Auf SSL basierte Trendfolgestrategie mit gleitendem Durchschnitt

Übersicht

Diese Strategie nutzt den SSL-Kanal-Indikator zur Bestimmung des Markttrends und folgt dem Trend auf Basis eines gleitenden Durchschnitts. Sie eignet sich für mittel- bis langfristige 4-Stunden- und Tages-Charts.

Strategieprinzip

-

Der SSL-Kanal setzt sich aus dem Kerzen-Durchschnitt (Keltner) und der tatsächlichen Volatilität zusammen. Er zeigt die Richtung des Markttrends an. Wenn der Preis die obere Linie durchbricht, ist dies ein bullishes Signal; bei einem Durchbruch der unteren Linie ein bärisches Signal.

-

Die Strategie verwendet gleitende Durchschnitte wie den EMA zur Berechnung einer Basislinie. Diese Linie filtert einige falsche Ausbrüche heraus.

-

Die Strategie geht long, wenn der Preis die obere SSL-Linie durchbricht, und short, wenn der Preis die untere SSL-Linie durchbricht. In einem Aufwärtstrend wird auf steigende Kurse gesetzt, in einem Abwärtstrend wird nach Tiefs gesucht („fallende Messer auffangen“).

-

Der Stop-Loss erfolgt über prozentuale Absicherung, ATR-Stop oder Lookback auf Tiefst-/Höchstkurse. Der Take-Profit ist ein Vielfaches des Stops. Die genauen Parameter werden vom Nutzer festgelegt.

Vorteile

-

Der SSL-Kanal erkennt Trendrichtungen präzise und reduziert Fehlsignale. Die Kombination mit gleitenden Durchschnitten als Einstiegssignal vermeidet Käufe an Spitzen und Verkäufe an Tiefs.

-

Verschiedene Arten gleitender Durchschnitte können flexibel gewählt werden, was sich an eine breitere Marktsituation anpassen lässt.

-

Die Stop-Loss-Methoden sind flexibel und vielseitig, das Risiko kontrollierbar. Auch der Take-Profit-Multiplikator kann je nach Präferenz angepasst werden.

-

Long- und Short-Positionen sind gleichzeitig möglich, sodass beide Marktrichtungen genutzt werden können.

Risikoanalyse

-

Gleitende Durchschnitte weisen eine Verzögerung auf, was zu kumulierten Verlusten führen kann.

-

In Seitwärtsmärkten können Ausbrüche aus dem SSL-Kanal schnell wieder umkehren, was zu Verlusten führt.

-

ATR- und Lookback-Stopps können bei außergewöhnlichen Ausbrüchen zu großzügig sein, sodass Verluste steigen.

Risikominderung:

- Anpassung der Parameter der gleitenden Durchschnitte oder Wahl einer anderen Art von gleitendem Durchschnitt.

- Vergrößerung des Stop-Loss-Abstands und sofortiges Stoppen bei Verlust.

- Hinzufügen eines Multiplikators zum ATR oder Anpassung des Lookback-Zeitraums.

Optimierungsrichtungen

- Testen weiterer Arten von gleitenden Durchschnitten, um die besten Parameter zu finden.

- Optimieren des ATR-Zeitraums für den Stop-Loss.

- Testen verschiedener Stop-Loss-Multiplikatoren.

- Testen unterschiedlicher Risikokoeffizienten für den Take-Profit.

Zusammenfassung

Diese Strategie kombiniert den SSL-Kanal zur Trendbestimmung und gleitende Durchschnitte zur Einstiegsbestätigung, um effektiv dem Trend zu folgen. Sie bietet flexible Stop-Loss- und Take-Profit-Methoden, die bei Risikokontrolle höhere Gewinne ermöglichen. Durch kontinuierliches Testen und Optimieren der Parameter kann eine bessere Handelsleistung erzielt werden. Es handelt sich um eine effektive Strategie, die langfristig verfolgt und eingesetzt werden sollte.

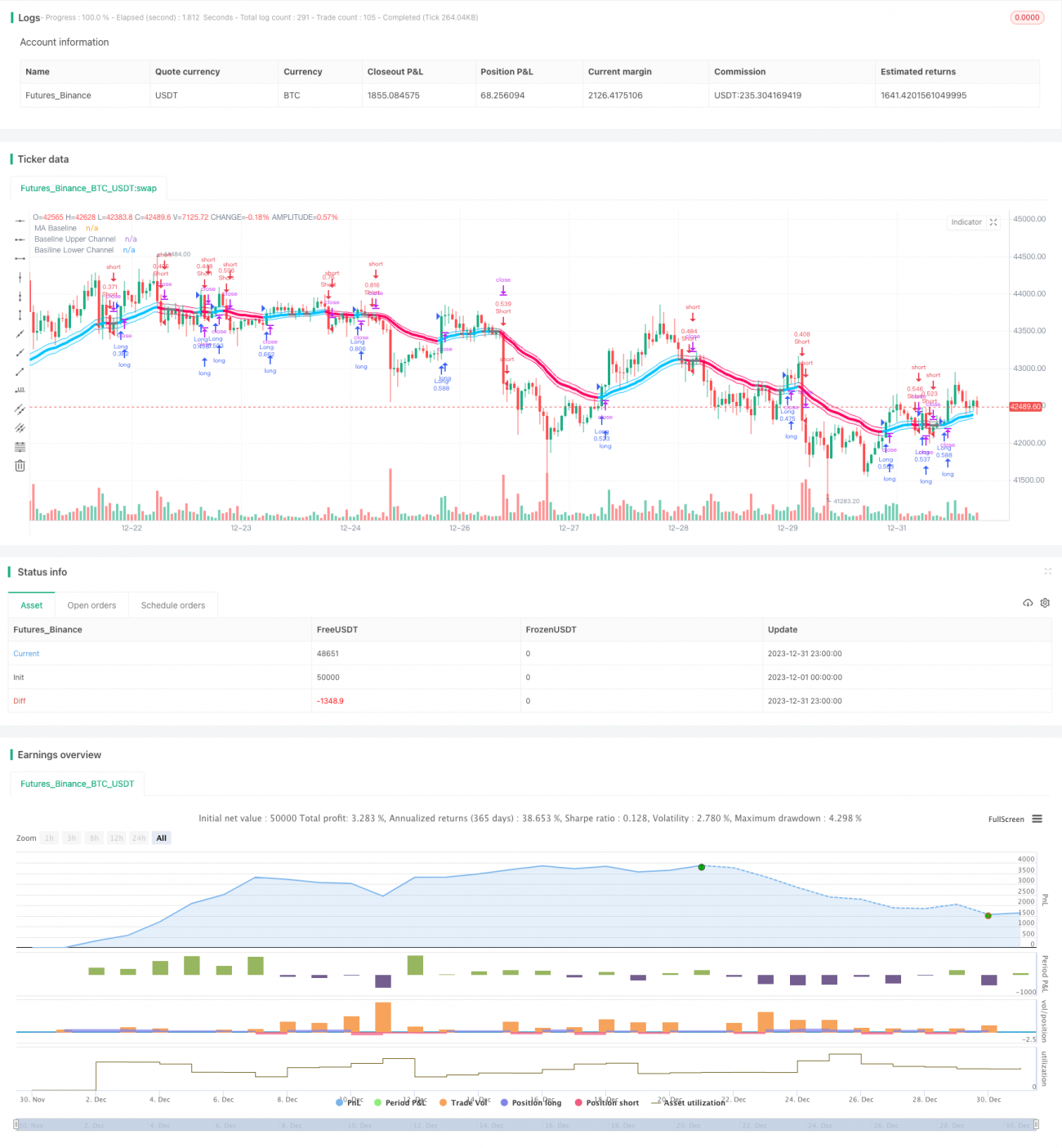

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Thanks to @kevinmck100 for opensource strategy template and @Mihkel00 for SSL Hybrid

// @fpemehd

// @version=5- 1