স্বর্ণের তারল্য শিকারী কৌশল

🎯 এই কৌশলটি আসলে কী করছে?

আপনি কি জানেন? বাজারে কিছু 'স্মার্ট মানি' সবসময় গুরুত্বপূর্ণ জায়গায় ফাঁদ পেতে পছন্দ করে! এই কৌশলটি একজন অভিজ্ঞ শিকারীয়ের মতো, বিশেষভাবে এই ফাঁদগুলো চিহ্নিত করে এবং বিপরীত দিকে কাজ করে। সহজভাবে বললে, যখন দাম ইচ্ছাকৃতভাবে গুরুত্বপূর্ণ সাপোর্ট-রেজিস্ট্যান্স লেভেল 'ভাঙার ভান' করে এবং তারপর দ্রুত ফিরে আসে, তখন আমরা বড় মূলধনের তালে তাল মিলিয়ে বাজারে প্রবেশ করি!

📊 ট্রিপল ফিল্টারেশন সিস্টেমের রহস্য উন্মোচন

গুরুত্বপূর্ণ কথা! এই কৌশলটি তিনটি সুরক্ষা স্তর ব্যবহার করে:

🔸 ট্রেন্ড ফিল্টার: 200-পিরিয়ড EMA একজন পাকা ড্রাইভারের মতো, আপনাকে বলে দেয় এখন চড়াই নাকি উৎরাই পথ

🔸 কী লেভেল চিহ্নিতকরণ: স্বয়ংক্রিয়ভাবে সেই 'যুদ্ধক্ষেত্রের' সাপোর্ট-রেজিস্ট্যান্স লেভেলগুলো খুঁজে বের করে

🔸 লিকুইডিটি সুইপ ডিটেকশন: বড় মূলধনের ইচ্ছাকৃত 'ভুয়া চাল' ধরে ফেলে

ঠিক যেন মাছ ধরার মতো—আপনাকে জানতে হবে মাছ কোথায়, কী টোপ ব্যবহার করতে হবে, এবং কখন জাল টানতে হবে!

🎪 লিকুইডিটি সুইপের জাদুকরী আকর্ষণ

কল্পনা করুন: আপনি একটি চায়ের দোকানে লাইনে দাঁড়িয়ে আছেন, হঠাৎ কেউ চিৎকার করে বলে 'ফ্রি!' সবাই সেদিকে ছুটে যায়, কিন্তু দেখা যায় তা ভুয়া, তবে বুদ্ধিমান ব্যক্তি সেই সুযোগে সামনে চলে গেছে।

বাজারও তাই! দাম প্রথমে 'ভুলে' সাপোর্ট লেভেল ভাঙে (স্টপ লস অর্ডার সুইপ করে), তারপর দ্রুত ফিরে আসে—এটাই সেরা এন্ট্রির সময়। কৌশলটি 0.6 গুণ ATR-এর বাফার সেট করে, নিশ্চিত করতে যে এটি সত্যিই একটি 'সুইপ'—সত্যিকারের ব্রেকআউট নয়।

⚡ ঝুঁকি নিয়ন্ত্রণ: 1:2 স্বর্ণালী অনুপাত

ফাঁদ এড়ানোর নির্দেশিকা: অনেক মানুষ ট্রেড করে যেন গাড়ি চালাচ্ছেন কিন্তু সিট বেল্ট বাঁধেননি—এই কৌশলটি বাধ্যতামূলকভাবে 1:2 ঝুঁকি-পুরস্কার অনুপাত প্রয়োগ করে!

- স্টপ লস সেট করা হয় কী লেভেলের নিচে 0.5 গুণ ATR দূরে

- টেক প্রফিট স্টপ লসের দ্বিগুণ দূরত্বে

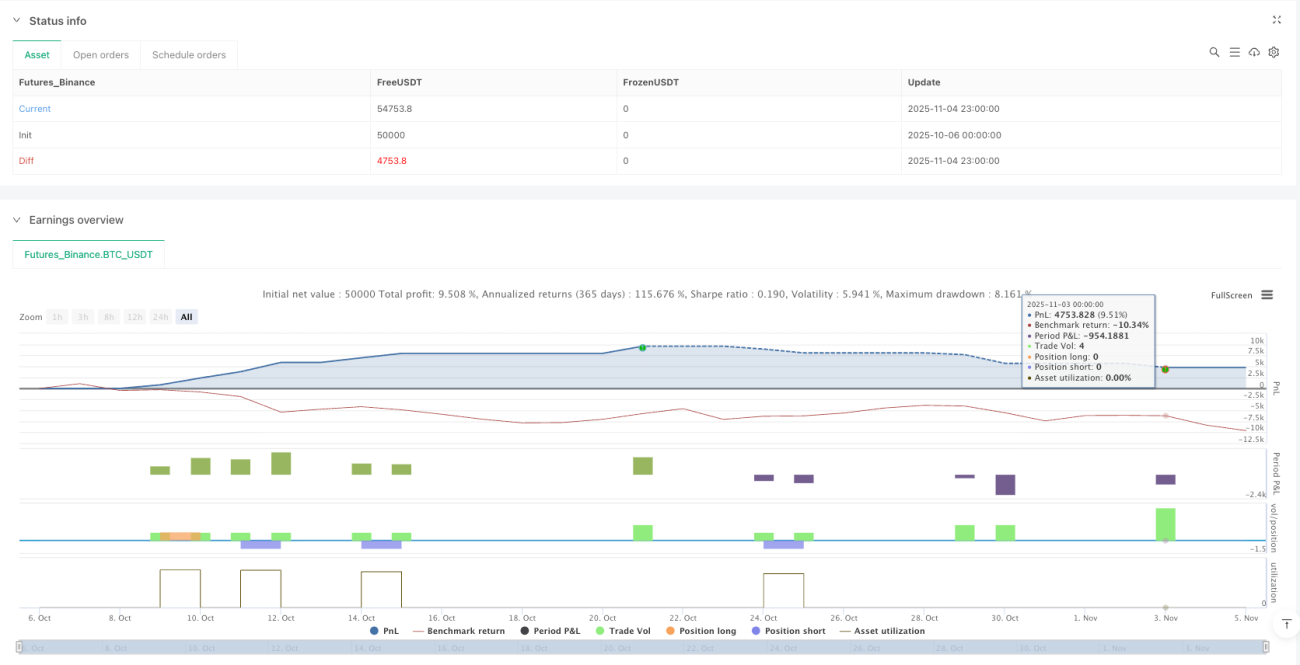

- এমনকি যদি সাফল্যের হার মাত্র 40% হয়, তবুও দীর্ঘমেয়াদে লাভজনক!

🚀 বাস্তব প্রয়োগের টিপস

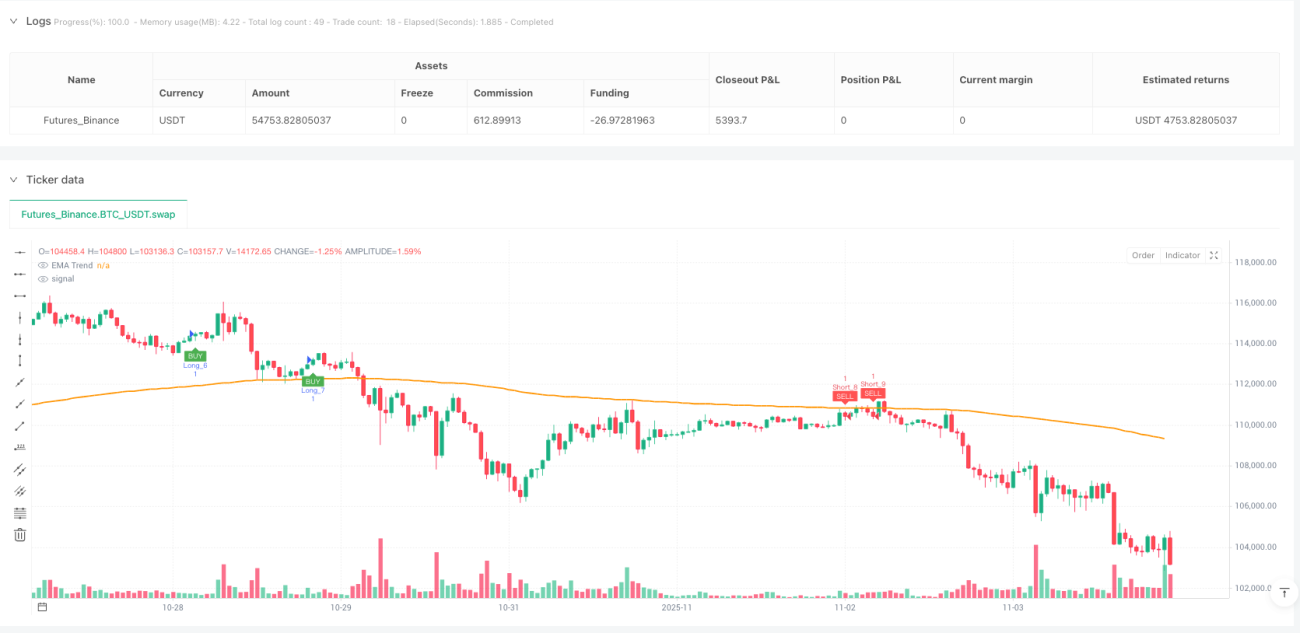

এই কৌশলটি 15 মিনিটের টাইমফ্রেমে গোল্ড ট্রেডিংয়ের জন্য সবচেয়ে উপযুক্ত। কেন? কারণ গোল্ড বাজারে তারল্য ভালো, ভুয়া ব্রেকআউটের প্রবণতা স্পষ্ট, এবং 15 মিনিটের টাইমফ্রেম অতিরিক্ত নয়েজ ফিল্টার করে দেয়।

মনে রাখবেন: লোভ করবেন না! কৌশলটি আপনার জন্য ভালো জায়গা খুঁজে দিয়েছে—বাকি কাজ বাজার এবং সময়কে করতে দিন।

/*backtest

start: 2025-10-06 00:00:00

end: 2025-11-05 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Gold 15m: Trend + S/R + Liquidity Sweep (RR 1:2)", overlay=true, default_qty_type=strategy.fixed, default_qty_value=1, commission_type=strategy.commission.percent, commission_value=0.0)

// ---------------------- INPUTS ----------------------- 1