Doppel-EMA Golden-Cross Trendfolgestrategie

Überblick

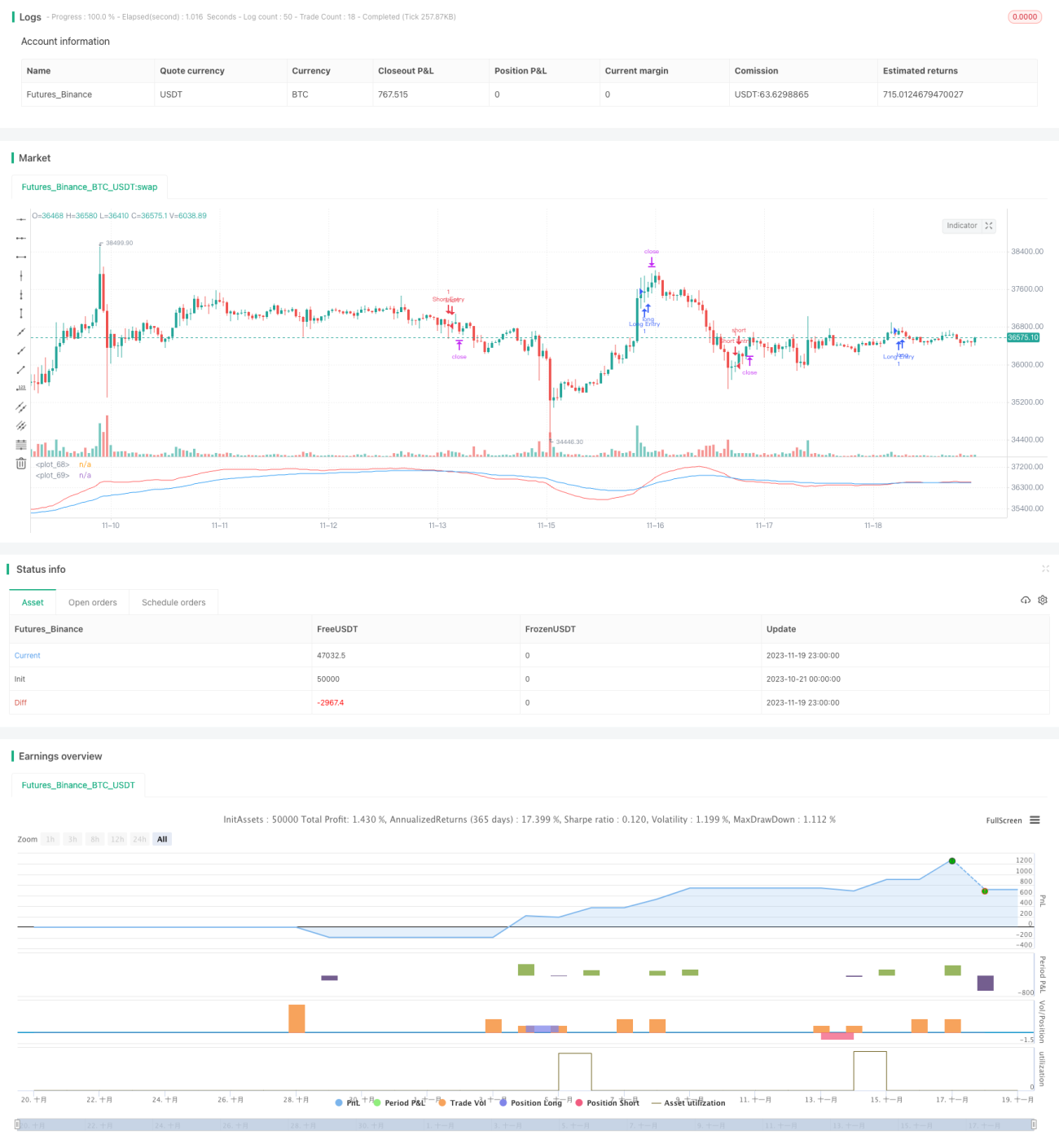

Diese Strategie bestimmt die Markttrendrichtung durch die Berechnung einer schnellen EMA und einer langsamen EMA sowie den Vergleich der Größenverhältnisse der beiden EMAs. Es handelt sich um eine einfache Trendfolgestrategie. Wenn die schnelle EMA die langsame EMA nach oben kreuzt, wird eine Long-Position eröffnet; wenn die schnelle EMA die langsame EMA nach unten kreuzt, wird eine Short-Position eröffnet. Es ist die klassische doppelte EMA-Golden-Cross-Strategie.

Strategieprinzip

Der Kernindikator dieser Strategie sind die schnelle EMA und die langsame EMA. Die Länge der schnellen EMA ist auf 21 Perioden eingestellt, die Länge der langsamen EMA auf 55 Perioden. Die schnelle EMA reagiert schneller auf Preisänderungen und spiegelt die kurzfristige Tendenz wider; die langsame EMA reagiert träger auf Preisänderungen, filtert Rauschen heraus und spiegelt den mittel- bis langfristigen Trend wider.

Wenn die schnelle EMA die langsame EMA nach oben kreuzt, zeigt dies an, dass der kurzfristige Trend auf einen Aufwärtstrend umschwenkt und der mittel- bis langfristige Trend möglicherweise einen Wendepunkt erreicht – dies ist ein Long-Signal. Wenn die schnelle EMA die langsame EMA nach unten kreuzt, zeigt dies an, dass der kurzfristige Trend auf einen Abwärtstrend umschwenkt und der mittel- bis langfristige Trend möglicherweise einen Wendepunkt erreicht – dies ist ein Short-Signal.

Durch den Vergleich der schnellen und langsamen EMA können Trendwenden auf kurzer und mittel- bis langfristiger Zeitebene erfasst werden. Es handelt sich um eine typische Trendfolgestrategie.

Strategievorteile

- Einfacher und klarer Ansatz, leicht verständlich und umsetzbar

- Flexible Parametereinstellung: Die Perioden der schnellen und langsamen EMA können individuell angepasst werden

- Konfigurierbarer ATR-Stop-Loss und Take-Profit für kontrolliertes Risiko

Strategierisiken

- Der Zeitpunkt des doppelten EMA-Kreuzes kann suboptimal gewählt sein, es besteht das Risiko, den besten Einstiegspunkt zu verpassen

- In Seitwärtsmärkten können mehrfache Fehlsignale auftreten, was zu Verlusten führt

- Eine falsche Einstellung des ATR-Parameters kann zu zu weiten oder zu aggressiven Stop-Loss- und Take-Profit-Niveaus führen

Maßnahmen zur Risikobewältigung:

- Optimierung der Parameter für schnelle und langsame EMA, um die optimale Parameterkombination zu finden

- Hinzufügen von Filtermechanismen, um Fehlsignale in Seitwärtsmärkten zu vermeiden

- Testen und Optimieren des ATR-Parameters, um angemessene Stop-Loss- und Take-Profit-Niveaus sicherzustellen

Optimierungsmöglichkeiten

- Statistische Tests der Stabilität verschiedener EMA-Parameterkombinationen

- Hinzufügen von Filtern, kombiniert mit anderen Indikatoren zur Vermeidung von Fehlsignalen

- Optimierung des ATR-Parameters für das beste Verhältnis von Stop-Loss zu Take-Profit

Zusammenfassung

Diese Strategie nutzt das Kreuzen der schnellen EMA und der langsamen EMA zur Bestimmung des Markttrends. Sie ist einfach, klar und leicht umsetzbar. Gleichzeitig wird ATR zur Festlegung von Stop-Loss und Take-Profit verwendet, um das Risiko zu kontrollieren. Durch Parameteroptimierung und Hinzufügen von Filtern kann die Stabilität und Rentabilität der Strategie weiter gesteigert werden.

- 1