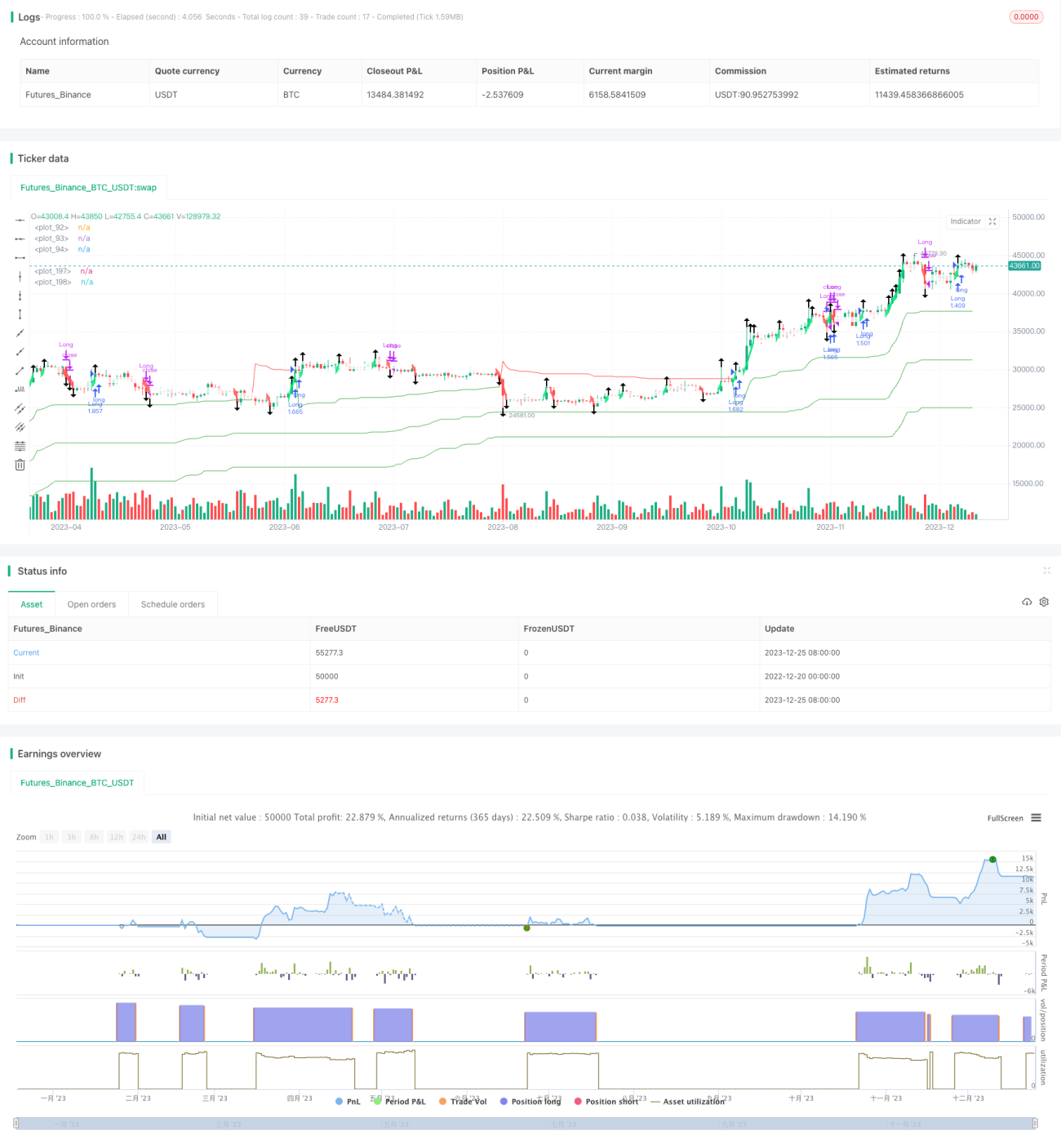

Trendfolge-Intraday-Strategie mit mehreren Stop-Loss-Ebenen

Überblick

Diese Strategie vereint mehrere dynamische ATR-Stopps mit verbesserten Renko-Bausteinen, um Intraday-Trendbewegungen zu erfassen. Sie kombiniert Trendindikatoren und Bausteinindikatoren für eine Multi-Timeframe-Analyse, die es ermöglicht, Trendrichtungen zuverlässig zu identifizieren und rechtzeitig Stopps zu setzen.

Strategieprinzip

Der Kern der Strategie liegt im mehrstufigen ATR-Stoppmechanismus. Es werden drei ATR-dynamische Stopps mit den Parametern 5-faches ATR, 10-faches ATR und 15-faches ATR eingerichtet. Wenn der Preis diese drei Stopplinien unterschreitet, deutet dies auf einen Trendwechsel hin und die Position wird geschlossen. Diese mehrstufige Stoppsetzung filtert effektiv falsche Signale durch kurzfristige Schwankungen heraus.

Ein weiterer Kernbestandteil sind die verbesserten Renko-Bausteine. Diese Bausteine unterteilen die Inkremente basierend auf dem ATR-Wert und kombinieren dies mit dem SMA-Indikator zur Bestimmung der Trendrichtung. Sie reagieren empfindlicher als normale Renko-Bausteine und können Trendwechsel früher bestätigen. Wenn sich die Farbe eines Bausteins ändert, signalisiert dies einen Trendwechsel und kann als Stoppsignal dienen.

Die Einstiegsbedingung ist: Long gehen, wenn der Preis über die drei ATR-Stopps nach oben bricht; Short gehen, wenn der Preis unter die drei ATR-Stopps nach unten bricht. Die Ausstiegsbedingung ist: Schließen der Position, wenn der Preis einen der ATR-Stopps auslöst oder sich die Farbe eines Renko-Bausteins ändert.

Strategievorteile

- Mehrstufige ATR-Stopps zur effektiven Risikokontrolle

- Verbesserte Renko-Bausteine, empfindlicher und frühzeitiger Stopp möglich

- Kombination von Trendindikatoren und Bausteinindikatoren zur zuverlässigen Erfassung von Trends

- Multi-Timeframe-Analyse für zuverlässigere Trendrichtungsbestimmung

- Parameter anpassbar, um sich an verschiedene Marktbedingungen anzupassen

Strategierisiken und Optimierung

Das Hauptrisiko dieser Strategie besteht darin, dass der Stopp durchbrochen wird, was zu größeren Verlusten führt. Optimierungsmöglichkeiten:

- Anpassung der ATR-Stopp-Multiplikatoren: In starken Trendmärkten können sie etwas gelockert werden; in schwachen Trendmärkten sollten sie enger gesetzt werden

- Anpassung des ATR-Zeitraums der Renko-Bausteine, um ein Gleichgewicht zwischen Empfindlichkeit und Stabilität zu erreichen

- Hinzufügen weiterer Stoppindikatoren wie Donchian-Channel, um die Zuverlässigkeit der Stopps zu erhöhen

- Hinzufügen von Filtern, um häufigen Handel in Seitwärtsmärkten zu vermeiden

Zusammenfassung

Insgesamt eignet sich diese Strategie für Intraday-Trendbewegungen mit starkem Momentum. Sie zeichnet sich durch wissenschaftliche Stoppsetzung aus, und die Bausteinindikatoren können Trendwechsel frühzeitig erkennen. Durch Parameteranpassungen kann sie an verschiedene Marktbedingungen angepasst werden – eine trendfolgende Strategie, die sich für den Live-Handel lohnt.

/*backtest

start: 2022-12-20 00:00:00

end: 2023-12-26 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Lancelot vstop intraday strategy", overlay=true, currency=currency.NONE, initial_capital = 100, commission_type=strategy.commission.percent,

commission_value=0.075, default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

- 1