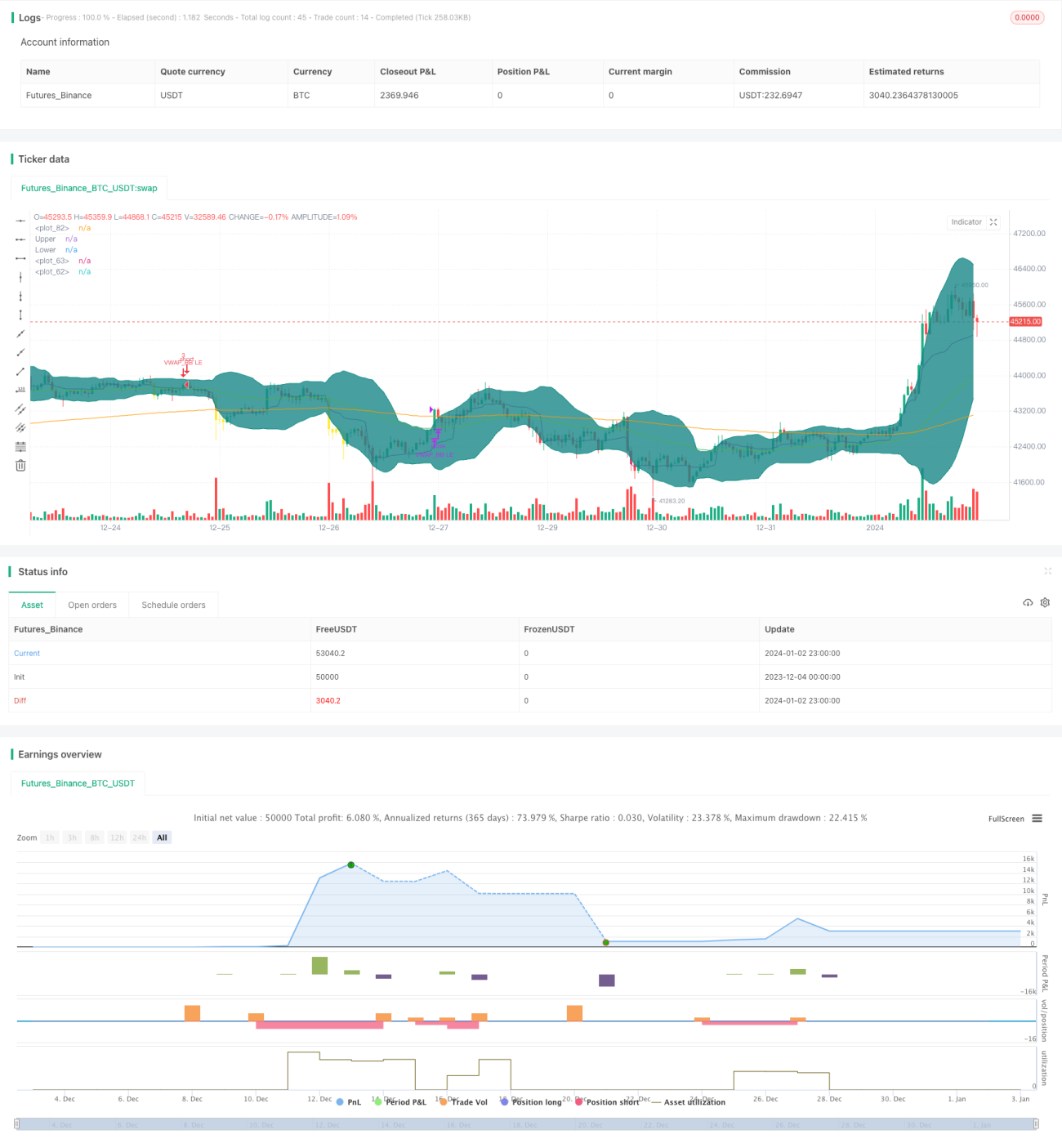

Quantitative Handelsstrategie basierend auf Bollinger-Bändern und VWAP

Übersicht

Diese Strategie kombiniert die beiden Indikatoren Bollinger-Bänder (BB) und Volume-Weighted Average Price (VWAP), um Kauf- und Verkaufsentscheidungen zu treffen. Sie erkennt kurzfristige Preisabweichungen und handelt darauf – ideal für den kurzfristigen Handel.

Strategieprinzip

Die Strategie basiert auf den folgenden Regeln für Kauf und Verkauf:

-

Die schnelle EMA-Linie liegt über der langsamen EMA-Linie – dies dient als Vorbedingung zur Trendbewertung.

-

Wenn der Schlusskurs über dem VWAP liegt, wird ein Preisanstieg erkannt und gekauft.

-

Wenn eine der letzten 10 Kerzen einen Schlusskurs unterhalb des unteren Bollinger-Bandes aufweist, wird eine Preisabweichung erkannt und gekauft.

-

Wenn der Schlusskurs über dem oberen Bollinger-Band liegt, wird eine Trendumkehr erkannt und verkauft.

Im Detail prüft die Strategie zunächst, ob der 50-Tage-EMA über dem 200-Tage-EMA liegt (schnelle und langsame EMA zur Bestimmung des übergeordneten Trends). Anschließend wird mit dem VWAP beurteilt, ob der Preis kurzfristig im Aufwärtstrend liegt. Schließlich werden die Bollinger-Bänder genutzt, um eine kurzfristige Abwärtsabweichung zu erkennen, die als Einstiegsgelegenheit dient.

Die Ausstiegsregel ist einfach: Sobald der Preis das obere Bollinger-Band überschreitet, wird eine Trendumkehr angenommen und ausgestiegen.

Vorteilsanalyse

Die Strategie kombiniert mehrere Indikatoren, um Preisabweichungen zu identifizieren, was die Treffsicherheit der Einstiegssignale erhöht. Die Verwendung der EMA zur Bestimmung des übergeordneten Trends verhindert Handel gegen den Trend. Die Einbeziehung des VWAP ermöglicht es, kurzfristige Preissteigerungen zu nutzen. Die Bollinger-Bänder helfen, präzise Einstiegszeitpunkte für den kurzfristigen Handel zu finden.

Risikoanalyse

- Ungenaue Trendbestimmung durch die EMA kann zu konträrem Handel zum Gesamtmarkt führen.

- Der VWAP-Indikator ist am effektivsten bei stündlichen oder Intraday-Daten; bei Tagesdaten verringert sich die Wirksamkeit.

- Ungeeignete Einstellungen der Bollinger-Bänder – zu breite oder zu enge Grenzen – führen zu verpassten Signalen.

Diesen Risiken kann durch Anpassung der EMA-Parameter oder den Einsatz anderer Indikatoren zur Trendbestimmung begegnet werden. Der VWAP sollte auf Intraday-Daten angewendet oder durch andere kurzfristige Indikatoren ersetzt werden. Die Bollinger-Band-Parameter sollten optimiert werden, um die ideale Bandbreite zu finden.

Optimierungsmöglichkeiten

- Alternative Indikatoren zur Trendbestimmung testen, z. B. MACD.

- Optimierung der EMA- und Bollinger-Band-Parameter für die beste Konfiguration.

- Einführung einer Stop-Loss-Mechanik.

- Kombination mit anderen Indikatoren zur Filterung falscher Signale.

- Testen verschiedener Handelsinstrumente und Zeitrahmen.

Zusammenfassung

Diese Strategie kombiniert die beiden Indikatoren Bollinger-Bänder und VWAP, um kurzfristige Preisabweichungen als Einstiegszeitpunkte zu identifizieren. Die EMA dient der Bestimmung des übergeordneten Trends und verhindert Handel gegen diesen. Sie ermöglicht eine schnelle Erkennung kurzfristiger Preistrendchancen und eignet sich für den Intraday- und kurzfristigen Handel. Durch Parameteroptimierung und die Integration weiterer Indikatoren können Stabilität und Rentabilität der Strategie weiter gesteigert werden.

- 1