Oszillationshandelsstrategie basierend auf zwei gleitenden Durchschnitten

Überblick

Diese Strategie ist eine auf gleitenden Durchschnitten basierende Range-Trading-Strategie. Sie nutzt den Crossover eines schnellen gleitenden Durchschnitts (Fast Moving Average) und eines langsamen gleitenden Durchschnitts (Slow Moving Average) als Kauf- und Verkaufssignale. Ein Kaufsignal wird erzeugt, wenn der schnelle gleitende Durchschnitt von unten den langsamen gleitenden Durchschnitt kreuzt; ein Verkaufssignal wird erzeugt, wenn der schnelle gleitende Durchschnitt von oben den langsamen gleitenden Durchschnitt kreuzt. Diese Strategie eignet sich für Seitwärtsmärkte und kann kurzfristige Preisschwankungen zur Gewinnerzielung nutzen.

Strategie-Prinzip

Die Strategie verwendet einen RMA mit einer Länge von 6 als schnellen gleitenden Durchschnitt und einen HMA mit einer Länge von 4 als langsamen gleitenden Durchschnitt. Anhand des Crossovers der schnellen und der langsamen Linie wird der Preistrend identifiziert und ein Handelssignal generiert.

Wenn die schnelle Linie von unten die langsame Linie kreuzt, deutet dies auf eine kurzfristige Umkehr von fallenden zu steigenden Kursen hin – ein günstiger Zeitpunkt für einen Positionswechsel. Daher generiert die Strategie zu diesem Zeitpunkt ein Kaufsignal. Wenn die schnelle Linie von oben die langsame Linie kreuzt, deutet dies auf eine kurzfristige Umkehr von steigenden zu fallenden Kursen hin – ebenfalls ein günstiger Zeitpunkt für einen Positionswechsel. Daher generiert die Strategie zu diesem Zeitpunkt ein Verkaufssignal.

Zusätzlich prüft die Strategie den längerfristigen Trend, um gegenläufige Trades zu vermeiden. Nur wenn der längerfristige Trend das Signal ebenfalls bestätigt, werden tatsächliche Kauf- und Verkaufssignale generiert.

Vorteile der Strategie

Die Strategie bietet folgende Vorteile:

- Der Doppel-Gleitenden-Durchschnitts-Crossover ermöglicht eine effektive Identifizierung kurzfristiger Preisumkehrpunkte.

- Die Kombination der Längen von schnellem und langsamem Durchschnitt erzeugt recht genaue Handelssignale.

- Die Einbeziehung der kurz- und langfristigen Trendbeurteilung filtert die meisten Rauschtsignale heraus.

- Die Implementierung von Take-Profit- und Stop-Loss-Logik ermöglicht eine aktive Risikovermeidung.

- Die Strategie ist leicht verständlich und umsetzbar, daher ideal für Anfänger im quantitativen Handel.

Risiken und Lösungsansätze

Die Strategie birgt auch einige Risiken:

- Der Doppel-Gleitenden-Durchschnitts-Ansatz kann zu vielen kleinen Gewinnen, aber einem großen Verlust führen. Lösung: Anpassung der Take-Profit- und Stop-Loss-Niveaus.

- In Seitwärtsmärkten können häufige Signale zu übermäßigem Handel führen. Lösung: Lockerung der Handelsbedingungen zur Reduzierung der Transaktionen.

- Die Parameter der Strategie können leicht überoptimiert werden, was im Live-Handel zu schlechten Ergebnissen führen kann. Lösung: Robustheitstests der Parameter.

- Die Strategie performt in Trendmärkten schlecht. Lösung: Integration eines Trendbeurteilungsmoduls oder Kombination mit Trendstrategien.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen weiter optimiert werden:

- Aktualisierung der gleitenden Durchschnitte, z. B. Einsatz adaptiver Filter wie Kalman.

- Integration eines maschinellen Lernmoduls zur KI-gestützten Bestimmung von Kauf- und Verkaufspunkten.

- Hinzufügen eines Money-Management-Moduls zur Automatisierung der Risikosteuerung.

- Kombination mit Hochfrequenzfaktoren, um stärkere Handelssignale zu finden.

- Mehrfachprodukt- und marktübergreifender Arbitrage.

Zusammenfassung

Insgesamt handelt es sich bei dieser Range-Trading-Strategie mit zwei gleitenden Durchschnitten um einen typischen und praktischen quantitativen Handelsansatz. Sie ist sehr anpassungsfähig und bietet Anfängern eine gute Gelegenheit, viel über die Entwicklung von Handelsstrategien zu lernen. Gleichzeitig bietet sie erhebliches Verbesserungspotenzial und kann durch die Integration weiterer quantitativer Techniken optimiert werden, um bessere Ergebnisse zu erzielen.

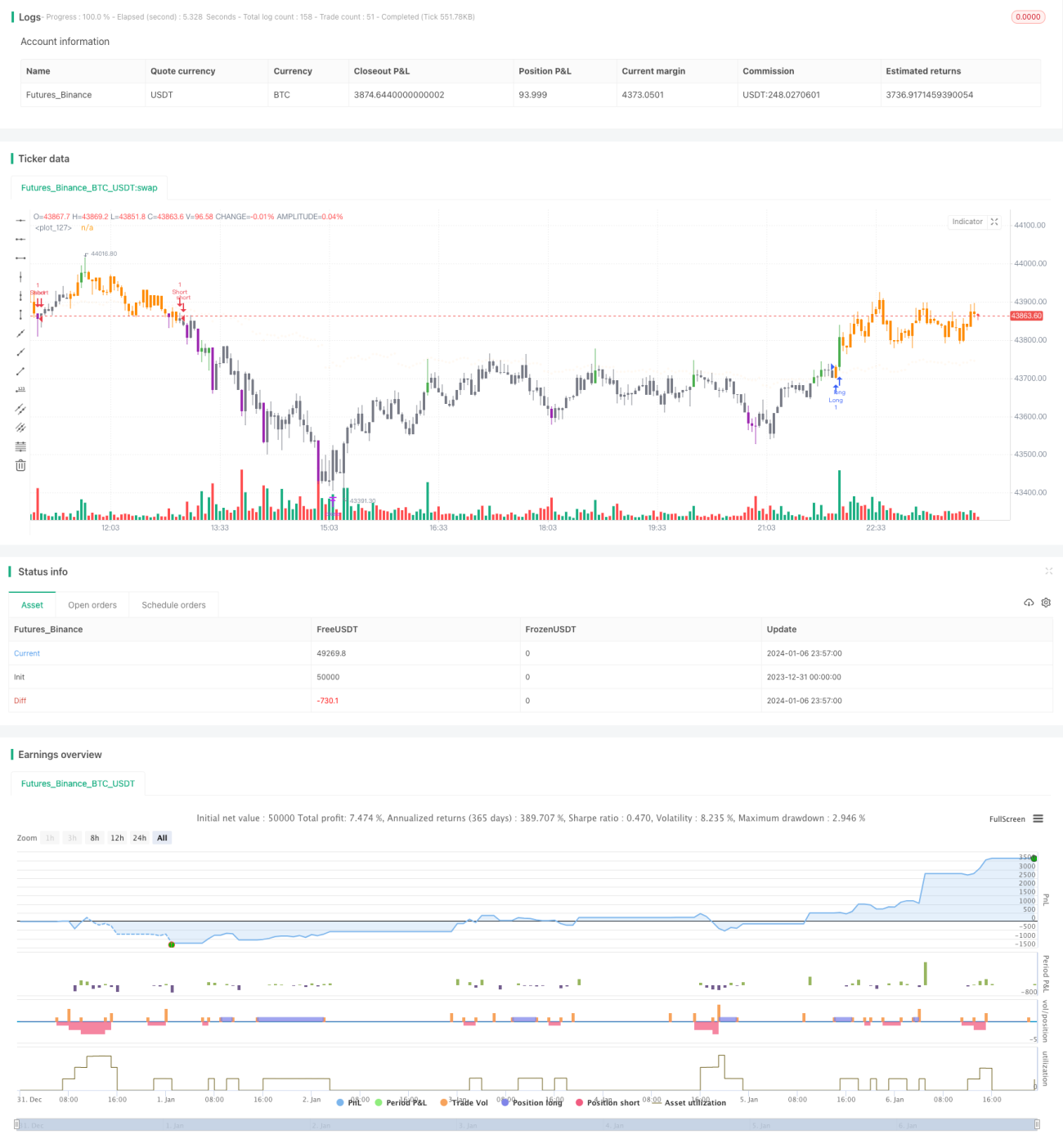

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © dc_analytics

// https://datacryptoanalytics.com/

- 1