Auf verallgemeinerter Unterstützung/Widerstand basierende Umkehr-Handelsstrategie

Überblick

Diese Strategie nutzt Umkehrhandel auf Basis von Long-Short-Faktoren und setzt gleichzeitig Zielgewinnpunkte. Der Kern der Long-Short-Faktoren ist die auf Handelsvolumen basierende erweiterte Formation „breite Unterstützung/Widerstand“, die für Instrumente mit hohem Handelsvolumen und Volatilität geeignet ist. Der Vorteil der Strategie liegt darin, dass sie große kurz- bis mittelfristige Trendumkehrmöglichkeiten erfassen und schnell Gewinne erzielen kann; es besteht jedoch auch das Risiko, in einer Position gefangen zu sein.

Strategieprinzip

-

Identifizierung von Long-Short-Faktoren mittels „breiter Unterstützung/Widerstand“ basierend auf Handelsvolumen

-

Verwendung von Kerzenformationen zur Erkennung klassischer Unterstützung/Widerstand, Filtern von Fehlausbrüchen durch hohes Volumen

-

Breite Unterstützung/Widerstand hat eine bessere Abdeckung als klassische Formationen

-

Ausbruch über breiten Widerstand ist ein Short-Faktor-Signal, Ausbruch unter breite Unterstützung ist ein Long-Faktor-Signal

-

-

Umkehrhandel

-

Nach Auslösung eines Faktorsignals wird eine gegensätzliche Position eröffnet

-

Bei bestehender Position wird entweder reduziert oder eine Gegenposition eröffnet

-

-

Festlegung von Gewinnzielen

-

Stop-Loss basierend auf ATR

-

Setzen mehrerer Zielgewinnpunkte wie 1R/2R/3R

-

Schrittweiser Positionsabbau bei Erreichen verschiedener Gewinnziele

-

Vorteilsanalyse

-

Erfassung größerer kurz- bis mittelfristiger Umkehrungen

Unterstützungs-/Widerstandsausbrüche stellen starke Trendumkehrsignale dar, die eine gewisse Zuverlässigkeit bieten und größere kurz- bis mittelfristige Umkehrungen erfassen können.

-

Schnelle Gewinnerzielung, geringe Drawdowns

Durch Stop-Loss und mehrstufige Gewinnziele können schnelle Gewinne realisiert und die Einzelwert-Drawdowns begrenzt werden.

-

Geeignet für Instrumente mit hohem institutionellem Kapitaleinsatz und hoher Volatilität

Die Strategie ist auf Volumenindikatoren angewiesen und benötigt ausreichend institutionelle Kapitalzuflüsse zur Unterstützung des Trends; gleichzeitig ist eine gewisse Volatilitätsspanne für die Gewinnerzielung erforderlich.

Risikoanalyse

-

Risiko, in Seitwärtsbewegungen gefangen zu werden

Bei Seitwärtsbewegungen kann das Verhalten, aus dem Stop-Loss auszusteigen und dann wieder in die Gegenrichtung einzusteigen, zu häufigem Gefangenwerden führen.

-

Risiko des Versagens von Unterstützung/Widerstand

Breite Unterstützung/Widerstand sind nicht absolut zuverlässig; es besteht eine Wahrscheinlichkeit von Fehltests und Umkehrungen.

-

Risiko einer einseitigen Position

Die Strategie ist reiner Umkehrhandel, berücksichtigt keine Trendfolge und könnte größere trendgerichtete Chancen verpassen.

-

Risikomanagement

-

Die Faktorbedingungen für Umkehrgeschäfte können gelockert werden; nicht jeder Ausbruch muss umgekehrt werden

-

Kombination mit anderen Indikatoren zur Filterung, z. B. Divergenz zwischen Preis und Volumen

-

Optimierung der Stop-Loss-Strategie zur Verringerung der Wahrscheinlichkeit, gefangen zu werden

-

Optimierungsmöglichkeiten

-

Optimierung der Parameter für die Breite

Optimierung der Parameter für breite Unterstützung/Widerstand zur Identifizierung zuverlässigerer Faktoren

-

Optimierung der Gewinnstrategie

Hinzufügen weiterer Gewinnziele oder Verwendung nicht-fester Ziele

-

Optimierung der Stop-Loss-Strategie

Anpassung der ATR-Parameter oder Verwendung eines IST-Ansatzes (z. B. Trailing Stop) zur Reduzierung unnötig aggressiver Stopps, die Handelskosten verursachen

-

Kombination mit Trend und anderen Faktoren

Einführung von Trendindikatoren wie gleitenden Durchschnitten, um starke Gegenläufigkeit zum Trend zu vermeiden; auch andere Hilfsfaktoren können einbezogen werden

Zusammenfassung

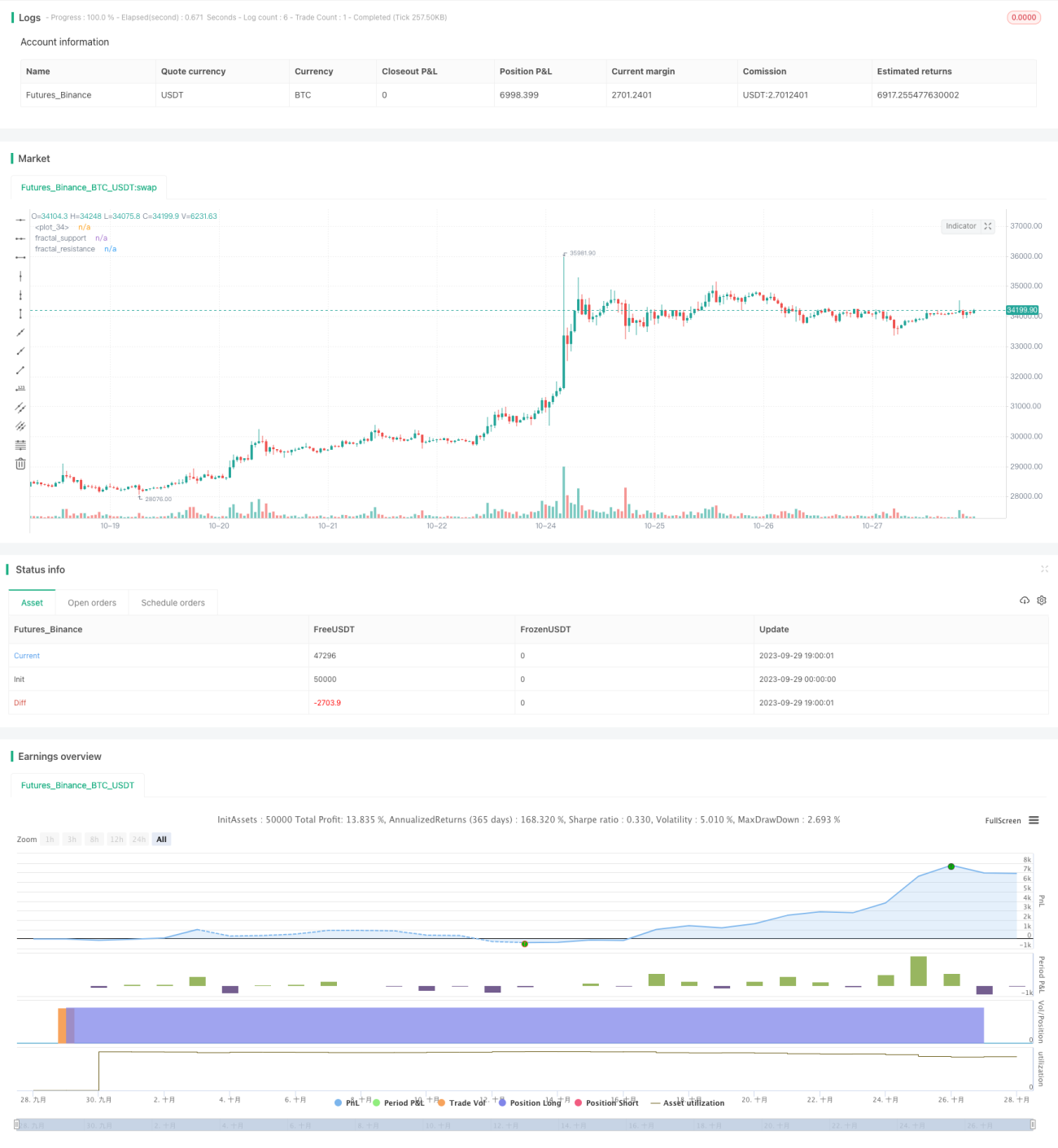

Der Kern dieser Strategie liegt darin, durch Umkehrhandel kurz- bis mittelfristige größere Schwankungen zu erfassen. Der Ansatz ist einfach und direkt; durch Parametereinstellungen können im Live-Handel gute Ergebnisse erzielt werden. Allerdings ist die Umkehrstrategie aggressiv und birgt gewisse Drawdown- und Fangrisiken, weshalb eine weitere Optimierung von Stop-Loss und Gewinnstrategie sowie die angemessene Einbeziehung von Trendurteilen erforderlich sind, um unnötige Verluste zu vermeiden.

- 1