Mehrfach-Zeitrahmen modifizierte und verbesserte Stochastik-Indikator und SMA-Kombinations-Trendfolgestrategie

Übersicht

Diese Strategie kombiniert die klassischen Stochastic-Indikatoren mit SMA-Indikatoren, um eine starke Trendfolgefähigkeit zu erreichen. Der Kern der Strategie besteht darin, mit dem Stochastic-Indikator Trendsignalrichtungen zu identifizieren, diese mit dem SMA-Indikator zu filtern, um die Signalqualität zu verbessern, und unterschiedliche Risikomodi zur Einstellung der Indikatorparameter zu nutzen, um eine dynamische Anpassung von Risiko und Rendite zu ermöglichen. Darüber hinaus optimiert die Strategie die Einstiegszeitpunkte durch die Nutzung mehrerer Zeitrahmen.

Strategieprinzip

- Die Strategie verwendet eine modifizierte und verbesserte Version des Stochastic-Indikators. Die Indikatorparameter umfassen %K-Periode, %K-Glättungsperiode und %D-Glättungsperiode, durch deren Einstellung die Empfindlichkeit des Indikators gesteuert wird.

- Die SMA-Indikatorparameter umfassen den Hochpunkt-SMA und den Tiefpunkt-SMA, die zur Signalfilterung und Verbesserung der Signalqualität dienen, um Fehldurchbrüche zu vermeiden.

- Abhängig von der Risikobereitschaft bietet die Strategie eine Auswahl zwischen niedrigem, mittlerem und hohem Risikomodell. Der Risikomodell beeinflusst die Crossover-Parameter des Stochastic-Indikators und ermöglicht so eine dynamische Anpassung von Risiko und Rendite.

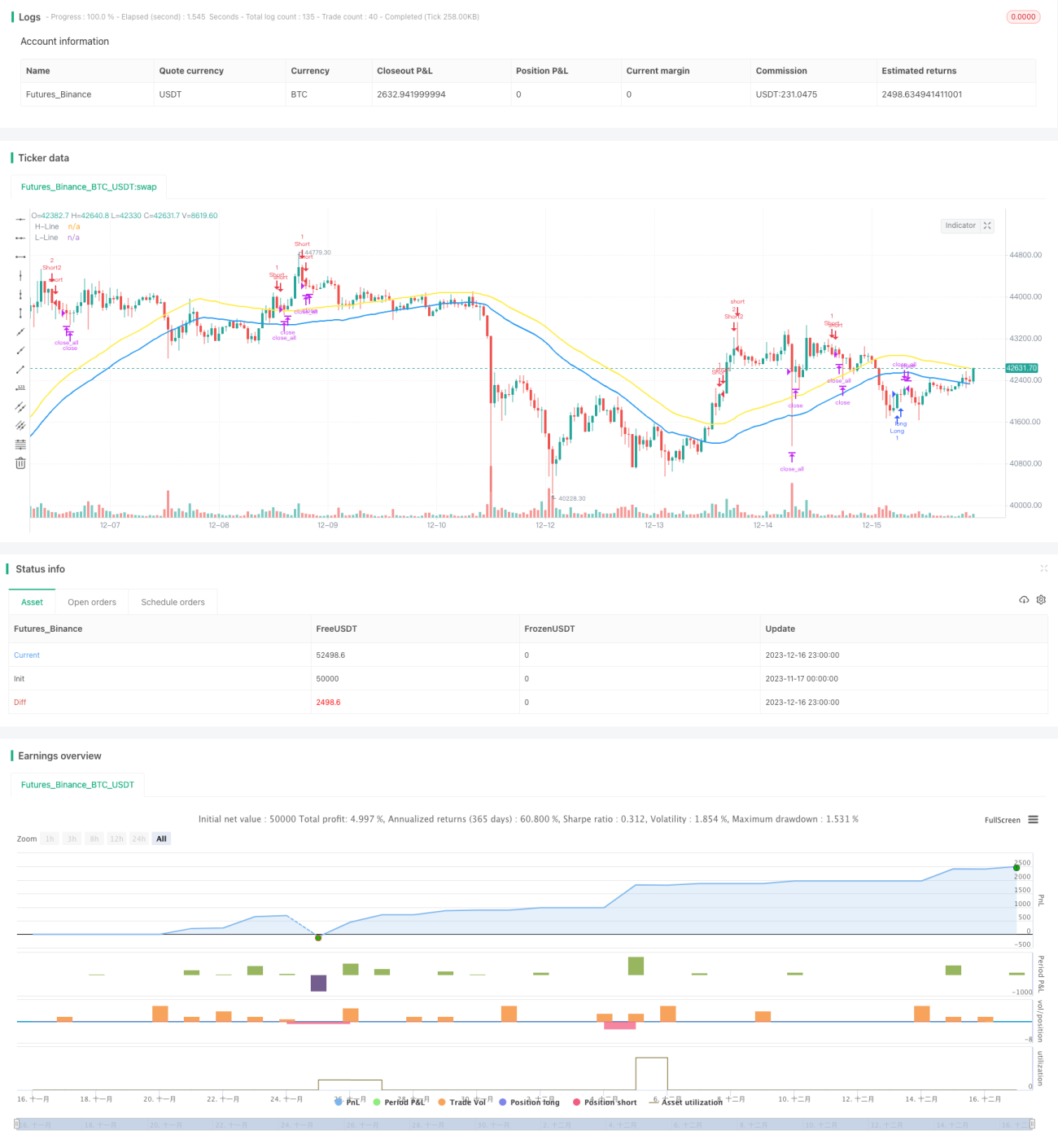

- Die Strategie identifiziert ein Long-Signal, wenn der Stochastic-Indikator den Schwellenwert nach oben durchbricht und der Schlusskurs unter dem Tiefpunkt-SMA liegt; ein Short-Signal wird erkannt, wenn der Stochastic-Indikator den Schwellenwert nach unten durchbricht und der Schlusskurs über dem Hochpunkt-SMA liegt.

- Durch die Einführung eines Moduls zur Bewertung mehrerer Zeitrahmen werden Signale in verschiedenen Zeitintervallen verifiziert, um günstigere Einstiegszeitpunkte zu wählen und das Handelsrisiko zu kontrollieren.

Strategievorteile

- Verwendung einer modifizierten, verbesserten Version des Stochastic-Indikators, die die Empfindlichkeit des Indikators erhöht und eine schnelle Erfassung von Marktveränderungen ermöglicht.

- Ergänzung eines zweispurigen SMA-Filtermechanismus, der effektiv Fehlsignale herausfiltert und die Signalqualität verbessert.

- Bereitstellung mehrerer Risikomodi zur Auswahl, sodass Benutzer die Parameter je nach eigener Risikobereitschaft flexibel anpassen können.

- Integration eines Moduls zur Bewertung mehrerer Zeitrahmen, das die Auswahl des Einstiegszeitpunkts optimiert und das Handelsrisiko senkt.

- Angemessene Parametereinstellungen, natürlicher Einsatz der Indikatoren, insgesamt wissenschaftlicher und solider Rahmen mit guter Stabilität und Anpassungsfähigkeit.

Strategierisiken

- Die Strategie selbst verfügt über keinen Stop-Loss-Mechanismus; ein manuelles Setzen von Stop-Loss-Schwellen ist erforderlich, um Verlustrisiken zu kontrollieren.

- Die Strategie erzeugt häufige Signale, was zu übermäßigem Handel und höheren Transaktionskosten führen kann.

- Die Strategie reagiert empfindlich auf die Parameter- und Risikomodell-Einstellungen; es sind Tests und Optimierungen erforderlich, um die idealen Parameter zu finden.

- Der Drawdown der Strategie kann erheblich sein; eine vollständige Positionierung ist nicht geeignet, die Handelskapitalgröße muss kontrolliert werden.

Entsprechende Maßnahmen:

- Angemessene Festlegung des Stop-Loss-Prozentsatzes basierend auf der Marktvolatilität, um Verluste maximal zu begrenzen.

- Anpassung der Stochastic-Indikatorparameter, um die Signalfrequenz zu verringern, oder Festlegung eines Mindest-Take-Profit, um unnötige Trades zu reduzieren.

- Empfehlung, den Standard-Niedrigrisiko-Modus zu wählen und andere Parameter anhand von Backtest-Daten anzupassen.

- Kontrolle der Positionsgröße, schrittweiser Aufbau von Positionen, um das Risiko pro Trade zu senken.

Optimierungsrichtungen der Strategie

- Vollständige Tests der Parameter des Stochastic- und SMA-Indikators, um die optimale Parameterkombination zu finden.

- Erhöhung der Anzahl der Zeitrahmen, um die Beurteilungsgrundlage zu erweitern und die Einstiegszeitpunktauswahl zu optimieren.

- Einführung einer Stop-Loss-Indikatorkombination wie ATR-Stop-Loss, um einen dynamischen Stop-Loss nachzuführen und das Risiko zu senken.

- Aufbau eines Signal-Filter- und Bestätigungsmechanismus, z. B. durch Hinzufügen eines Volumenindikators, um Fehlsignale zu vermeiden.

- Integration eines Positionsmanagement-Moduls, das die Positionen je nach Marktlage aktiv anpasst, um das Risiko pro Trade zu reduzieren.

Zusammenfassung

Diese Strategie kombiniert die Vorteile des Stochastic-Indikators und des SMA-Indikators, um eine starke Trendfolgewirkung zu erzielen. Der Strategierahmen ist sinnvoll, der Einsatz der Indikatoren natürlich. Durch die Kontrolle der Parameter und Risikomodi wird das Wesen der Indikatoren wiederhergestellt und die Stabilität der Strategie optimiert. Das Modul zur Bewertung mehrerer Zeitrahmen verbessert zudem die Anpassungsfähigkeit der Strategie, die je nach Produkt und Zeiteinheit angepasst werden kann. Insgesamt bietet die Strategie eine gute Allgemeingültigkeit und zugleich ein großes Optimierungspotenzial, das eine weiterführende Untersuchung wert ist.

- 1