Umfassende automatisierte Moving-Average-Regenbogen-Strategie

Übersicht

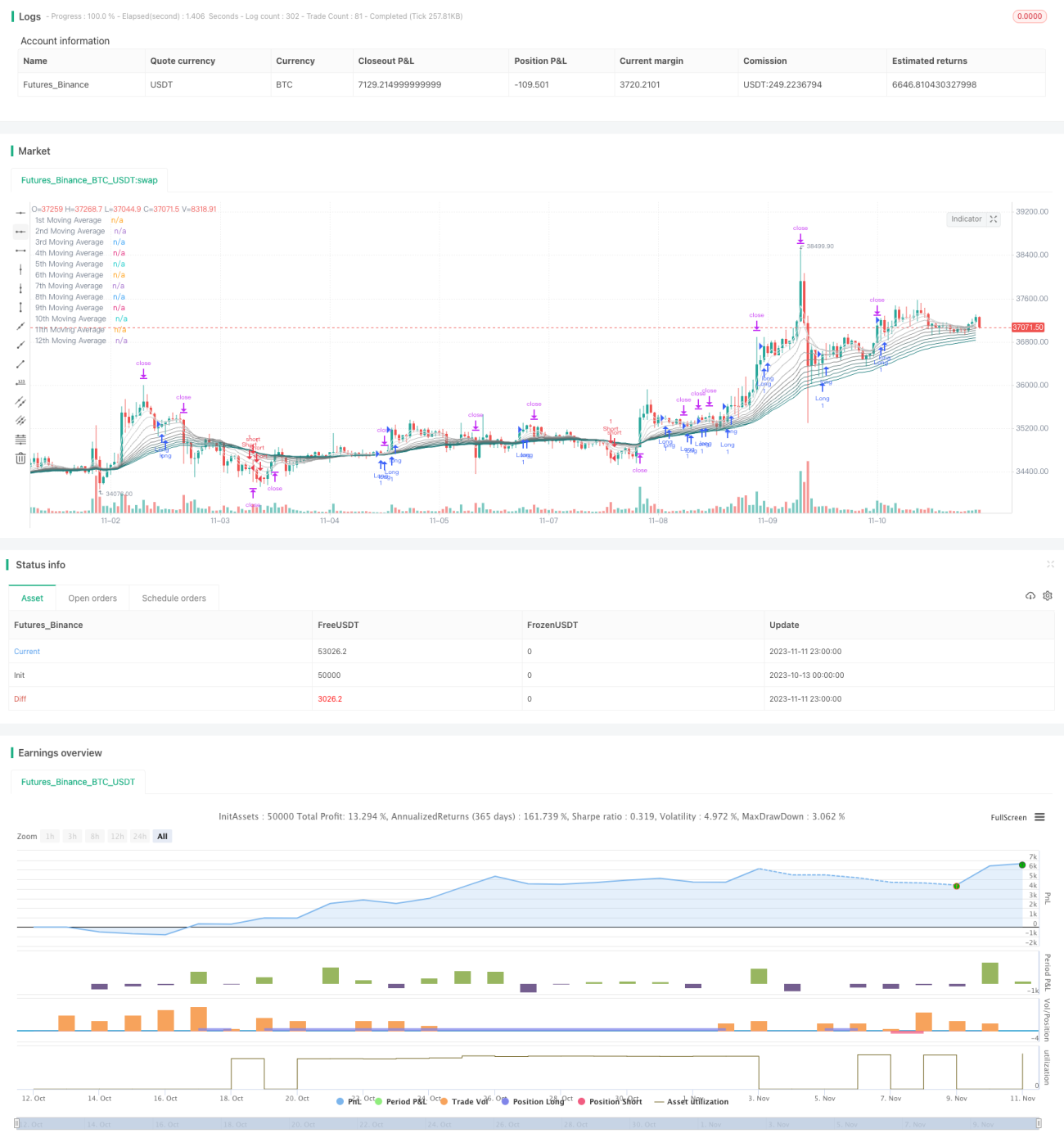

Die Allround-Autotrading-Moving-Average-Regenbogenstrategie ist eine typische Multi-Zeitrahmen-Kombinationsstrategie aus gleitenden Durchschnitten. Sie verwendet 12 gleitende Durchschnitte mit unterschiedlichen Perioden und analysiert die Anordnung der gleitenden Durchschnitte sowie deren Verhältnis zum Preis, um die Marktrichtung zu bestimmen sowie Positionseröffnungen, Stop-Loss und Take-Profit zu definieren. Die Strategie kann Trends automatisch erkennen und verfügt über ein umfassendes Stop-Loss-Management zur Risikokontrolle.

Prinzip

Die Strategie verwendet 12 gleitende Durchschnitte mit Perioden von 3, 5, 8 bis zu 55. Der Typ der gleitenden Durchschnitte kann EMA, SMA, RMA usw. sein. Die Strategie bewertet zunächst die Anordnung der kurzfristigen und langfristigen gleitenden Durchschnitte (Linien der Perioden 1-4 und Linien der Perioden 5-8). Liegen die kurzfristigen über den langfristigen, wird ein Aufwärtstrend angenommen; liegen sie darunter, ein Abwärtstrend.

Im Aufwärtstrend wird ein Long-Einstiegssignal erkannt, wenn der Preis den gleitenden Durchschnitt des vorherigen Tiefs durchbricht. Der Stop-Loss liegt auf dem gleitenden Durchschnitt des vorherigen Tiefs, der Take-Profit beträgt das 1,6-Fache des Stop-Loss-Abstands. Im Abwärtstrend wird ein Short-Einstiegssignal erkannt, wenn der Preis den gleitenden Durchschnitt des vorherigen Hochs durchbricht. Der Stop-Loss liegt auf dem gleitenden Durchschnitt des vorherigen Hochs, der Take-Profit beträgt das 1,6-Fache des Stop-Loss-Abstands.

Die Strategie verfügt auch über eine Trendwende-Erkennung. Während einer offenen Position wird, wenn sich die Anordnung der kurzfristigen gleitenden Durchschnitte ändert und der Preis das letzte Hoch oder Tief überschreitet, eine mögliche Trendwende angenommen. In diesem Fall wird die aktuellen Position geschlossen und eine gegenläufige Position eröffnet, wobei das neue Hoch oder Tief als Stop-Loss und Take-Profit dient.

Vorteile

-

Die Strategie nutzt mehrere Zeitrahmen-Analysen und kann Trendrichtungen gut einschätzen.

-

Sie berücksichtigt die gleich- oder gegenläufige Anordnung der gleitenden Durchschnitte, um Fehlsignale in Seitwärtsmärkten zu vermeiden.

-

Sie verfügt über ein umfassendes Stop-Loss-Management, das das Risiko einzelner Trades effektiv begrenzt.

-

Die Trendwende-Erkennung ermöglicht es, Trendwechsel rechtzeitig zu erfassen und systemische Risiken zu reduzieren.

-

Die Parameter sind flexibel einstellbar – sowohl die Perioden als auch die Typen der gleitenden Durchschnitte können individuell angepasst werden.

-

Die Strategie verwendet einen nachgeführten Stop-Loss (Trailing Stop), um Gewinne bestmöglich zu sichern.

Risiken

-

Bei einer Kombination mehrerer gleitender Durchschnitte beeinflusst die Parametereinstellung die Performance; Optimierungstests sind erforderlich.

-

In Seitwärtsmärkten können gleitende Durchschnitte Fehlsignale erzeugen; Parameter sollten angepasst oder der Handel ausgesetzt werden.

-

Es besteht eine gewisse Verzögerung, sodass in der Nähe von Trendwendepunkten Chancen verpasst werden können.

-

Andere technische Indikatoren sollten beachtet werden, um nicht in der Nähe wichtiger Unterstützungszonen Short-Positionen zu eröffnen.

-

Systemische Risiken müssen berücksichtigt werden; die Trendwende-Erkennung kann diese nicht vollständig vermeiden.

-

Zur Drawdown-Kontrolle sollten zusätzliche Mechanismen wie dynamisches Positionsmanagement hinzugefügt werden.

Optimierungsmöglichkeiten

-

Testen verschiedener Typen gleitender Durchschnitte und Parametereinstellungen, um die beste Kombination zu finden.

-

Optimierung der Trendwende-Erkennung mit präziseren Auslösebedingungen.

-

Integration eines dynamischen Positionsmanagements, um die Positionsgröße bei zu großen Drawdowns zu reduzieren.

-

Einsatz von Machine-Learning-Algorithmen, um mithilfe großer Datenmengen wichtige Punkte zu identifizieren.

-

Kombination mit anderen Indikatorsignalen zur Verbesserung der Entscheidungsgenauigkeit.

-

Aufbau eines Multi-Asset-Portfolios, um durch unkorrelierte Beziehungen Risiken zu streuen.

Zusammenfassung

Die Allround-Autotrading-Moving-Average-Regenbogenstrategie ist insgesamt eine solide Trendfolgestrategie mit starker Trenderkennungs- und Risikokontrollfähigkeit. Durch Parameteroptimierung und die Integration dynamischen Positionsmanagements kann sie zu einer sehr praktischen quantitativen Handelsstrategie weiterentwickelt werden. Die Strategie ist klar und verständlich und bietet dennoch ausreichend Flexibilität, sodass eine eingehende Untersuchung, Nutzung und kontinuierliche Optimierung lohnenswert ist.

- 1