Kurzfristige quantitative Strategie auf Basis von RSI und VWAP

Überblick

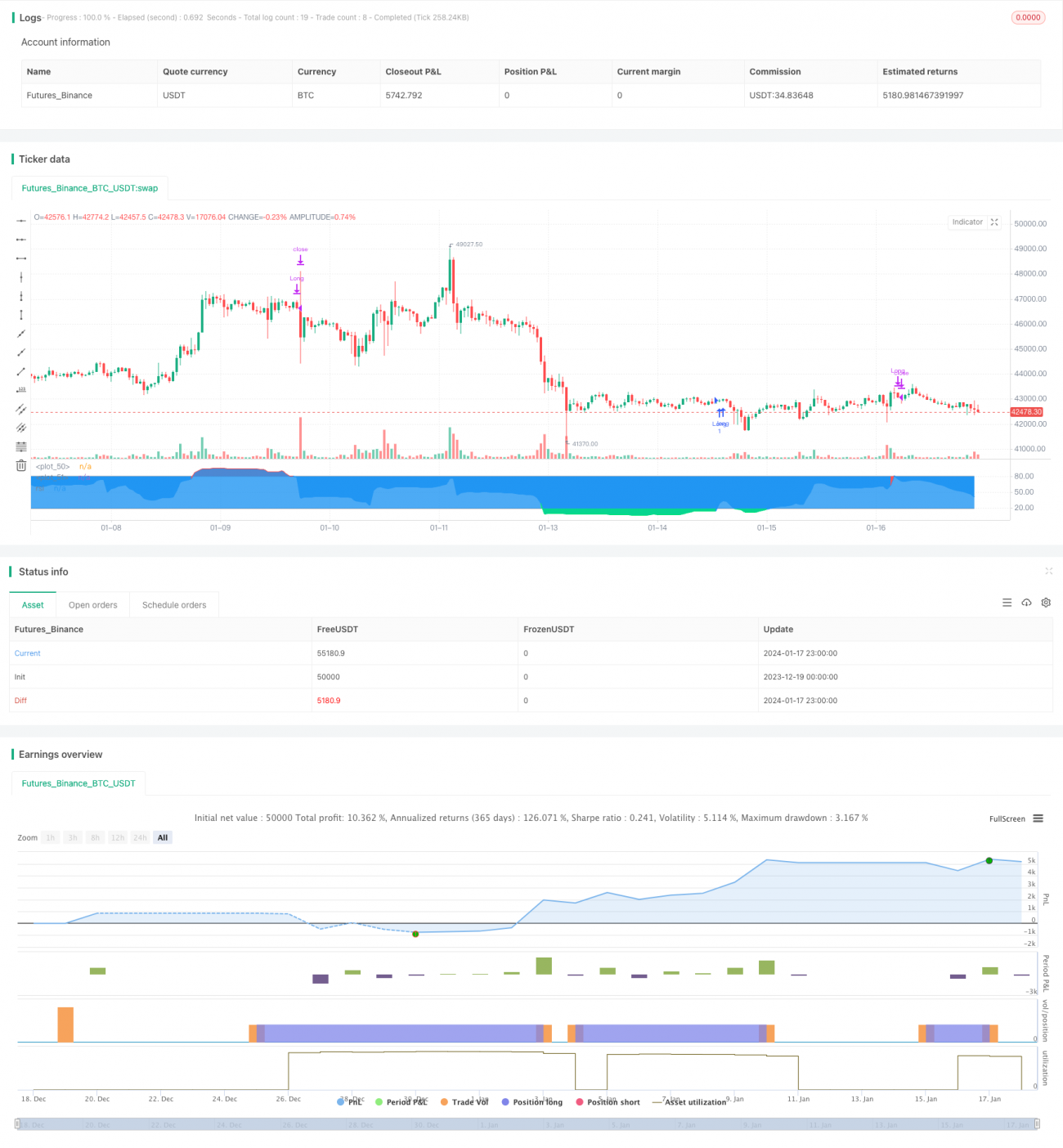

Diese Strategie trägt den Namen "RSI-VWAP-Kurzfriststrategie". Sie verwendet den RSI-Indikator und den volumengewichteten Durchschnittspreis (VWAP) als technische Indikatoren, definiert Long- und Short-Signale und generiert darauf basierend Kauf- und Verkaufsentscheidungen. Die Strategie zielt darauf ab, auf kurzfristiger Basis überkaufte und überverkaufte Marktsituationen zu erfassen, um Überrenditen zu erzielen.

Strategieprinzip

- Der RSI-Indikator wird verwendet, um zu beurteilen, ob der Markt überkauft oder überverkauft ist. Ein RSI-Wert über 80 gilt als überkaufter Bereich, unter 20 als überverkaufter Bereich.

- Der RSI-Indikator verwendet VWAP anstelle des Schlusskurses als Quelldaten. VWAP spiegelt den volumengewichteten Durchschnittspreis des Tages besser wider.

- Ein Kaufsignal wird generiert, wenn der RSI-Wert von unten den überverkauften Bereich (20) überschreitet. Ein Verkaufssignal wird generiert, wenn der RSI-Wert von oben den überkauften Bereich (80) unterschreitet.

- Die Strategie geht nur Long, nicht Short. Das bedeutet, sie kauft nur bei Überverkauf und verkauft nur bei Überkauf.

Vorteilsanalyse

- Die Verwendung von VWAP als Datenquelle für den RSI macht die Marktbeurteilung durch den RSI genauer und vermeidet Fehlinterpretationen durch falsche Ausbrüche.

- Nur Long-Positionen zu halten reduziert die Handelsfrequenz und begünstigt langfristig stabile Erträge.

- Der RSI-Parameter von 17 eignet sich für kurzfristige Trades.

- Die kurzfristige Handelsweise mit einer nicht zu hohen erwarteten Anzahl von Trades senkt die Transaktionskosten und begünstigt höhere Renditen.

Risikoanalyse

- Backtests quantitativer Strategien bergen das Risiko der Überanpassung, sodass die tatsächlichen Ergebnisse von den Backtests abweichen können.

- Die reine Long-Strategie kann Chancen in Abwärtstrends nicht nutzen.

- Die Kriterien für überkaufte/überverkaufte Bereiche sind möglicherweise nicht für alle Instrumente geeignet und müssen je nach Instrument angepasst werden.

- Jeder technische Indikator kann Fehlsignale erzeugen, Verluste sind nicht vollständig vermeidbar.

Durch eine moderate Anpassung der überkauften/überverkauften Schwellen, die Kombination mit anderen Indikatoren zur Signalbestätigung und die Anpassung der Parameterbereiche können Risiken reduziert werden.

Optimierungsmöglichkeiten

- Testen verschiedener Parameter auf die Strategieergebnisse, Optimierung der RSI-Länge und der Schwellen für überkaufte/überverkaufte Bereiche.

- Hinzufügen einer Stop-Loss-Strategie, z. B. durch nachlaufende Stopps oder zeitbasierte Stopps, um Teile der Gewinne zu sichern und Drawdowns zu reduzieren.

- Signalvalidierung durch Kombination mit anderen Indikatoren, um die Signalgenauigkeit zu erhöhen.

- Festlegung individueller Parameterbereiche je nach Instrument, damit die Strategie sich besser an verschiedene Produkte anpassen kann.

Zusammenfassung

Insgesamt handelt es sich bei dieser Strategie um eine einfache und praktische kurzfristige Strategie. Die Verwendung von VWAP macht die RSI-Beurteilung genauer, und die reine Long-Positionierung reduziert die Handelsfrequenz. Die Strategie ist klar konzipiert, leicht verständlich und umsetzbar und eignet sich für Einsteiger im quantitativen Handel. Allerdings kann keine auf einem einzelnen Indikator basierende Strategie perfekt sein; sie muss ständig optimiert werden, um bessere Ergebnisse im Live-Handel zu erzielen.

/*backtest

start: 2023-12-19 00:00:00

end: 2024-01-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Xaviz

//#####©ÉÉÉɶN###############################################- 1