Kurzfristige Trendstrategie basierend auf Entscheidungen mit mehrdimensionalen Indikatoren

Überblick

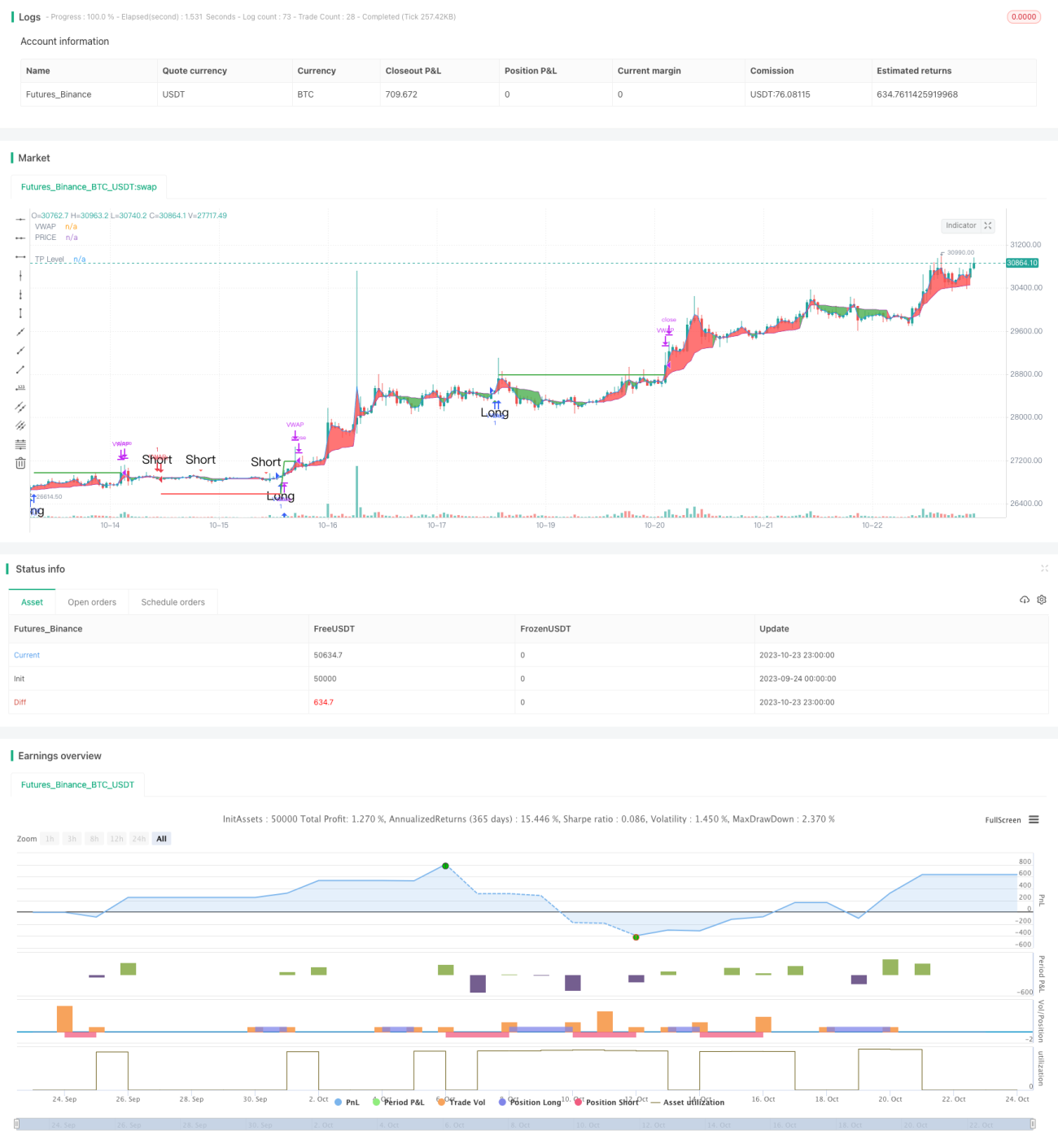

Diese Strategie kombiniert drei technische Indikatoren aus verschiedenen Dimensionen: Unterstützungs- und Widerstandsniveaus, ein gleitende-Durchschnitte-System und überkaufte/überverkaufte Indikatoren. Anhand ihrer kombinierten Signale wird die kurzfristige Trendrichtung bestimmt, um eine hohe Trefferquote zu erzielen.

Strategieprinzip

Im Code werden zunächst die Unterstützungs- und Widerstandsniveaus des Kurses berechnet, darunter die Standard-Oszillatorachse und Fibonacci-Unterstützungs-/Widerstandsniveaus, und in das Diagramm eingezeichnet. Wenn der Kurs diese Schlüsselniveaus durchbricht, wird dies als wichtiges Trendsignal betrachtet.

Anschließend werden der volumengewichtete gleitende Durchschnitt (VWAP) und der Durchschnittskurs berechnet, um deren Goldenes Kreuz und Todeskreuz zu ermitteln. Dies dient der mittel- bis langfristigen Trendanalyse.

Zuletzt wird der Stochastic RSI-Indikator berechnet, um dessen Goldenes Kreuz und Todeskreuz zu bestimmen – dies ist ein überkaufter/überverkaufter Indikator.

Werden die Signale aus diesen drei Dimensionen kombiniert, wird eine Long-Position eröffnet, wenn Unterstützungs-/Widerstandsniveaus, VWAP-Gleitender-Durchschnitt und Stochastic RSI gleichzeitig ein Kaufsignal senden. Eine Short-Position wird eröffnet, wenn alle drei gleichzeitig ein Verkaufssignal senden.

Vorteilsanalyse

Der größte Vorteil dieser Strategie ist die Kombination von Indikatoren aus drei verschiedenen Dimensionen, was die Beurteilung umfassender und genauer macht und die Trefferquote erhöht. Zunächst zeigen die Unterstützungs-/Widerstandsniveaus den großen Trend, dann der VWAP den mittel- bis langfristigen Trend, und schließlich der Stochastic RSI die überkaufte/überverkaufte Situation. Wenn alle drei Dimensionen gleichzeitig ein Signal senden, können Fehlsignale stark gefiltert und die Erfolgsquote beim Einstieg verbessert werden.

Zusätzlich ist eine Take-Profit-Funktion integriert, die es erlaubt, einen bestimmten prozentualen Gewinn zu sichern, was das Risikomanagement unterstützt.

Risikoanalyse

Das Hauptrisiko dieser Strategie besteht darin, dass die Entscheidung zum Long oder Short von der Synchronität der Indikatorsignale abhängt. Wenn einige Indikatoren Fehlsignale senden, kann dies zu Fehlentscheidungen führen. Sendet beispielsweise der Stochastic RSI ein überkauftes Signal, während VWAP und Unterstützungs-/Widerstandsniveaus weiterhin aufwärtsgerichtet sind, könnte der Einstiegspunkt verpasst und nicht gehandelt werden.

Auch eine falsche Parametereinstellung der Indikatoren kann zu Fehlsignalen führen. Die optimalen Parameter müssen durch wiederholtes Backtesting gefunden werden.

Darüber hinaus treten an den Aktienmärkten kurzfristig oft Black-Swan-Ereignisse auf, die zum Versagen der Indikatoren führen können. Um dieses Risiko zu mindern, kann eine Stop-Loss-Strategie integriert werden, um übermäßige Verluste pro Trade zu vermeiden.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen weiter optimiert werden:

- Hinzufügen weiterer Indikatorsignale, z. B. Volumenindikatoren, um die Trendstärke zu beurteilen und die Entscheidungsgenauigkeit zu erhöhen.

- Einsatz von maschinellen Lernmodellen, die auf den mehrdimensionalen Indikatoren trainiert werden, um automatisch die optimale Handelsstrategie zu finden.

- Optimierung der Parameter je nach Marktprodukt, Einführung adaptiver Parameter.

- Ergänzung einer Stop-Loss-Strategie und Steuerung der Positionsgröße basierend auf dem Drawdown, um das Risiko besser zu kontrollieren.

- Portfolioptimierung durch Kombination von Produkten mit geringer Korrelation, um den Drawdown des Portfolios zu reduzieren.

Zusammenfassung

Insgesamt eignet sich diese Strategie sehr gut für den kurzfristigen Trendhandel. Sie nutzt mehrdimensionale Indikatoren zur Entscheidungsfindung, filtert viele Störsignale heraus und erzielt eine hohe Trefferquote. Dennoch ist das Risiko von Fehlsignalen der Indikatoren zu beachten. Durch weitere Optimierungen hat diese Strategie das Potenzial, zu einer effizienten und stabilen Kurzfriststrategie zu werden.

- 1