Multi-Timeframe SuperTrend Oszillator-Ausbruchsstrategie

Überblick

Diese Strategie kombiniert den Super-Trend-Indikator über mehrere Zeitrahmen mit Bollinger-Bändern, um Trendrichtung und wichtige Unterstützungs-/Widerstandsniveaus zu identifizieren. Bei Ausbrüchen aus der Seitwärtsbewegung werden Einstiege getätigt, und Positionen werden basierend auf Überkreuzungen verlassen. Die Strategie eignet sich hauptsächlich für stark volatile Rohstoff-Futures wie Gold, Silber, Rohöl usw.

Strategieprinzip

Basierend auf der in Pine Script geschriebenen benutzerdefinierten Multi-Timeframe-Super-Trend-Funktion pine_supertrend() wird in Kombination mit dem Super-Trend verschiedener Zeiträume (z. B. 1 Minute und 5 Minuten) die Trendrichtung des größeren Zeitrahmens bestimmt.

Gleichzeitig werden die oberen und unteren Bänder der Bollinger-Bänder berechnet, um Kanalausbrüche zu beurteilen. Wenn der Preis das obere Bollinger-Band durchbricht, wird ein bullischer Ausbruch angenommen; wenn der Preis das untere Bollinger-Band unterschreitet, ein bärischer.

Strategiesignale:

- Long-Signal: Schlusskurs > oberes Bollinger-Band UND Schlusskurs > Multi-Timeframe-Super-Trend-Indikator

- Short-Signal: Schlusskurs < unteres Bollinger-Band UND Schlusskurs < Multi-Timeframe-Super-Trend-Indikator

Stop-Loss:

- Long-Stop-Loss: Schlusskurs < 5-Minuten-Super-Trend-Indikator

- Short-Stop-Loss: Schlusskurs > 5-Minuten-Super-Trend-Indikator

Somit erfasst die Strategie die Resonanzausbrüche von Super-Trend und Bollinger-Bändern und handelt in Phasen hoher Volatilität.

Vorteilsanalyse

- Nutzung des Multi-Timeframe-Super-Trends zur Bestimmung der Trendrichtung großer Zeitrahmen, wodurch die Signalqualität verbessert wird.

- Die oberen und unteren Bollinger-Bänder dienen als wichtige Unterstützungs-/Widerstandszonen und reduzieren Fehlausbrüche.

- Der Super-Trend als Stop-Loss-Level reduziert Verluste und kontrolliert das Risiko.

Risikoanalyse

- Der Super-Trend-Indikator weist eine Verzögerung auf und kann Trendwenden verpassen.

- Ungünstige Parameter der Bollinger-Bänder können zu zu häufigen oder zu seltenen Trades führen.

- Bei Nachtzeiten von Rohstoff-Futures oder wichtigen Ereignissen können starke Preisschwankungen auftreten, die leicht zu einem Stop-Loss führen.

Lösungsansätze für Risiken:

- Kombination mit mehreren Hilfsindikatoren zur Bestätigung von Signalen, um Fehlausbrüche zu vermeiden.

- Optimierung der Bollinger-Band-Parameter, um den optimalen Gleichgewichtspunkt zu finden.

- Anpassung der Stop-Loss-Positionen, um den Abstand zu vergrößern.

Optimierungsrichtung

- Ausprobieren anderer Trendindikatoren wie KDJ, MACD usw. als zusätzliche Bestätigung.

- Einbeziehung von maschinellen Lernmodellen zur Wahrscheinlichkeitsbewertung als Unterstützung.

- Parametoptimierung, um die beste Kombination von Hyperparametern zu finden.

Zusammenfassung

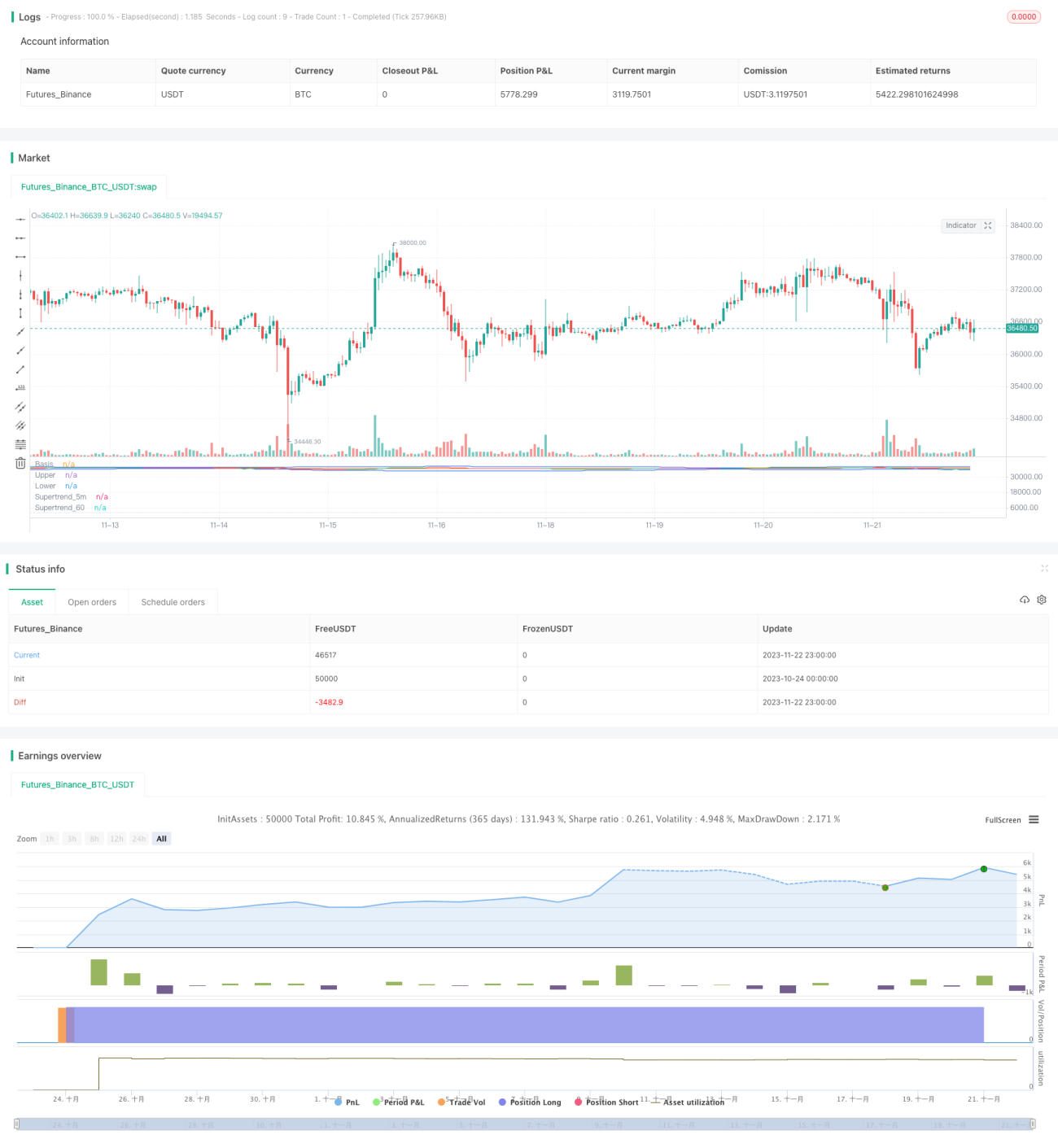

Die Strategie integriert die beiden effizienten Indikatoren Super-Trend und Bollinger-Bänder und erzielt durch Analyse über verschiedene Zeitrahmen sowie Ausbruchserkennung aus Kanälen eine hohe Wahrscheinlichkeit für erfolgreiche Positionen. Die Strategie kontrolliert effektiv das Kapitalrisiko und hat gezeigt, dass sie bei stark volatilen Produkten gute Renditen erzielen kann. Durch weitere Optimierung und Kombination mit zusätzlichen Indikatoren kann die Effektivität der Strategie weiter gesteigert werden.

- 1