Strategie zur Bodenumkehr mit mehreren Zeitrahmen

Überblick

Die Strategie nutzt eine Kombination aus mehreren grundlegenden Formindikatoren, um die Zeit für eine starke Umkehr zu identifizieren, und verfolgt eine Trend-Stopp-Strategie, die darauf abzielt, mehr zu gewinnen als zu stoppen.

Grundsätze

Die Strategie basiert auf folgenden Indikatoren, um eine Bottom-up-Umkehr zu bestimmen:

-

Noro's BottomSensivity: Beurteilt, ob eine bestimmte Bottomform auf der K-Linie auftritt.

-

Der Index der Bestimmtheitsbereitschaft (CVI): Beurteilung der Transformation der Mehrraumpsychologie.

-

Der Endindikator ((UCS): Beurteilung der Abweichung von der Durchschnittslinie.

-

Der RSI: Überverkauf.

-

Formkombination: umfasst mehrere Unterformen, wie z. B. Schrägstücke, Figuren und ähnliches.

Die Strategie verwendet mehrere Kombinationen von Basisindikatoren, um ein Kaufsignal zu erzeugen, wenn die Anzahl der Basisformate, die für die Strategieparameter festgelegt ist, erfüllt wird. Zur Filterung falscher Durchbrüche wird die Strategie auch die RSI-Indikatorentscheidung hinzugefügt, die nur bei Überverkauf ein Kauf auslöst.

Die Benutzer können die Verwendung und die Parameter der einzelnen unteren Beurteilungsindikatoren konfigurieren, was eine hohe Flexibilität ermöglicht. Die Strategie enthält auch eine SMA-Gleichgewichtsfilterung, um zu vermeiden, dass sie unter dem Trend liegt.

Vorteile

-

Mehrfache Indikatoren zur Gewissheit

-

Anpassbare Kennwerte für verschiedene Sorten

-

SMA-Gleichfilterung, Vermeidung von Überschneidungen

-

Eintritt nur auf der roten K-Linie, um das Risiko zu verringern

-

Mit einem Pop-up-Alarm und einer Echtzeitüberwachung

Die Gefahr

-

Mehrfaches Kombi-Gutachten könnte den Tiefpunkt übersehen haben

-

Die Grundform muss sich nicht ständig umdrehen

-

Es ist wichtig, sich darauf zu konzentrieren, ob die Umkehrung durch den Umsatz unterstützt werden kann.

Optimierungsrichtung

-

Optimierung der Parameterkonfiguration der Kennzahlen und Anpassung an die verschiedenen Sorten

-

Erhöhung der Lagerhaltung und Senkung der Kosten durch Lagerhaltung

-

Erhöhung der Stop-Loss-Strategie und Verfolgung von Trendstop-Losses

Zusammenfassen

Die Strategie nutzt mehrere Indikatoren, um die Basis zu verbessern und die Gewinne zu verringern. Die Risiken können durch Trendverfolgung und Stop-Loss-Lock-in effektiv kontrolliert werden. Es ist jedoch wichtig zu beachten, ob das Handelsvolumen den Trend umkehren kann.

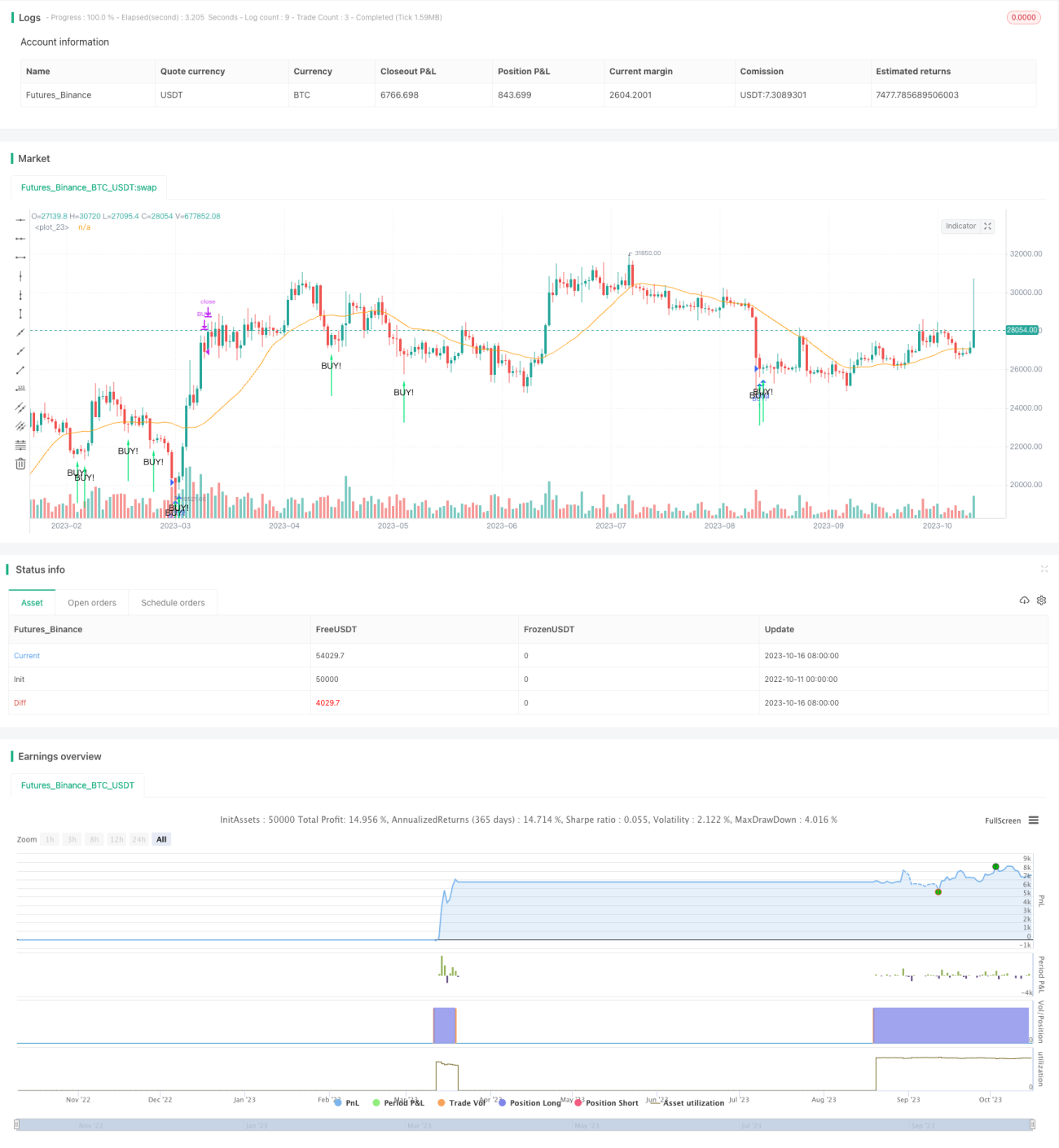

/*backtest

start: 2022-10-11 00:00:00

end: 2023-10-17 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// the original indicator is Noro's BottomSensivity v0.6

//@version=4

strategy("Noro's BottomSensivity v0.6 strategy + rsi + Alarm", shorttitle="Bottom 0.6 StRsiAlarm", overlay=true)

- 1