Momentum-Stochastik-Geglätteter-Gleitender-Durchschnitt-Strategie

Übersicht

Diese Strategie kombiniert den exponentiell gleitenden Durchschnitt (EMA) mit dem Stochastic-Oszillator, folgt dem Trend und setzt auf Fortsetzungsbewegungen – und bietet zudem einige coole Funktionen. Ich habe diese Strategie speziell für den Handel mit Altcoins entwickelt, sie funktioniert aber genauso gut für Bitcoin selbst sowie für einige Devisenpaare.

Funktionsweise der Strategie

Die Strategie hat vier notwendige Bedingungen für ein Handelssignal. Im Folgenden sind die Bedingungen für eine Long-Position aufgeführt (die Signale für eine Schließung sind genau entgegengesetzt):

- Der schnelle EMA liegt über dem langsamen EMA

- Die Stochastic-K-Linie befindet sich im überkauften Bereich

- Die Stochastic-K-Linie kreuzt die Stochastic-D-Linie von unten nach oben

- Der Schlusskurs liegt zwischen dem langsamen EMA und dem schnellen EMA

Sobald alle Bedingungen erfüllt sind, wird zu Beginn des nächsten Candlesticks eine Position eröffnet.

Vorteilsanalyse

Die Strategie kombiniert die Stärken von EMA und Stochastic-Oszillator, um den Beginn und die Fortsetzung von Trends effektiv zu erkennen. Sie eignet sich für mittel- bis langfristige Operationen. Gleichzeitig bietet die Strategie verschiedene anpassbare Parameter, die der Nutzer je nach seinem Handelsstil und den Marktmerkmalen einstellen kann.

Im Einzelnen sind die Vorteile der Strategie:

- Der EMA-Crossover bestimmt die Trendrichtung und erhöht die Stabilität und Zuverlässigkeit der Signale.

- Der Stochastic-Oszillator zeigt überkaufte oder überverkaufte Bereiche an und sucht nach Umkehrchancen.

- Durch die Kombination beider Indikatoren werden sowohl Trendfolge als auch konträre Handelssignale berücksichtigt.

- Der ATR berechnet automatisch den Stop-Loss-Abstand, der sich an die Marktvolatilität anpasst.

- Das Verhältnis von Risiko zu Gewinn kann individuell angepasst werden, um den Anforderungen verschiedener Nutzer gerecht zu werden.

- Es stehen zahlreiche anpassbare Parameter zur Verfügung, sodass der Nutzer die Strategie je nach Marktlage anpassen kann.

Risikoanalyse

Die Hauptrisiken dieser Strategie liegen in:

- EMA-Crossover-Signale können Fehlausbrüche erzeugen, was zu irreführenden Signalen führt.

- Der Stochastic-Oszillator selbst ist nachlaufend, sodass der optimale Zeitpunkt für eine Preisumkehr möglicherweise verpasst wird.

- Eine einzelne Strategie kann sich nicht vollständig an die sich ständig ändernden Marktbedingungen anpassen.

Um die genannten Risiken zu verringern, können folgende Maßnahmen ergriffen werden:

- Passen Sie die EMA-Periodenparameter angemessen an, um übermäßig viele Fehlsignale zu vermeiden.

- Kombinieren Sie weitere Indikatoren zur Trend- und Unterstützungsbestimmung, um die Zuverlässigkeit der Handelssignale zu gewährleisten.

- Entwickeln Sie eine klare Geldmanagementstrategie, um das Risiko pro Trade zu begrenzen.

- Verwenden Sie eine Multi-Strategie, bei der sich verschiedene Strategien gegenseitig validieren, um die Stabilität zu erhöhen.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen weiter optimiert werden:

- Ein auf Volatilität basierendes Modul zur Positionsanpassung einfügen. Bei steigender Marktvolatilität die Positionen verkleinern, bei nachlassender Volatilität die Positionen vergrößern.

- Einbeziehung der übergeordneten Trendrichtung, um gegenläufige Geschäfte zu vermeiden. Beispielsweise den Trend anhand von Tages- oder Wochenkerzen bestimmen.

- Einbindung von maschinellen Lernmodellen zur Beurteilung von Kauf- und Verkaufssignalen. Anhand historischer Daten könnte ein Klassifikationsmodell trainiert werden, das zusätzliche Handelssignale generiert.

- Optimierung des Geldmanagementmoduls, um den Stop-Loss und die Positionsgröße noch intelligenter zu gestalten.

Zusammenfassung

Diese Strategie vereint die Vorteile von Trendfolge und gegenläufigem Handel. Sie berücksichtigt sowohl das übergeordnete Marktumfeld als auch das aktuelle Preisverhalten und ist eine effektive Strategie, die sich für eine langfristige Verfolgung im Live-Handel eignet. Durch die kontinuierliche Optimierung der Parametereinstellungen, die Integration von Trendbestimmungsmodulen und weitere Maßnahmen besteht noch großes Potenzial zur Leistungssteigerung, sodass sich zusätzliche Forschungs- und Entwicklungsarbeit lohnt.

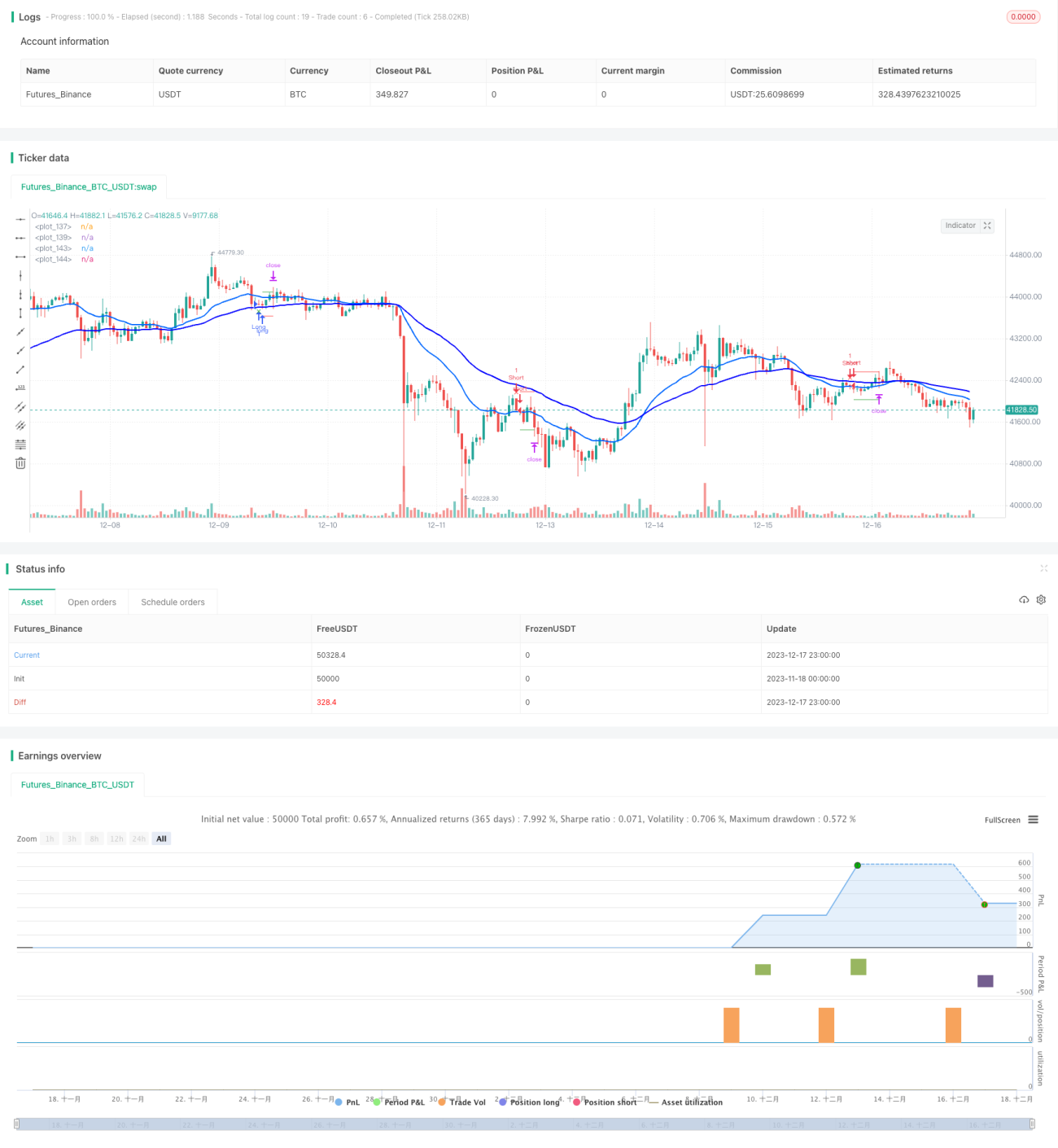

/*backtest

start: 2023-11-18 00:00:00

end: 2023-12-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LucasVivien

// Since this Strategy may have its stop loss hit within the opening candle, consider turning on 'Recalculate : After Order is filled' in the strategy settings, in the "Properties" tabs- 1