Trendfolge-MA-Kreuzungshandelsstrategie

Überblick

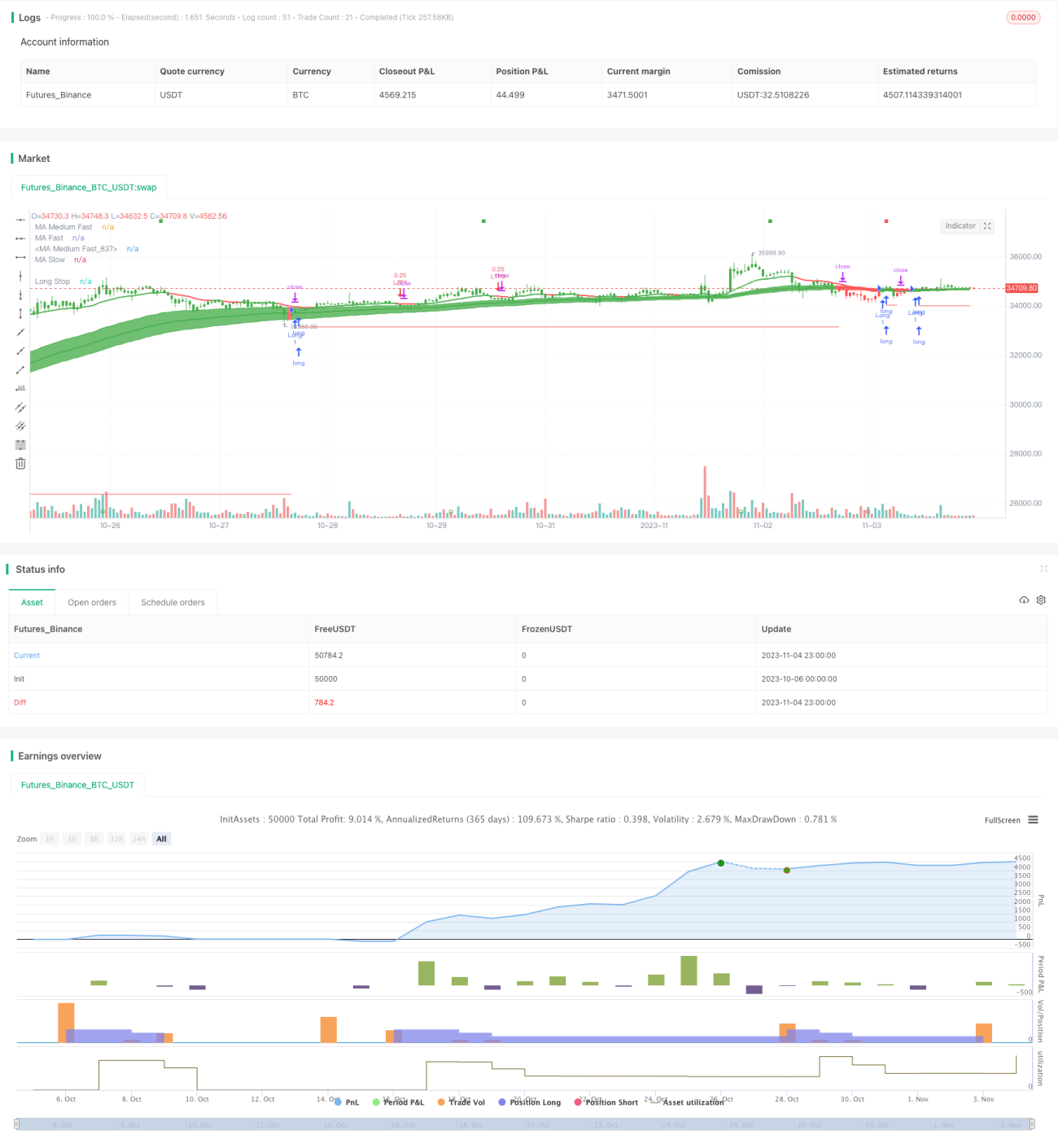

Diese Strategie ist eine trendfolgende Handelsstrategie basierend auf gleitenden Durchschnitten. Sie verwendet drei Hull Moving Averages mit unterschiedlichen Parametereinstellungen, um die Trendrichtung des Preises zu bestimmen. In Kombination mit einem schnellen ATR-Filter wird eine frühzeitige Erkennung potenzieller Trendumkehrungen ermöglicht. Wenn die drei gleitenden Durchschnitte (schnell, mittel, langsam) einen Aufwärts- oder Abwärts-Crossover bilden, werden Kauf- oder Verkaufssignale ausgelöst. Die Strategie verfügt außerdem über einen nachlaufenden Stop-Loss und einen nachlaufenden Take-Profit, um das Risiko effektiv zu kontrollieren.

Strategieprinzip

Die Strategie verwendet drei Hull Moving Averages zur Bestimmung der Preistrendrichtung: einen schnellen Hull MA, einen mittelschnellen Hull MA und einen langsamen Hull MA. Anhand ihrer Kreuzungen wird die Trendrichtung ermittelt:

-

Wenn der schnelle MA den mittleren MA von unten nach oben kreuzt, signalisiert dies einen Aufwärtstrend und löst ein Kaufsignal aus.

-

Wenn der schnelle MA den mittleren MA von oben nach unten kreuzt, signalisiert dies einen Abwärtstrend und löst ein Verkaufssignal aus.

Um die Empfindlichkeit bei der Erkennung von Trendumkehrungen zu erhöhen, wird ein auf dem RSI basierender schneller ATR-Filter eingeführt. Dieser Filter misst die Volatilität des Preises. Wenn sich der Preistrend ändert, ändert sich sein Wert deutlich. Daher können wir anhand des Durchbruchs des ATR-Filters nach oben oder unten eine Trendumkehr frühzeitig erkennen.

Konkret implementiert die filtr-Funktion die Berechnungslogik dieses schnellen ATR-Filters. Sie berechnet die ATR-Größe auf Basis des RSI-Werts. Wenn der ATR-Wert die RSI-Kurve nach oben oder unten durchbricht, könnte dies eine Trendwende des Preises ankündigen.

Darüber hinaus sind in der Strategie nachlaufende Stop-Loss- und Take-Profit-Bedingungen festgelegt, die eine automatische Risikosteuerung basierend auf den festgelegten Stop-Loss- und Take-Profit-Prozentsätzen ermöglichen.

Vorteile

- Die Verwendung von drei Hull-MA-Linien zur Bestimmung der Trendrichtung filtert Marktrauschen effektiv heraus und identifiziert mittel- bis langfristige Trends.

- Die Anwendung des schnellen ATR-Filters verbessert die Fähigkeit, Trendumkehrungen frühzeitig zu erkennen.

- Automatisches Erkennen von Trendwendechancen, rechtzeitige Positionsanpassung ohne Verpassen von Käufen oder Verkäufen.

- Nachlaufende Stop-Loss- und Take-Profit-Einstellungen schaffen ein dynamisches Gleichgewicht zwischen Risiko und Ertrag.

- Anpassbare Parameter, geeignet für verschiedene Märkte und Handelsinstrumente.

Risikoanalyse

- MA-Crossover-Strategien neigen zu falschen Long- und Short-Signalen, weshalb der ATR-Filter zur Bestätigung erforderlich ist.

- In stark schwankenden Märkten kann es zu häufigen MA-Überkreuzungen kommen; die ATR-Kurve sollte genau beobachtet werden.

- Ein zu enger Stop-Loss kann zu vorzeitigen Ausstiegen führen, ein zu weiter Stop-Loss erschwert die Verlustkontrolle. Parameter müssen je nach Situation angepasst werden.

- Diese Strategie eignet sich besser für trendende Märkte, nicht für Seitwärtsmärkte.

- Durch Parameteroptimierung können die besten MA- und ATR-Periodenkombinationen gefunden werden, um die Fehlsignalrate zu reduzieren.

Optimierungsmöglichkeiten

- Der MA-Typ könnte auf DEMA, TEMA oder andere EMA-Varianten geändert werden, um mehr Rauschen zu filtern.

- Der ATR-Filter könnte durch die MIDDLE-Linie des Keltner-Kanals ersetzt werden, um die Erkennung von Trendumkehrungen zu überprüfen.

- Verschiedene MA-Parameterkombinationen könnten getestet werden, um das optimale Parameterpaar zu finden.

- Die ATR-Periode könnte getestet werden, um die beste Glättungswirkung zu erzielen.

- Volumenindikatoren könnten hinzugefügt werden, um die Wahrscheinlichkeit eines echten Ausbruchs zu bewerten.

- Das Hinzufügen anderer Indikatoren wie MACD könnte getestet werden, um die Zuverlässigkeit der Signale zu erhöhen.

Zusammenfassung

Diese Strategie integriert mehrere Funktionen: gleitende Durchschnitte zur Trendbestimmung, einen ATR-Filter zur frühzeitigen Erkennung von Umkehrungen sowie automatische Stop-Loss- und Take-Profit-Management zur Risikosteuerung. Sie kann Trends automatisch verfolgen, Wendepunkte rechtzeitig nutzen und durch Parameteroptimierung an verschiedene Instrumente und Zeitrahmen angepasst werden. Es handelt sich um eine sehr praktische trendfolgende Handelsstrategie. Ihre Vorteile sind die einfache und klare Logik sowie effiziente Risikokontrollmechanismen. Es ist jedoch wichtig, auf falsche Signale und die korrekte Einstellung von Stop-Loss-Punkten zu achten. Durch weitere Optimierung kann eine noch bessere Strategieleistung erzielt werden.

- 1