়া

এই ডিজাইনটি একটি গুরুত্বপূর্ণ ট্রেডিং ফিলোসফি প্রতিফলিত করেঃ বিভিন্ন মার্কেট পরিবেশে ভিন্ন রিস্ক প্রোফাইল প্রয়োজন। সাইডওয়ে মার্কেটে আমাদের আরও সতর্ক হওয়া উচিত; ট্রেন্ড মার্কেটে আমাদের লাভের জন্য আরও জায়গা দেওয়া উচিত।

স্টেপড ট্রেইলিং স্টপ লস: কীভাবে লাভ সুরক্ষিত করা এবং ট্রেন্ড ট্র্যাকিংয়ের মধ্যে ভারসাম্য বজায় রাখা যায়?

ঐতিহ্যবাহী ট্রেইলিং স্টপ লস প্রায়ই যান্ত্রিক হয়, হয় খুব টাইট হয়ে তাড়াতাড়ি এক্সিট হয়, নয়তো খুব লুজ হয়ে কার্যকরভাবে লাভ সুরক্ষিত করতে পারে না। এই কৌশলের স্টেপড ট্রেইলিং স্টপ লস একটি আরও স্মার্ট সমাধান দেয়:

স্টেপ সেটিং লজিক:

- ATR-এর উপর ভিত্তি করে স্টেপ দূরত্ব গতিশীলভাবে গণনা করা

- সর্বোচ্চ ৫টি স্টেপ লেভেল সেট করা

- প্রতিটি স্টেপ ব্রেক করার সময় স্টপ লস ঊর্ধ্বমুখী সমন্বয়

এই ডিজাইনের সুবিধা হলোঃ এটি লাভ সুরক্ষিত রাখার পাশাপাশি ট্রেন্ডের জন্য পর্যাপ্ত বিকাশের জায়গা নিশ্চিত করে।

বাস্তব প্রয়োগে কী কী বিষয় খেয়াল রাখতে হবে?

আমার লাইভ ট্রেডিং অভিজ্ঞতার ভিত্তিতে, এই ধরনের কৌশল ব্যবহার করার সময় নিম্নলিখিত বিষয়গুলি খেয়াল রাখা জরুরি:

-

প্যারামিটার অপ্টিমাইজেশনের ফাঁদ: ADX থ্রেশহোল্ড অতিরিক্ত অপ্টিমাইজ করবেন না, ২৫-৩০ এর মধ্যে মান বেশিরভাগ বাজারে স্থিতিশীল থাকে

-

বাজার অভিযোজনযোগ্যতা: এই কৌশলটি মাঝারি অস্থিরতার বাজারের জন্য বেশি উপযুক্ত, চরম অস্থিরতার পরিবেশে ATR মাল্টিপল সামঞ্জস্যের প্রয়োজন হতে পারে

-

মানি ম্যানেজমেন্ট: বিশেষ করে ট্রেন্ড ক্যাপচার ফিচার ব্যবহার করার সময়, প্রতি ট্রেডে মোট মূলধনের ১০% এর বেশি না লাগানোর পরামর্শ দেওয়া হয়

-

ব্যাকটেস্টিং ফাঁদ: স্লিপেজ এবং কমিশনের প্রভাব বিশেষ করে খেয়াল রাখবেন, বিশেষ করে সাইডওয়ে মার্কেটে ঘন ঘন ট্রেডিংয়ের সময়

এই কৌশলটির উদ্ভাবনী মূল্য কোথায়?

কোয়ান্টিটেটিভ স্ট্র্যাটেজি উন্নয়নের দৃষ্টিকোণ থেকে, এই কৌশলটি একটি গুরুত্বপূর্ণ বিবর্তনের দিক নির্দেশ করেঃ একক যুক্তি থেকে বহু-অবস্থা অভিযোজিত সিস্টেমে রূপান্তর।

ঐতিহ্যবাহী কৌশলগুলি প্রায়ই একটি নির্দিষ্ট যুক্তি দিয়ে সব মার্কেট পরিস্থিতি মোকাবেলা করার চেষ্টা করে, কিন্তু এই কৌশলটি "স্থানভেদে কৌশল"-এর প্রজ্ঞা প্রদর্শন করেঃ

- ট্রেন্ড মার্কেটে এটি একটি আক্রমণাত্মক ট্রেন্ড ফলোয়ার হিসেবে আচরণ করে

- সাইডওয়ে মার্কেটে এটি একটি রক্ষণশীল রেঞ্জ ট্রেডার হিসেবে আচরণ করে

এই ডিজাইন চিন্তাটি কৌশল ডেভেলপারদের জন্য গুরুত্বপূর্ণ প্রেরণা প্রদান করেঃ আমাদের কৌশলটিকে "বাজার উপলব্ধি" করার ক্ষমতা দেওয়া উচিত, নির্দিষ্ট যুক্তি অন্ধভাবে অনুসরণ করা নয়।

পরিশেষে, জোর দিয়ে বলতে চাই যে কোনো কৌশলই সর্বজনীন নয়। এই স্টেপড অ্যাভারেজ কৌশল তত্ত্বগতভাবে মার্জিত হলেও, বাস্তব প্রয়োগে নির্দিষ্ট বাজার পরিবেশ এবং ব্যক্তিগত রিস্ক প্রোফাইলের সাথে সামঞ্জস্য করতে হবে। মনে রাখবেন, সেরা কৌশলটি সবসময় সেইটিই যা আপনার জন্য সবচেয়ে উপযুক্ত।

/*backtest

start: 2024-10-09 00:00:00

end: 2025-10-07 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"SOL_USDT","balance":500000}]

*/

//@version=5

strategy("Trend Following Ladder Average Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// ═══════════════════════════════════════════════════════════════════════════════- 1