Momentum-Indikator-Crossover-Reversal-Trendfolgestrategie

Überblick

Diese Strategie kombiniert mehrere Momentum-Indikatoren wie MACD, RSI und ADX, um Preisumkehrsignale zu identifizieren. Sie verfolgt einen konträren Ansatz, indem sie bei starken Trendwenden gegen den Trend eingeht. Gleichzeitig werden Stop-Loss und Take-Profit gesetzt, um Gewinne zu sichern und Risiken zu kontrollieren.

Strategieprinzip

Die Strategie analysiert zunächst, ob der schnelle und der langsame gleitende Durchschnitt des MACD einen goldenen oder toten Kreuz bilden, um den Preistrend zu beurteilen. Anschließend wird der RSI verwendet, um falsche Ausbrüche zu filtern und sicherzustellen, dass ein Handelssignal erst dann generiert wird, wenn eine echte Preisumkehr stattgefunden hat. Schließlich prüft der ADX erneut, ob der Preis in einen Trend eingetreten ist. Nur wenn mehrere dieser Bedingungen gleichzeitig erfüllt sind, wird ein Kauf- oder Verkaufssignal generiert.

Im Einzelnen: Ein Kaufsignal entsteht, wenn die schnelle MACD-Linie die langsame von unten kreuzt, der RSI über 50 liegt und wieder ansteigt, und der ADX über 20 liegt. Ein Verkaufssignal entsteht, wenn die schnelle MACD-Linie die langsame von oben kreuzt, der RSI unter 50 liegt und fällt, und der ADX über 20 liegt.

Vorteilsanalyse

Der größte Vorteil dieser Strategie liegt in der Kombination mehrerer Indikatoren, die effektiv Seitwärtsmärkte und Fehlsignale ausfiltern und echte Trendwendepunkte identifizieren, was zu einer höheren Gewinnrate führt. Zudem werden Stop-Loss und Take-Profit gesetzt, um Gewinne zu sichern und Risiken zu kontrollieren, was eine wirksame Absicherung gegen unerwartete Ereignisse darstellt.

Risikoanalyse

Das größte Risiko dieser Strategie besteht in einer Fehleinschätzung der Trendumkehr, z. B. durch tiefe Preiskorrekturen, die zu Fehlentscheidungen führen können. Darüber hinaus könnte die neue Trendrichtung nach der Umkehr nicht ausreichend nachhaltig sein, um ausreichende Gewinne zu erzielen.

Lösungsansätze sind die weitere Optimierung der Parameter, die Anpassung der Stop-Loss-Spannen oder die Einbindung zusätzlicher Hilfsindikatoren zur Signalfilterung.

Optimierungsmöglichkeiten

Diese Strategie kann in folgenden Bereichen weiter optimiert werden:

-

Optimierung der Parameterkombination von MACD und RSI, um die Genauigkeit der Preisumkehrbewertung zu erhöhen.

-

Hinzufügen weiterer Indikatoren wie KD oder Bollinger-Bänder (BOLL), um eine Indikator-Umfeldwirkung zu erzielen.

-

Dynamische Anpassung der Stop-Loss-Spanne je nach Marktsituation.

-

Anpassung des Take-Profit-Niveaus in Echtzeit basierend auf der tatsächlichen Kursentwicklung nach der Umkehr.

Zusammenfassung

Diese Strategie nutzt eine Kombination mehrerer Momentum-Indikatoren, um potenzielle Preisumkehr-Chancen zu identifizieren. Durch Parameteroptimierung, die Einbindung weiterer Hilfsindikatoren und dynamische Anpassungen von Stop-Loss und Take-Profit kann die Stabilität und Zuverlässigkeit der Strategie weiter verbessert werden, um die verschiedenen Handelsmöglichkeiten des Marktes zu nutzen.

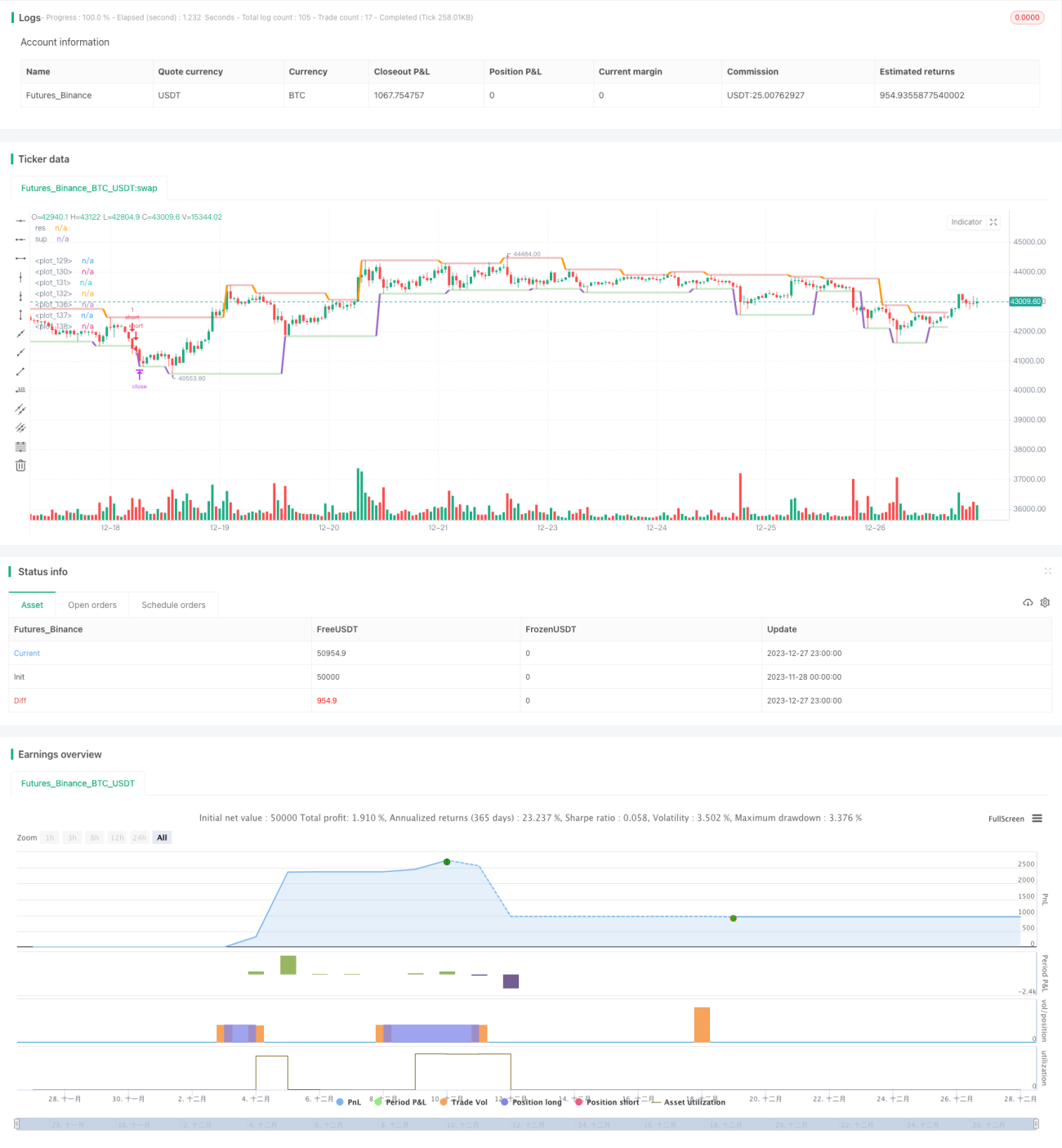

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © AHMEDABDELAZIZZIZO

//@version=5- 1