Hochfrequenz-Quantitative-Handelsstrategie auf Basis doppelter Filterung

Überblick

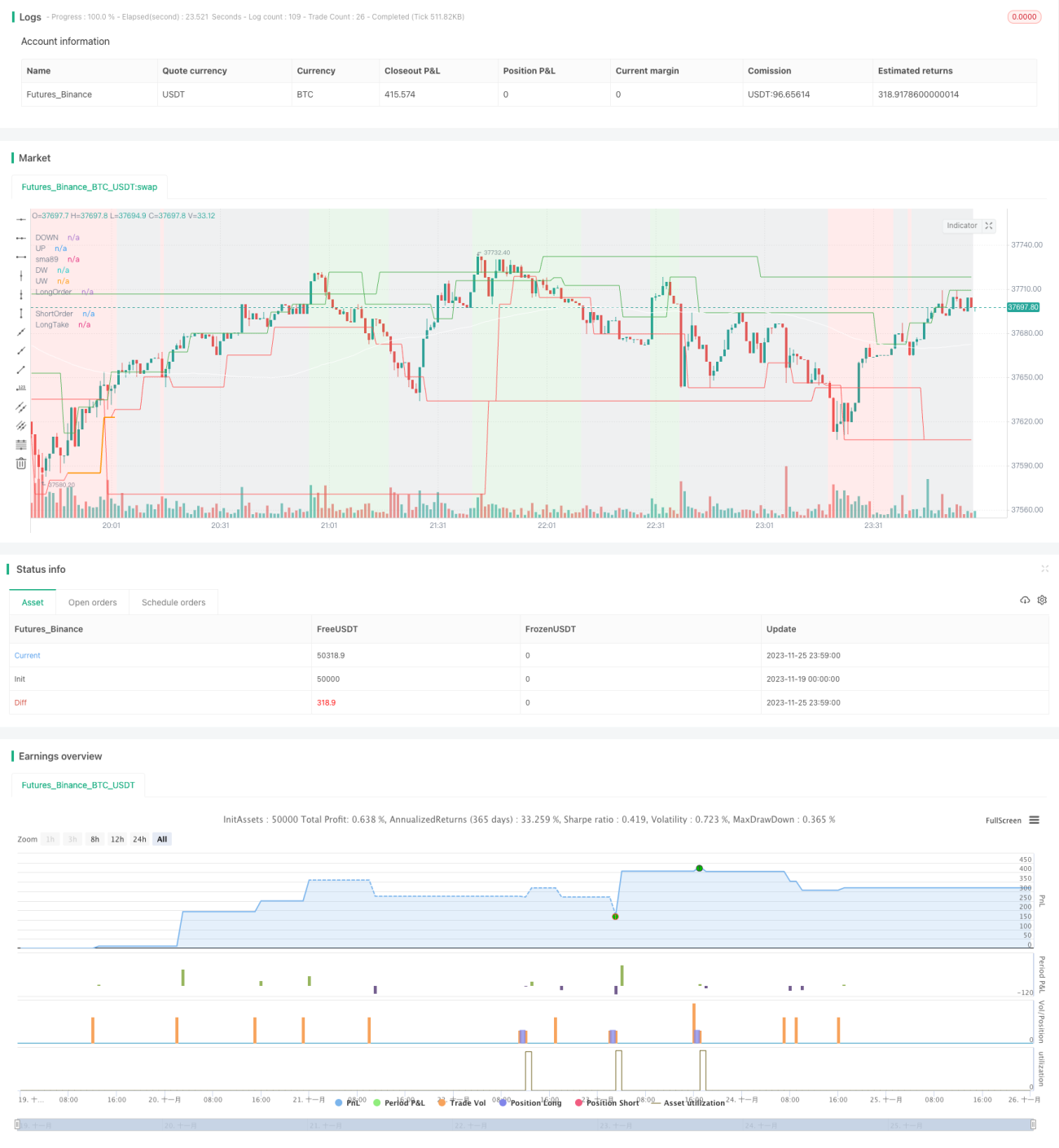

Der Name dieser Strategie lautet „Quantitativer Doppelfilter“. Sie nutzt mehrere Zeitrahmen und realisiert eine hochfrequente quantitative Handelsstrategie, die auf dem Konzept der doppelten Filterung basiert. Die Strategie verwendet Indikatoren auf verschiedenen Zeitrahmen für die Bewertung und ermöglicht so eine strengere Filterung von Handelssignalen. Dadurch werden zahlreiche Fehlsignale ausgefiltert und eine höhere Gewinnrate erzielt.

Strategieprinzip

Das Kernprinzip der Strategie ist:

- Die Markttrendrichtung wird anhand von Wochen- und Tagescharts ermittelt und dient als Filter für die Strategierichtung – gehandelt wird nur, wenn die Trendbedingungen erfüllt sind.

- Auf dem 4-Stunden-Chart werden Kanäle gebildet, um Verkaufs- und Kaufsignale zu identifizieren und Handelssignale zu generieren.

- Die Übereinstimmung der Richtungen von Wochen-, Tages- und 4-Stunden-Chart filtert viele Fehlsignale aus und erhöht die Zuverlässigkeit der Handelssignale.

- Fibonacci-Retracement-Levels dienen zur Festlegung von Take-Profit und Stop-Loss, um schnelle Gewinnmitnahmen und Verlustbegrenzungen zu ermöglichen.

Konkret wird zunächst auf dem Wochen- und Tageschart die Trendvorzugsrichtung ermittelt: Befindet sich der Schlusskurs der aktuellen Kerze auf der Seite mit dem größeren Winkelversatz zur Periodenlinie, wird dies als Richtung dieser Periodenlinie gewertet. Anschließend wird auf dem 4-Stunden-Chart ein A-B-C-D-Kanal gebildet; anhand der Kanalrichtung und der Wendepunkte werden Kauf- und Verkaufssignale generiert. Schließlich muss die auf der aktuellen Periodenlinie ermittelte Vorzugsrichtung mit der Richtung des 4-Stunden-Signals übereinstimmen. Dadurch werden viele Fehlsignale ausgefiltert und die Zuverlässigkeit der Handelssignale erhöht.

Strategievorteile

Die Strategie bietet folgende Hauptvorteile:

- Doppelte Signalfilterung auf Basis mehrerer Zeitrahmen filtert Rauschen effektiv aus und liefert hochzuverlässige Handelsmöglichkeiten.

- Die Bildung von Kanälen zur Bestimmung von Kauf- und Verkaufspunkten sorgt für klare Handelssignale.

- Fibonacci-Retracement-Levels für Take-Profit und Stop-Loss ermöglichen schnelle Gewinnmitnahmen und Verlustbegrenzungen.

- Die Strategie hat wenige Parameter und ist leicht verständlich und beherrschbar.

- Sie ist gut erweiterbar und leicht zu optimieren und verbessern.

Strategierisiken

Die Strategie birgt folgende Hauptrisiken:

- Die Überwachung zu vieler Zeitrahmen erhöht die Komplexität und die Fehleranfälligkeit.

- Unvorhergesehene Ereignisse wie starke Kursbewegungen durch wichtige Nachrichten werden nicht berücksichtigt.

- Die Festlegung von Take-Profit und Stop-Loss anhand von Retracement-Levels kann zu unzureichenden Gewinnen führen.

- Eine falsche Parametrisierung kann zu Überhandel oder verpassten Trades führen.

Gegenmaßnahmen:

- Verstärkte Überwachung von Ausnahmesituationen und wichtigen Nachrichtenereignissen.

- Optimierung der Take-Profit/Stop-Loss-Logik, um sicherzustellen, dass Gewinne ein bestimmtes Niveau erreichen.

- Gründliches Testen und Optimieren der Parameter, um die Wahrscheinlichkeit von Überhandel und verpassten Trades zu verringern.

Optimierungsmöglichkeiten

Die Hauptoptimierungsrichtungen der Strategie sind:

- Integration von Machine-Learning-Modellen zur Bestimmung der Trendvorzugsrichtung, um durch mehr Daten die Treffsicherheit zu erhöhen.

- Testen anderer Indikatoren zur Kanalbildung und Bestimmung von Kauf-/Verkaufspunkten.

- Ausprobieren fortschrittlicherer Take-Profit/Stop-Loss-Methoden wie Trailing-Stop, Jump-Stop usw.

- Ableiten optimaler Parameter aus Backtesting-Ergebnissen, um die Parametereinstellungen stärker an den Prinzipien des quantitativen Investierens auszurichten.

- Hinzufügen eines Überwachungs- und Reaktionsmechanismus für wichtige unerwartete Ereignisse.

Zusammenfassung

Insgesamt basiert die Strategie auf dem Kerngedanken einer hochfrequenten quantitativen Handelsstrategie, die durch doppelte Filterung Rauschen reduziert. Sie nutzt die Bewertung auf mehreren Zeitrahmen und die Kanalbildung zur Bestimmung von Kauf- und Verkaufspunkten, um eine doppelte Zuverlässigkeitsfilterung der Handelssignale zu erreichen. Gleichzeitig hat die Strategie wenige Parameter, ist leicht zu beherrschen, gut erweiterbar und einfach zu optimieren. In der nächsten Phase wird sie in den Bereichen Bewertungsgenauigkeit, Take-Profit/Stop-Loss-Methoden und Parameteroptimierung verbessert, um eine bessere Leistung zu erzielen.

- 1