Zwei-Bänder-Durchbruchsstrategie

Überblick

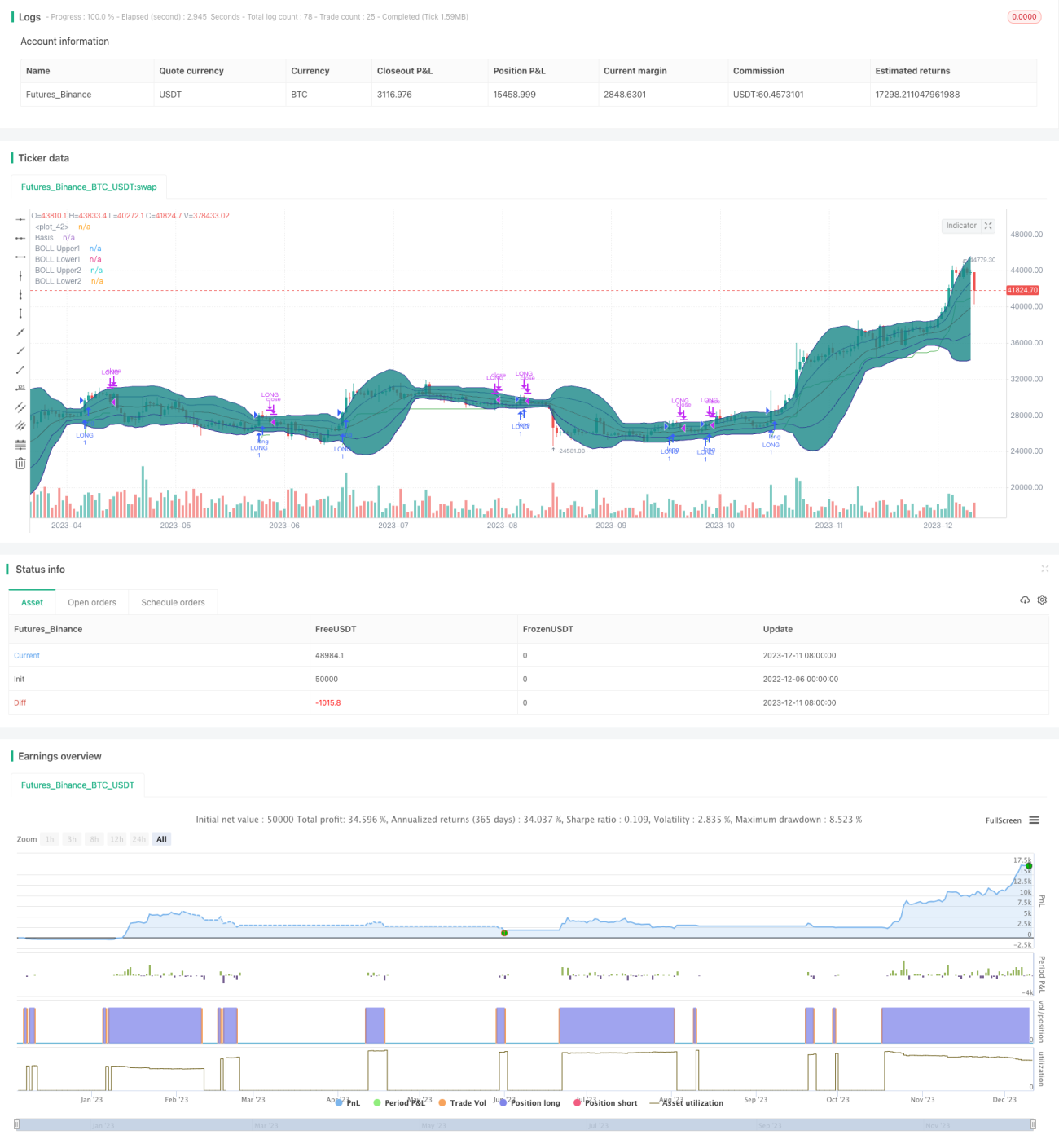

Diese Strategie verwendet den Double-Bollinger-Bänder-Indikator, um Konsolidierungsbereiche zu identifizieren, und kombiniert ihn mit einer Ausbruchsstrategie, um eine Tiefkaufen-Hochverkaufen-Strategie umzusetzen. Wenn der Preis die neutrale Zone durchbricht, deutet dies auf den Beginn eines neuen Trends hin, und es wird eine Long-Position eröffnet. Wenn der Preis die neutrale Zone wieder nach unten durchbricht, endet der Trend und die Position wird geschlossen.

Funktionsweise der Strategie

Diese Strategie verwendet zwei Bollinger-Bänder. Die obere und untere Grenze des inneren Bandes sind der 20-Tage-einfache gleitende Durchschnitt ± 1 Standardabweichung; die des äußeren Bandes sind der 20-Tage-einfache gleitende Durchschnitt ± 2 Standardabweichungen. Wenn der Preis zwischen dem inneren und äußeren Band liegt, wird dies als neutrale Zone definiert.

Wenn der Preis zwei aufeinanderfolgende Kerzen in der neutralen Zone liegt, wird dies als Konsolidierung betrachtet. Nach zwei konsolidierenden Kerzen erzeugt der Schlusskurs der dritten Kerze, der die obere Grenze des inneren Bandes überschreitet, ein Long-Signal.

Nach Eröffnung einer Long-Position wird der Stop-Loss auf Tiefstpreis - 2×ATR gesetzt, um Gewinne zu sichern und Risiken zu kontrollieren. Wenn der Preis die obere Grenze des inneren Bandes nach unten durchbricht, wird die Position geschlossen.

Vorteilsanalyse

Diese Strategie kombiniert Indikator und Trend, um Konsolidierungsbereiche zu identifizieren und zu beurteilen, ob der Preis einen neuen Trend startet, und ermöglicht so Tiefkaufen und Hochverkaufen mit großem Gewinnpotenzial. Die Stop-Loss-Strategie sichert Gewinne und kontrolliert Risiken, was die Stabilität der Strategie erhöht.

Risikoanalyse

Diese Strategie ist auf Long-Signale angewiesen, die durch den Ausbruch des Preises über die obere Grenze des Bollinger-Bandes entstehen. Bei einem Fehlausbruch können Fehlpositionen und Verluste entstehen. Zudem kann ein zu enger Stop-Loss zu einem sofortigen Ausstieg führen.

Durch Optimierung der Parameter der Bollinger-Bänder und Hinzufügen von Filtern kann die Wahrscheinlichkeit von Fehlausbrüchen verringert werden. Außerdem kann der Stop-Loss großzügiger gesetzt werden, um ausreichend Spielraum zu gewährleisten.

Optimierungsmöglichkeiten

- Optimierung der Parameter der Bollinger-Bänder, Anpassung der Bandbreite, um die Wahrscheinlichkeit von Fehlausbrüchen zu verringern

- Hinzufügen weiterer Indikatorfilter, z.B. Volumen, um Fehlausbrüche bei geringem Volumen zu vermeiden

- Anpassung der Stop-Loss-Strategie, um zu verhindern, dass man in der Falle sitzt oder sofort ausgestoppt wird

- Hinzufügen einer Strategie zur schrittweisen Positionseröffnung, um das Einzelrisiko zu reduzieren

Zusammenfassung

Diese Strategie integriert den Double-Bollinger-Bänder-Indikator und eine Trendstrategie, um Tiefkaufen und Hochverkaufen mit großem Gewinnpotenzial zu ermöglichen. Gleichzeitig sorgt die Stop-Loss-Strategie für eine relative Stabilität. Durch weitere Optimierung kann die Effektivität der Strategie verbessert werden, was eine praktische Erprobung im Live-Handel rechtfertigt.

- 1