Quantitative Trendfolgestrategie basierend auf SAR

Überblick

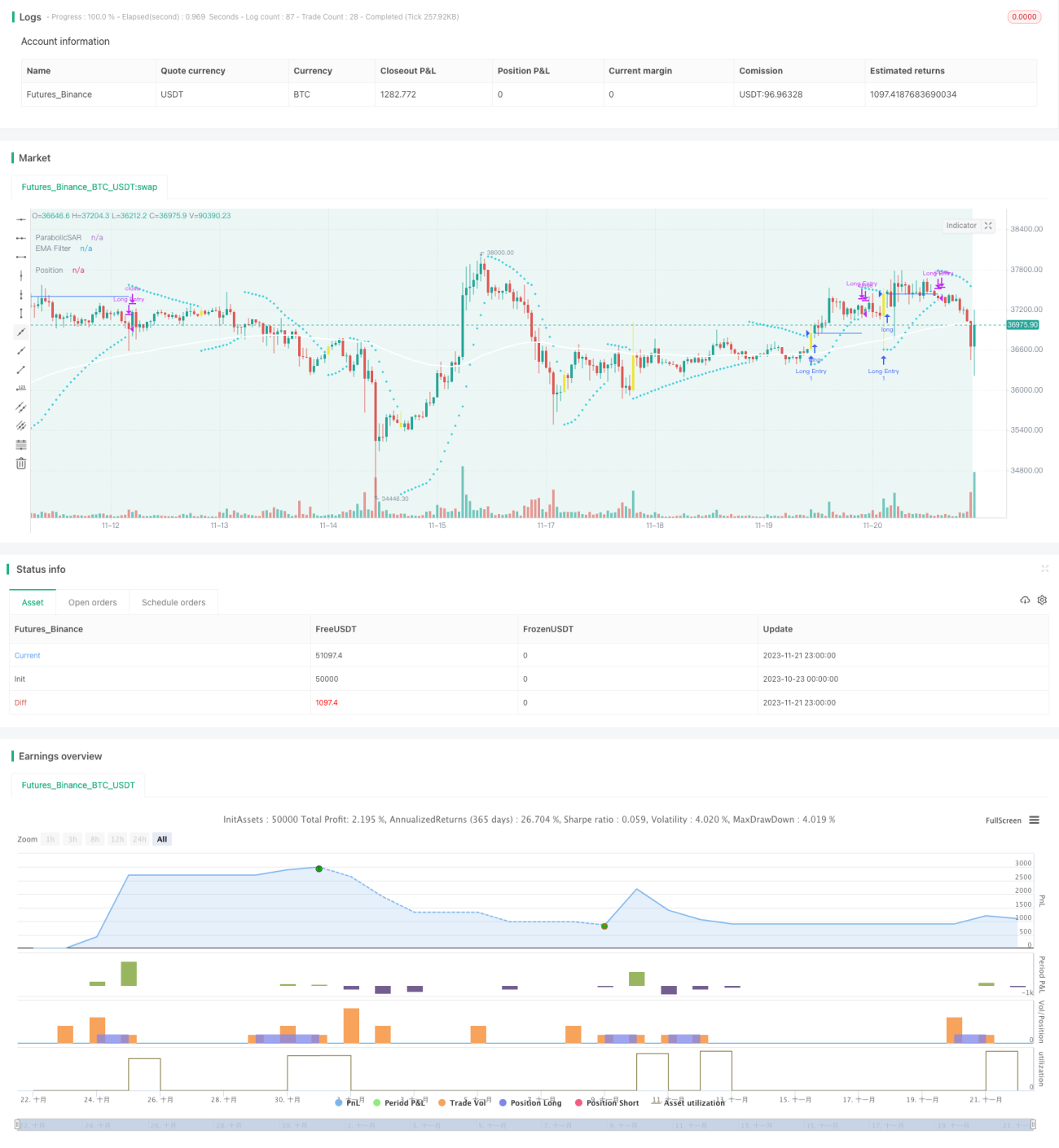

Die Spekulationslücken-Strategie ist eine trendfolgende quantitative Handelsstrategie, die die SAR-Glättungskurve als primäres Handelssignal verwendet und durch mehrere Filter wie EMA, Squeeze-Momentum und Volatilitätsoszillator ergänzt wird. Durch die Konfiguration der SAR-Parameter werden Trendumkehrpunkte identifiziert, um eine risikoarme Trendfolge zu ermöglichen. Diese Strategie eignet sich besonders für mittel- bis langfristige Anlagen.

Strategieprinzip

Die Strategie verwendet den Parabolic SAR als primäres Handelssignal. Der SAR kann effektiv Trendumkehrpunkte des Kurses erkennen: Wenn sich das SAR-Vorzeichen ändert, deutet dies auf eine Trendwende hin. Die Strategie gibt in der Regel Kauf- oder Verkaufssignale bei einer SAR-Umkehrung.

Zusätzlich bietet die Strategie eine SAR-Durchbruchsoption: Ein Signal wird bereits erzeugt, bevor der SAR vollständig umkippt, wenn der Kurs den letzten SAR-Wert durchbricht. Dies erhöht die Sensitivität der Strategie.

Um Fehlsignale zu filtern, werden drei zusätzliche Hilfsfilter verwendet: EMA, Squeeze-Momentum und Volatilitätsoszillator. Diese können einzeln oder in Kombination eingesetzt werden, um die Zuverlässigkeit von Preistrend und Handelssignal zu bestätigen.

Schließlich bietet die Strategie drei Arten von Stop-Loss- und Take-Profit-Methoden: festen Stop-Loss, festen Take-Profit sowie Stop-Loss basierend auf dem Risiko-Ertrags-Verhältnis. Dadurch kann die Strategie flexibel an die Eigenschaften verschiedener Handelsinstrumente angepasst werden.

Vorteilsanalyse

-

Der SAR kann Trendumkehrungen des Kurses präzise erkennen und neue Trends rechtzeitig erfassen, ideal für mittel- bis langfristige Trendfolge.

-

Mehrere Filter reduzieren die Wahrscheinlichkeit von Fehlausbrüchen und erhöhen die Signalzuverlässigkeit.

-

Einfache und flexible Konfiguration mit anpassbaren Parametern für verschiedene Handelsinstrumente.

-

Verschiedene Take-Profit- und Stop-Loss-Methoden ermöglichen ein ausgewogenes Risiko-Ertrags-Verhältnis.

-

Direkte Anbindung an Handelsroboter für automatisierten Handel möglich.

Risikoanalyse

-

In nicht-trendenden Märkten können vermehrt Fehlsignale und ineffektive Trades auftreten.

-

Ungünstige SAR-Parametereinstellungen können die Signalgenauigkeit beeinträchtigen.

-

Als Trendfolgestrategie kann bei stark volatilen Märkten leicht das Stop-Loss-Niveau erreicht werden.

Um diese Risiken zu mindern, können die SAR-Parameter oder Filterparameter angepasst werden, um die Wahrscheinlichkeit ineffektiver Trades zu verringern. Auch eine großzügigere Stop-Loss-Einstellung kann helfen, größere Kursschwankungen auszuhalten.

Optimierungsmöglichkeiten

-

SAR-Parameteroptimierung: Durch historische Backtest-Daten können die Schrittweite und der Inkrementparameter des SAR optimiert werden, um eine stabilere und effizientere Handelsstrategie zu erhalten.

-

Einführung von Trendindikatoren: Zusätzliche Indikatoren wie MACD, DMI können zur besseren Trendbewertung hinzugefügt werden.

-

Optimierung des Risiko-Ertrags-Verhältnisses: Anpassung der festen Take-Profit- und Stop-Loss-Prozentsätze sowie des Risiko-Ertrags-Verhältnisses, um bei entsprechend höherem Risiko höhere Gewinne zu erzielen.

-

Erweiterung auf Devisen: Die Strategie unterstützt derzeit nur den Handel mit Kryptowährungen. Eine Erweiterung auf Devisen, Rohstoffe und Aktienmärkte ist möglich.

Zusammenfassung

Die Spekulationslücken-Strategie ist eine äußerst praktische trendfolgende quantitative Strategie. Sie reagiert sensibel, liefert zuverlässige Signale und kann durch Stop-Loss- und Take-Profit-Management langfristig stabile Erträge erzielen. Durch geeignete Parameter- und Regeloptimierung lässt sich die Effizienz weiter steigern. Es handelt sich um eine effiziente quantitative Strategie, die langfristig eingesetzt werden kann.

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//VERSION =================================================================================================================

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// This strategy is intended to study.- 1