Doppelte Bestätigungs-Ausbruchsstrategie

Übersicht

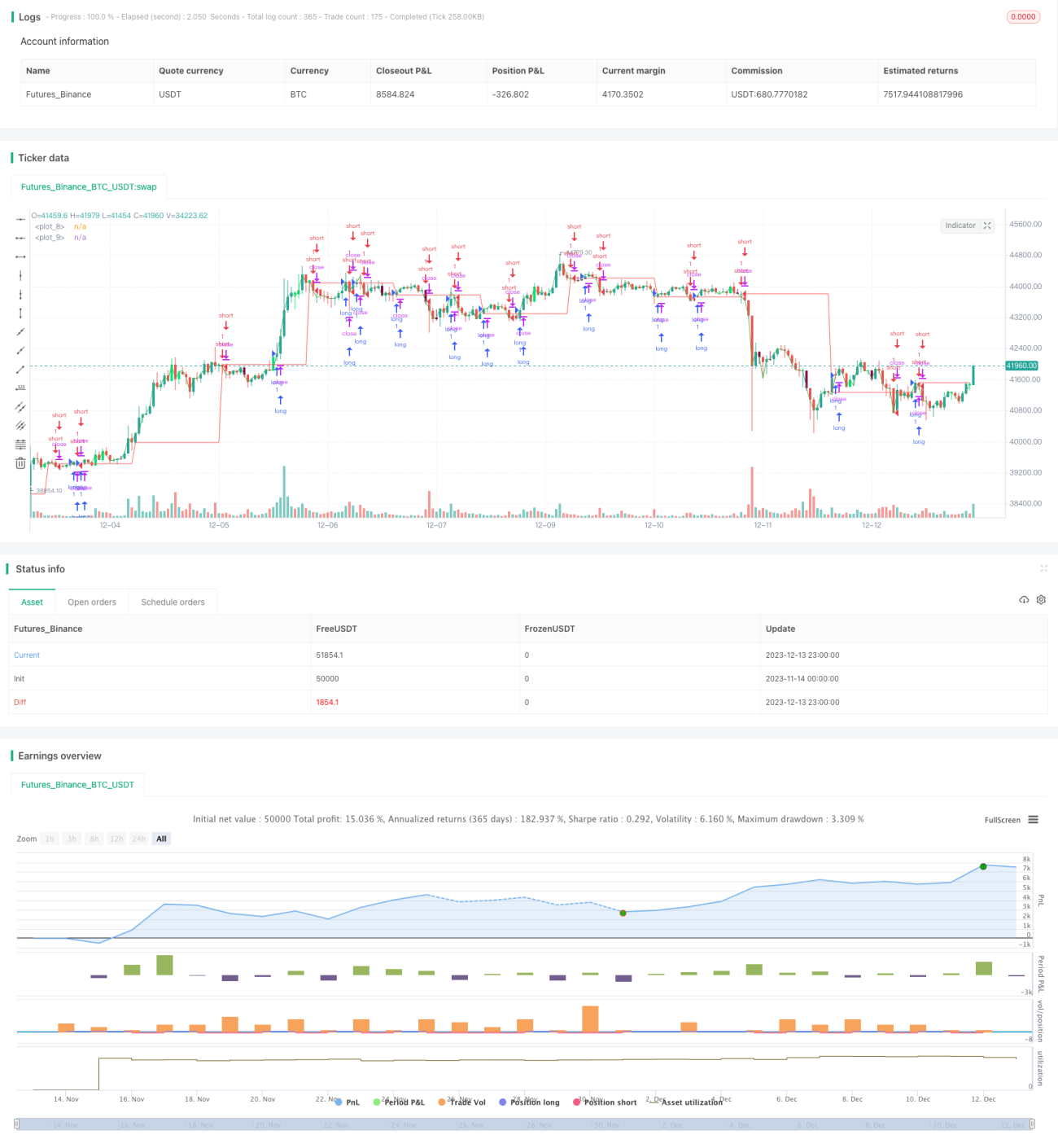

Diese Strategie kombiniert Ausbruchssignale im 4-Stunden- und Tageszeitrahmen und validiert vor der Auslösung eines Handelssignals die Kerzenformation, um so eine zuverlässigere Ausbruchsstrategie zu realisieren.

Strategieprinzip

Die Doppelbestätigungs-Ausbruchsstrategie identifiziert durch die Kombination von Ausbruchssignalen kurzer und langer Zeiträume effektivere Ausbruchspunkte unter Berücksichtigung der Konsistenz der Trends beider Zeitrahmen. Konkret berechnet die Strategie gleitende Durchschnitte im 4-Stunden- und Tageszeitrahmen. Wenn der kurzfristige gleitende Durchschnitt den langfristigen gleitenden Durchschnitt überschreitet, wird ein Kaufsignal generiert, der umgekehrte Ausbruch ein Verkaufssignal. Zusätzlich wird die aktuelle Kerzenformation vor dem Signalauslöser validiert, um Positionen nicht während einer laufenden Kerze zu eröffnen.

Durch diesen doppelten Bestätigungs- und Kerzenfiltermechanismus können Risiken wie Stop-Loss bei Long-Positionen oder Fangen bei Short-Positionen effektiv vermieden und die Signalqualität verbessert werden.

Vorteilsanalyse

-

Doppelter Zeitrahmenausbruch verbessert die Signalqualität. Die Kombination aus 4-Stunden- und Tages-Chart vereint die Vorteile der Verfolgung kurzfristiger Trends und der Berücksichtigung langfristiger Trends.

-

Kerzenformationsvalidierung vermeidet Fehlsignale. Die Validierung vor dem Signalauslöser filtert falsche oder ungewöhnliche Ausbrüche und vermeidet Verluste.

-

Automatische Optimierung – flexibel und bequem. Die Ausbruchs- und Zeitparameter der Strategie sind anpassbar, sodass Nutzer für verschiedene Handelsinstrumente und Märkte die optimale Parameterkombination wählen können.

Risikoanalyse

-

Schwache Nachverfolgung bei starken Kursbewegungen. Bei gleichzeitigen heftigen Bewegungen im kurzen und langen Zeitrahmen kann die Strategie den optimalen Einstiegspunkt verpassen.

-

Kerzenvalidierung kann Chancen verpassen. In extremen Märkten sind Kerzen oft verzerrt, der Validierungsmechanismus macht die Strategie konservativ und führt zu verpassten Gelegenheiten.

-

Unangemessene Parameter erzeugen Fehlsignale. Nutzer müssen je nach Instrument die richtigen Doppelausbruch- und Kerzenparameter wählen; falsche Parameter beeinträchtigen die Strategie erheblich.

Zur Minderung dieser Risiken können Parameteranpassungen, die Einrichtung von Stop-Loss/Take-Profit usw. vorgenommen werden.

Optimierungsmöglichkeiten

-

Sekundäre Validierung mit Volatilitätsindikatoren. Ausbruchssignale, die beispielsweise während einer Bollinger-Bänder-Einschnürung auftreten, sind qualitativ hochwertiger.

-

Hinzufügen von Stop-Loss/Take-Profit-Modulen. Angemessene Stop-Loss/Take-Profit-Einstellungen sichern Gewinne und vermeiden Risiken aktiv.

-

Optimierung der Doppelausbruchsparameter. Parameter können basierend auf der intraday- und Tagesvolatilität des Instruments angepasst werden.

-

Optimierung der Kerzenvalidierungsparameter. Unterschiedliche Zeitrahmen und Parameterkombinationen für die Kerzenvalidierung liefern stabilere Ergebnisse.

Zusammenfassung

Die Doppelbestätigungs-Ausbruchsstrategie erreicht durch die Kombination von Doppelzeitrahmen und Kerzenformationsvalidierung ein effektives Gleichgewicht zwischen Kapitaleffizienz und Signalqualität und ist eine empfehlenswerte kurzfristige Ausbruchsstrategie. Nutzer können die relevanten Parameter nach Bedarf anpassen, um bessere Ergebnisse zu erzielen.

- 1