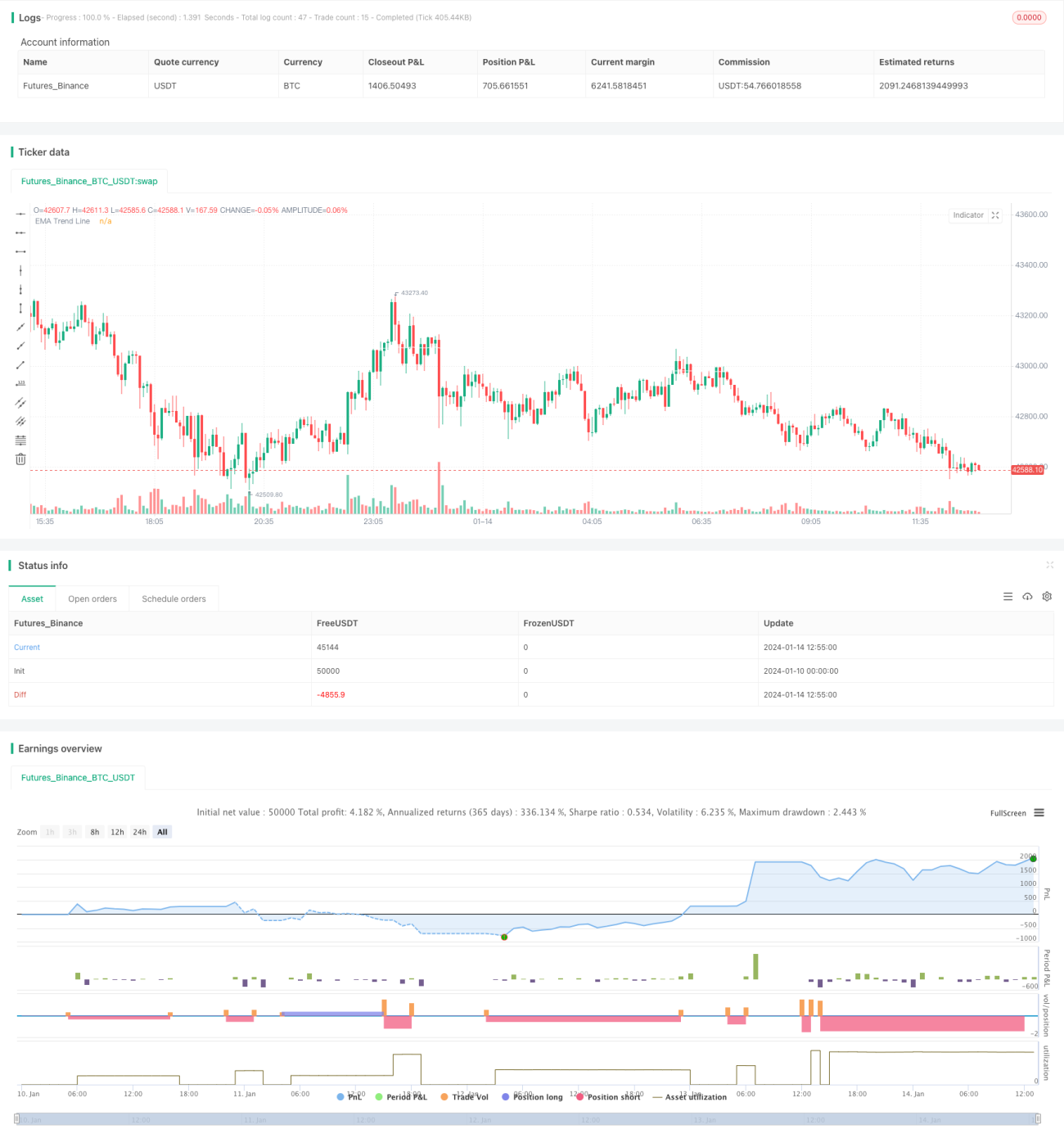

Trendfolgestrategie mit doppeltem EMA und RSI

Überblick

Diese Strategie nutzt eine Kombination aus doppelten EMAs und dem RSI-Indikator, um Preistrends zu identifizieren und rechtzeitig in den Markt einzusteigen, wenn sich die Trendrichtung ändert. Konkret wird mit einem längerfristigen EMA der übergeordnete Trend bestimmt, während der RSI kurzfristige überkaufte oder überverkaufte Bedingungen erkennt. Wenn der Preis in die Haupttrendrichtung zurückfällt, generiert der RSI ein Handelssignal, und je nach Trendrichtung wird eine Long- oder Short-Position eröffnet.

Funktionsweise der Strategie

- Ein 200-Perioden-EMA dient zur Bestimmung des übergeordneten Trends. Ein Kursanstieg über die EMA-Linie ist ein bullisches Signal, ein Kursrutsch unter die EMA-Linie ein bärisches Signal.

- Der RSI-Indikator wird auf einen Zeitraum von 10 Perioden eingestellt. Ein Anstieg des RSI über 40 gilt als überverkauftes Signal, ein Fall unter 60 als überkauftes Signal.

- Bei einem Aufwärtstrend (Kurs über der EMA-Linie) wird eine Long-Position eröffnet, wenn der RSI unter 40 fällt (überverkauftes Signal).

- Bei einem Abwärtstrend (Kurs unter der EMA-Linie) wird eine Short-Position eröffnet, wenn der RSI über 60 steigt (überkauftes Signal).

- Der Stop-Loss wird auf das 4-fache des ATR-Indikators gesetzt. Der Take-Profit beträgt das 2-fache des Stop-Loss, was einem Risiko-Ertrags-Verhältnis von 2:1 entspricht.

Vorteilsanalyse

Der größte Vorteil dieser Strategie liegt in der gleichzeitigen Kombination von Trend- und Umkehrindikatoren. Dadurch kann sie rechtzeitig in den Markt einsteigen, wenn der Trend zurückfällt, was zu guten Ergebnissen führt. Die spezifischen Vorteile sind:

- Die Verwendung eines doppelten EMA-Systems zur Bestimmung der Haupttrendrichtung ermöglicht eine effektive Verfolgung des Preistrends.

- Der RSI-Indikator erkennt kurzfristige überkaufte oder überverkaufte Situationen und unterstützt so die Entscheidung über den Einstiegszeitpunkt.

- Der Stop-Loss wird durch den ATR-Indikator festgelegt und kann je nach Marktvolatilität angepasst werden, was die Risikokontrolle verbessert.

- Die strikte Befolgung von Trendhandelsprinzipien reduziert unnötige Trades und senkt das systemische Risiko.

Risikoanalyse

Die Strategie birgt folgende Hauptrisiken:

- In Seitwärtsbewegungen oder sich abschwächenden Trends können falsche Handelssignale auftreten. In solchen Fällen ist eine vorsichtige Markteinschätzung und Zurückhaltung beim Einstieg erforderlich.

- In extremen Marktsituationen kann der durch den ATR festgelegte Stop-Loss zu groß oder zu klein sein und muss dynamisch angepasst werden. Alternativ könnten andere Stop-Loss-Methoden in Betracht gezogen werden.

- Die Häufigkeit der Handelssignale kann hoch sein; dies sollte mit den persönlichen Präferenzen bezüglich der Handelsfrequenz abgestimmt werden.

- Die Parameter des RSI sollten regelmäßig auf ihre Angemessenheit überprüft und bei Bedarf optimiert werden.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen verbessert werden:

- Es kann getestet werden, ob zusätzliche Trendindikatoren wie MACD zur Unterstützung der Trendbestimmung eingefügt werden.

- Andere Umkehrindikatoren wie KDJ oder Bollinger-Bänder könnten mit dem RSI kombiniert werden, um bessere Handelssignale zu finden.

- Maschinelles Lernen könnte eingesetzt werden, um Parameter adaptiv anzupassen und dynamische Stop-Loss- und Take-Profit-Niveaus zu erreichen.

- Stimmungsindikatoren, Nachrichten und weitere Faktoren könnten in die Entscheidungsfindung einbezogen werden, um die Gesamtrobustheit des Systems zu erhöhen.

Zusammenfassung

Insgesamt handelt es sich bei dieser Strategie um eine sehr typische kurzfristige Strategie, die Trendfolge mit Umkehrindikatoren kombiniert. Durch den Einsatz eines doppelten EMAs zur Bestimmung des Haupttrends und die Nutzung der Umkehreigenschaften des RSI wird versucht, Pullback-Chancen im Trend zu ergreifen. Vom Prinzip her vereint die Strategie die Vorteile verschiedener Indikatoren und schafft so eine gute komplementäre Wirkung. Wenn sie später durch Parameteroptimierung, Modellfusion und andere Verbesserungen weiterentwickelt wird, besteht noch großes Potenzial für eine Steigerung der Effektivität.

- 1