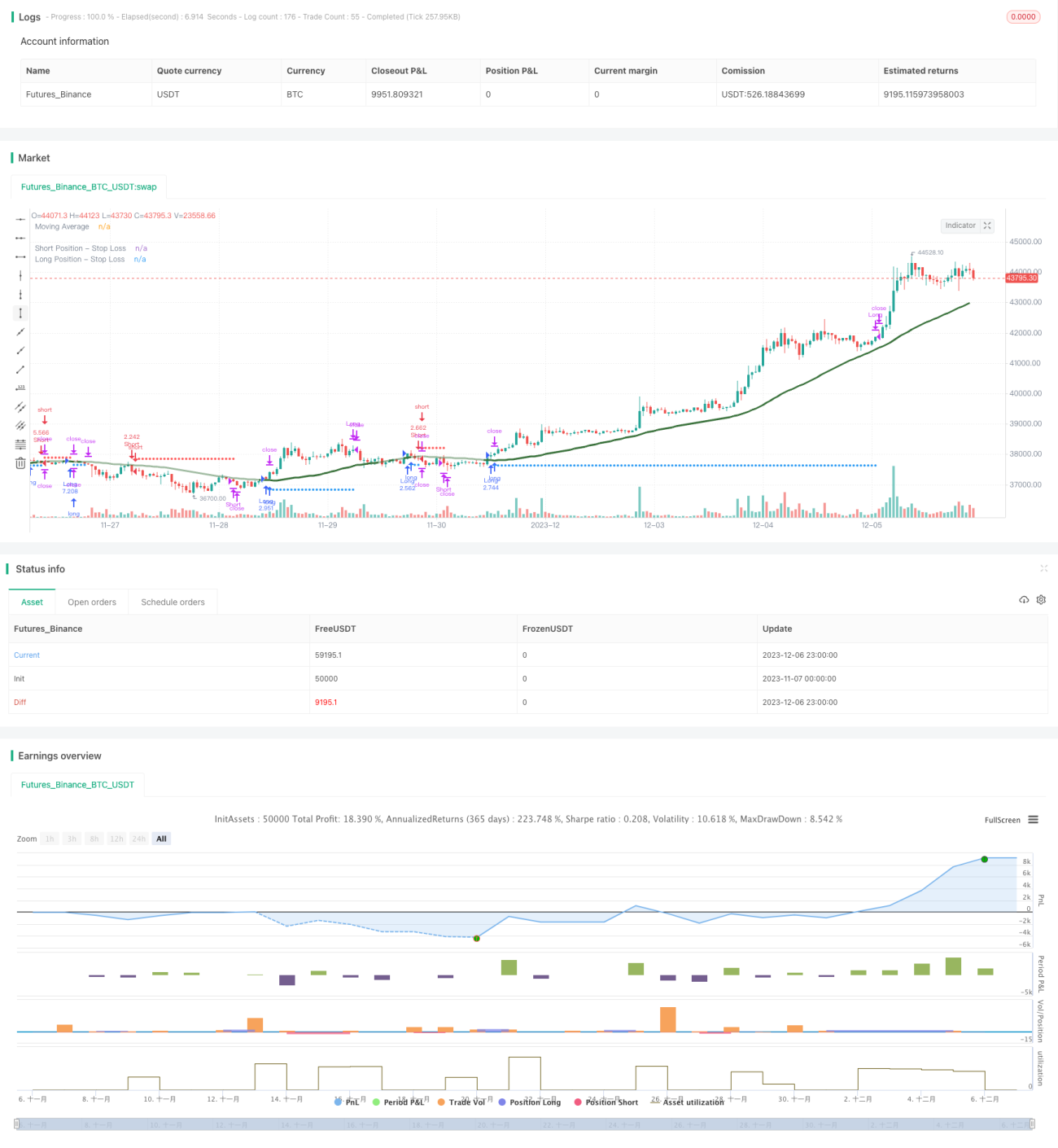

kNN-basierte Trendfolgestrategie

Übersicht

Diese Strategie nutzt den k-Nearest-Neighbor (kNN) Algorithmus des maschinellen Lernens zur Vorhersage von Markttrends und generiert auf Basis der Vorhersagen Long- und Short-Signale. Die Strategie berücksichtigt historische Daten, technische Indikatoren und weitere Faktoren, trainiert das kNN-Modell dynamisch, um Marktcharakteristiken zu extrahieren, und ermöglicht einen automatisierten Trendfolgehandel.

Funktionsprinzip

- Datensammlung: Sammlung historischer Zeitreihen wie Schlusskurse, Handelsvolumen sowie technischer Indikatoren wie RSI, CCI.

- Datenvorverarbeitung: Normalisierung der Indikatorwerte auf den Bereich 0–100.

- Training des kNN-Modells: Eingabe der beiden aktuellen Merkmale des kNN-Modells, Berechnung der euklidischen Distanz zwischen diesen Merkmalsvektoren und historischen Merkmalsvektoren, Auswahl der k nächsten historischen Stichproben und statistische Verteilung der Labels (Long oder Short) dieser k Stichproben.

- Prognose erhalten: Vorhersage der aktuellen Marktrichtung anhand der Labels der k nächsten Nachbarn. Bei Prognose „Long“ wird ein Long-Signal generiert, bei „Short“ ein Short-Signal.

- Handel mit Filtern: Kombination mit Stop-Loss, Positionsgrößenkontrolle, gleitenden Durchschnitten und anderen Filtern.

Vorteile

- Automatische Erkennung technischer Formationen durch maschinelles Lernen – kein manueller Eingriff erforderlich.

- Flexible Auswahl verschiedener technischer Indikatoren als Modellmerkmale – Echtzeitoptimierung der Strategie.

- Integration strenger Risikomanagementmechanismen wie Stop-Loss und Positionsmanagement.

- Visuelle Darstellung der Stop-Loss-Linie – klar und intuitiv.

Risiken und Lösungen

- Falschmeldungen durch maschinelles Lernen möglich. Optimierung des Modells durch geeignete Wahl von k, Merkmalsvektoren, Zeitfenster usw.

- Potenzielles Risiko bei einseitigem Handel. Durch Hinzufügen einer bilateralen Handelserlaubnis im Code können Fehler vermieden werden.

- Ungeeignete Parametereinstellungen können zu übermäßigem Handel führen. Anpassung von Positionsgröße, Handelsfrequenz usw.

Optimierungsmöglichkeiten

- Testen verschiedener Arten technischer Indikatoren als Eingabemerkmale für kNN.

- Ausprobieren anderer Distanzmaße wie Manhattan-Distanz.

- Anpassen der Positionsgröße anhand von Stichprobendistanz oder Klassifikationsqualität.

- Aufteilung in Trainings- und Testdatensätze für rollierende Optimierung.

Zusammenfassung

Diese Strategie nutzt den klassischen kNN-Algorithmus zur Vorhersage von Markttrends und führt einen Trendfolgehandel basierend auf den Vorhersagesignalen durch. Die Strategie ist parametrisierbar und risikokontrollierbar und bietet dem Nutzer eine effektive automatisierte Handelslösung. Durch Anpassen der Kombination technischer Indikatoren und Optimieren der Modell-Hyperparameter kann die Strategieleistung kontinuierlich verbessert werden.

- 1