PMax-adaptive Breakout-Strategie basierend auf RSI- und T3-Indikatoren

Übersicht

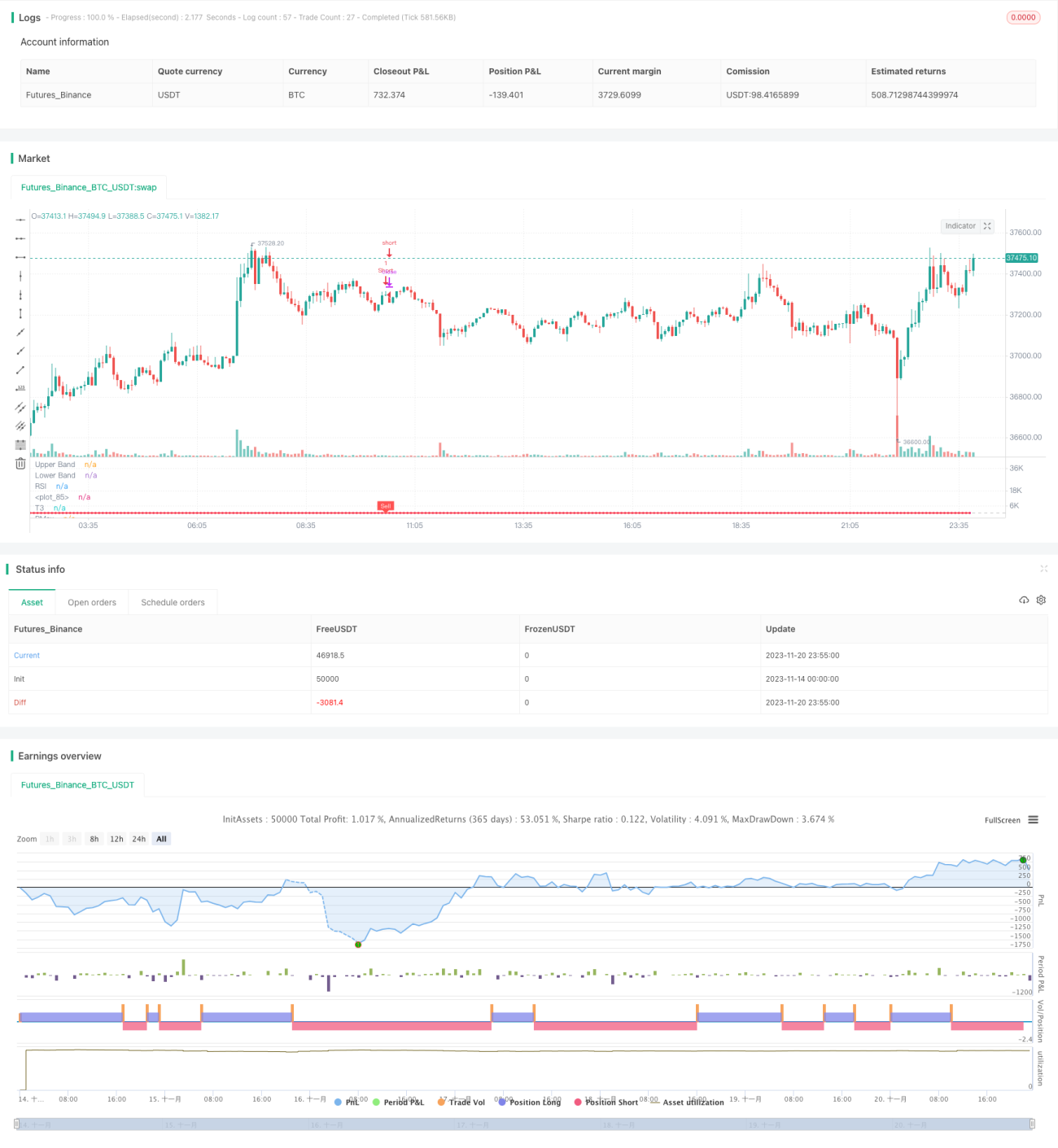

Diese Strategie ist ein quantitativer Handelsansatz, der RSI- und T3-Indikatoren zur Trendbestimmung nutzt und in Kombination mit dem ATR-Indikator eine Stop-Loss-Linie festlegt, um einen adaptiven PMax-Breakout zu realisieren. Die Kernidee besteht darin, die Trendbewertung und die Stop-Loss-Setzung zu optimieren, um Risiken zu kontrollieren und gleichzeitig die Rentabilität zu steigern.

Strategieprinzip

-

Berechnung von RSI und T3 zur Trendbestimmung

- Nutzung des RSI-Indikators zur Beurteilung, ob eine Aktie überkauft oder überverkauft ist.

- Berechnung des T3-Indikators auf Basis des RSI zur Trendanalyse.

-

Festlegung der adaptiven PMax-Stop-Loss-Linie anhand des ATR-Indikators

- Berechnung des ATR-Indikators als Maß für die Volatilität.

- Setzen einer Stop-Loss-Linie ober- und unterhalb des T3-Indikators, wobei die Linienbreite ein bestimmtes Vielfaches des ATR-Indikators beträgt.

- Ermöglichung einer adaptiven Anpassung der Stop-Loss-Linie.

-

Breakout-Kauf und Stop-Loss-Ausstieg

- Ein Kaufsignal wird erkannt, wenn der Kurs den T3-Indikator von unten nach oben durchbricht.

- Ein Ausstieg aus der aktuellen Position erfolgt, wenn der Kurs die Stop-Loss-Linie von oben nach unten durchbricht.

Vorteile der Strategie

Die Strategie bietet vor allem folgende Vorteile:

- Die Kombination von RSI- und T3-Indikatoren zur Trendbestimmung bietet eine hohe Genauigkeit.

- Der adaptive PMax-Stopp-Mechanismus kontrolliert das Risiko.

- Der ATR-Indikator als Volatilitätsmaß legt die Breite der Stop-Loss-Linie fest und vermeidet zu aggressive Einstellungen.

- Sowohl Drawdown als auch Rentabilität werden ausgewogen berücksichtigt.

Risiken der Strategie

Die Strategie birgt vor allem folgende Risiken:

-

Umkehrrisiko

Bei einer kurzfristigen Preisumkehr kann der Stop-Loss ausgelöst werden, was zu Verlusten führt. Eine lockere Einstellung der Stop-Loss-Linie kann die Auswirkungen von Umkehrungen verringern.

-

Risiko einer fehlgeschlagenen Trendbestimmung

Die Trendbestimmung mit RSI und T3 ist nicht zu 100 % zuverlässig. Bei Fehleinschätzungen kann es ebenfalls zu Verlusten kommen. Eine Anpassung der Parameter oder die Einbeziehung weiterer Indikatoren zur Optimierung ist möglich.

Optimierungsmöglichkeiten der Strategie

Die Strategie kann in folgenden Bereichen weiter optimiert werden:

- Einbeziehung von gleitenden Durchschnitten oder anderen Indikatoren zur Unterstützung der Trendbestimmung.

- Optimierung der Längenparameter von RSI und T3.

- Testen verschiedener ATR-Vielfacher als Breite der Stop-Loss-Linie.

- Anpassung des Spielraums der Stop-Loss-Linie je nach Marktbedingungen.

Zusammenfassung

Diese Strategie integriert die Stärken der drei Indikatoren RSI, T3 und ATR und realisiert so eine organische Kombination von Trendbestimmung und Risikokontrolle. Im Vergleich zu einem einzelnen Indikator zeichnet sich diese Kombination durch eine hohe Bestimmungsgenauigkeit und eine gute Drawdown-Kontrolle aus. Sie stellt eine zuverlässige Trendfolgestrategie dar. Es gibt noch Optimierungsspielraum bei Parametern und Risikomanagement. Insgesamt handelt es sich um eine empfehlenswerte quantitative Handelsstrategie.

/*backtest

start: 2023-11-14 00:00:00

end: 2023-11-21 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © KivancOzbilgic

//developer: @KivancOzbilgic- 1