Kifiers versteckte MFI/STOCH-Indikator-Trading- und Trend-Trading-Strategie

Übersicht

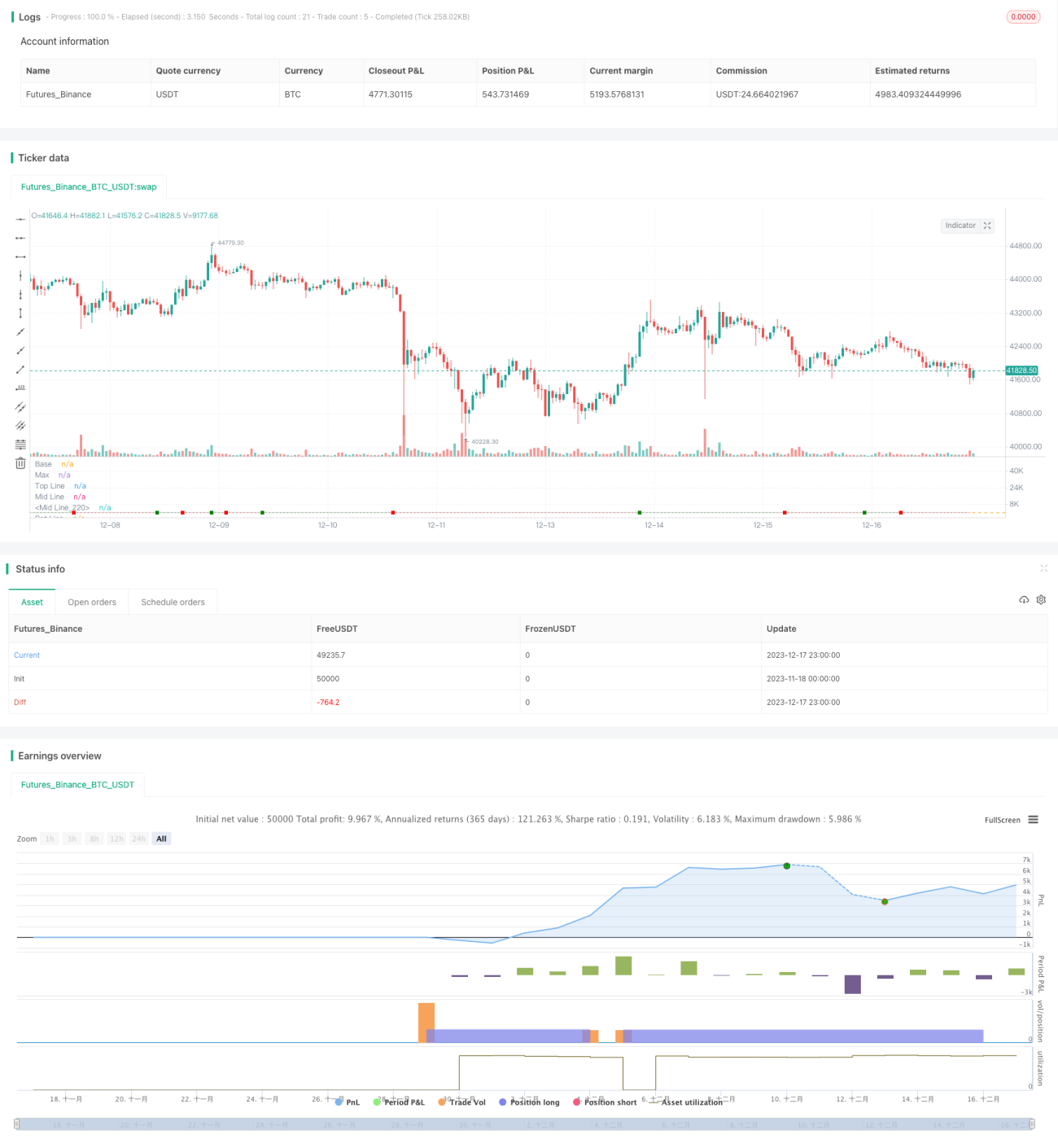

Dies ist eine universelle Handelsstrategie für den Kryptowährungsmarkt, die darauf abzielt, in einem bullischen Umfeld günstige Einstiegszeitpunkte für mittel- bis langfristige Positionen zu finden. Die Strategie kombiniert mehrere technische Indikatoren wie MFI, STOCH und VWMA, um durch die Erkennung versteckter Divergenzen potenzielle Trendumkehrungen zu identifizieren.

Strategieprinzip

Die Strategie umfasst zwei Einstiegslogiken:

-

MFI-Versteckte-Divergenz + STOCH-Filter: Wenn der MFI eine versteckte Divergenz bildet – d.h. der Preis erreicht ein neues Hoch, der MFI jedoch nicht – wird dies als potenzielles Signal für eine Trendumkehr gewertet. Um Fehlsignale zu vermeiden, wird als zusätzlicher Filter STOCH > 50 % hinzugefügt.

-

STOCH/MFI-Trendsystem: Wenn STOCH > 50 % und der MFI die 50er-Linie von unten nach oben kreuzt, deutet dies auf einen sich bildenden Markttrend hin. Ein Einstieg zu diesem Zeitpunkt bietet ein gutes Risiko-Ertrags-Verhältnis.

Zur Sicherstellung der Trendgenauigkeit haben wir ein auf VWMA und SMA basierendes Trendsystem entwickelt. Nur wenn der VWMA den SMA von unten kreuzt (d.h. ein Aufwärtstrend bestätigt ist), werden die beiden obigen Systeme Handelssignale ausgeben. Zusätzlich verwenden wir den OBV-Indikator, um zu beurteilen, ob der Gesamtmarkt aktiv oder seitwärts tendiert; dies dient ebenfalls zur Filterung von Fehlsignalen.

Der ATR-Indikator wird genutzt, um festzustellen, ob der Markt sich in einer Range befindet. Wir bevorzugen es, in solchen Phasen nach MFI-Versteckten-Divergenzen für Einstiege zu suchen. Der Stop-Loss wird anhand eines nahegelegenen Unterstützungsniveaus festgelegt. Der Take-Profit wird als prozentualer Gewinn ab Einstiegskurs berechnet.

Vorteilsanalyse

Diese Strategie kombiniert mehrere Indikatoren zur Analyse der Marktstruktur und vermeidet so erfolgreich die meisten Marktstörungen. Das System der versteckten Divergenzen bietet in Range- und Korrekturphasen Einstiege mit hoher Wahrscheinlichkeit und kontrolliertem Risiko. Das STOCH/MFI-Trendsystem hingegen ermöglicht zusätzliche Gewinne in klaren Trends. Stop-Loss und Take-Profit sind sinnvoll gesetzt und vermeiden häufige Fehler wie das Jagen von Kursen oder Panikverkäufe. Die gesamte Strategie eignet sich hervorragend für den volatilen Kryptomarkt und bietet risikobereinigt gute Renditen.

Risikoanalyse

Das größte Risiko dieser Strategie liegt darin, dass die Erkennung versteckter Divergenzen nicht immer zuverlässig ist; sie spiegelt lediglich eine Änderung der Marktstimmung wider, garantiert aber keine sofortige Trendumkehr. Zudem können falsche Parametereinstellungen für STOCH und andere Indikatoren dazu führen, dass Trends verpasst werden oder Fehlsignale entstehen. Schließlich kann ein zu aggressiver Stop-Loss/Take-Profit zu häufigen Ausstiegen und Wiedereinstiegen führen, was die Rendite schmälert.

Um diese Risiken zu mindern, filtern wir Signale zusätzlich durch Trend- und Marktzustandsprüfungen und setzen etwas großzügigere Stop-Loss/ Take-Profit-Niveaus. Dennoch können bei fehlendem rechtzeitigen Stop-Loss oder bei größeren makroökonomischen Ereignissen auch erhebliche Verluste nicht vollständig vermieden werden.

Optimierungsmöglichkeiten

Diese Strategie bietet noch Raum für Verbesserungen, insbesondere in folgenden Bereichen:

-

Optimierung der Parametereinstellungen von MFI und STOCH, um die Genauigkeit der Erkennung versteckter Divergenzen zu erhöhen.

-

Integration von maschinellem Lernen zur Beurteilung der Marktsituation und Backtesting zur Bestimmung optimaler Parameter.

-

Erprobung dynamischer Stop-Loss/Take-Profit, um bei gleichbleibender Rendite das Risiko weiter zu kontrollieren.

-

Testen der Unterschiede zwischen verschiedenen Kryptowährungen und Anpassung individueller Parameter.

-

Hinzufügen eines Aktienauswahlmoduls, damit sich die Strategie auf technisch besser strukturierte Einzelwerte konzentriert.

Durch diese Optimierungen können Stabilität und Rendite der Strategie voraussichtlich weiter gesteigert werden.

Zusammenfassung

Es handelt sich um eine sehr praxistaugliche Krypto-Handelsstrategie. Sie nutzt geschickt mehrere technische Indikatoren zur Analyse der Marktstruktur und erzielt bei kontrolliertem Risiko gute Gewinne. Das Hauptproblem ist die nicht immer zuverlässige Erkennung versteckter Divergenzen, das durch eine Reihe von Filtern abgemildert wird. Die Strategie hat noch Potenzial für weitere Stabilitäts- und Renditeverbesserungen und ist einen Test im Live-Handel sowie eine langfristige Beobachtung wert. Sie bietet quantitativen Händlern einen effektiven Ansatz, um am Kryptomarkt stabile Gewinne zu erzielen.

- 1