Quantitative Strategie der dynamischen Kombination von EMAs

Übersicht

Diese Strategie ist eine dynamische Kombinationsstrategie mit gleitenden Durchschnitten auf mehreren Zeitrahmen. Sie verwendet exponentielle gleitende Durchschnitte (EMA) unterschiedlicher Längen zur Trendbestimmung sowie zum Ein- und Ausstieg. Das „MAX“ im Strategienamen steht für die Verwendung mehrerer EMAs, und „dynamisch“ bedeutet, dass die EMA-Längen anpassbar sind.

Strategieprinzip

Die Strategie verwendet 7 EMAs mit unterschiedlicher Geschwindigkeit, von der schnellsten zur langsamsten: 3-Perioden-, 15-Perioden-, 19-Perioden-, 50-Perioden-, 100-Perioden-, 150-Perioden- und 200-Perioden-EMA. Diese 7 EMAs bilden eine treppenförmige Anordnung. Bei der Generierung von Long- und Short-Signalen muss der Schlusskurs nacheinander diese 7 EMAs durchbrechen, um einen starken Einstieg nach einer Trendwende sicherzustellen.

Darüber hinaus kombiniert die Strategie die Bedingungen eines neuen Höchstkurses und eines Schlusskurses, der das historische Hoch übertrifft, um Long-Signale zu bestätigen, sowie eines neuen Tiefstkurses und eines Schlusskurses, der das historische Tief durchbricht, um Short-Signale zu bestätigen. Dadurch werden Fehldurchbrüche vermieden.

Die Ausstiegsbedingung erfordert, dass der Schlusskurs nacheinander von den schnellen zu den langsamen EMAs durchbricht – dies deutet auf eine Trendumkehr hin. Oder der Tiefst- bzw. Höchstkurs der aktuellen Kerze bricht 4 EMAs – dies signalisiert eine sofortige Schließung der Position.

Vorteilsanalyse

- Die Verwendung von 7 EMAs mit unterschiedlicher Geschwindigkeit in einer Treppenanordnung ermöglicht eine präzisere Erkennung von Trendwendepunkten.

- Die Kombination von neuen Hoch- und Tiefständen mit historischen Höchst-/Tiefstständen für Long- bzw. Short-Signale vermeidet Fehldurchbrüche.

- Die strengen doppelten Ausstiegsbedingungen ermöglichen ein rechtzeitiges Stoppen von Verlusten.

Risikoanalyse

- Kein Stop-Loss gesetzt – es besteht ein erhebliches Verlustrisiko.

- Die doppelten Ausstiegsbedingungen können zu vorzeitigem Ausstieg führen.

- Kurze EMA-Perioden erzeugen mehr Rauschen, was die Handelsfrequenz und die Transaktionskosten erhöht.

Lösungsansätze:

- Festen Stop-Loss und Trailing-Stop-Loss setzen.

- Die Längen der Ausstiegs-EMAs anpassen, um die Strenge der doppelten Ausstiegsbedingungen zu verringern.

- Die EMA-Längen erhöhen, um die Handelsfrequenz zu reduzieren.

Optimierungsrichtungen

- Stop-Loss-Strategien hinzufügen, z. B. prozentualer Stop-Loss, Trailing-Stop-Loss usw.

- EMA-Parameter anpassen und nach optimalen Parameterkombinationen suchen.

- Weitere Indikatoren zur Filterung hinzufügen, z. B. MACD, ATR, KDJ, um die Signalqualität zu verbessern.

- Mit einer Swing-Trading-Strategie kombinieren, um untergeordnete Wellen im Trend zu erfassen.

- Ein Modul für das Risikomanagement einbauen.

Zusammenfassung

Die Strategie hat ein klares Konzept: Sie verwendet 7 EMAs unterschiedlicher Geschwindigkeit zur Trendbestimmung und verfügt über doppelte Ausstiegsbedingungen, die eine empfindliche Reaktion auf Trendumkehrungen ermöglichen. Allerdings fehlt ein Stop-Loss, wodurch ein enormes Verlustrisiko besteht. Zudem kann es zu vorzeitigem Ausstieg kommen. Zukünftig sollte die Strategie durch Stop-Loss, Parameteroptimierung, Indikatorfilterung und weitere Dimensionen verbessert werden, um ein stabiles und zuverlässiges quantitatives Handelssystem zu werden.

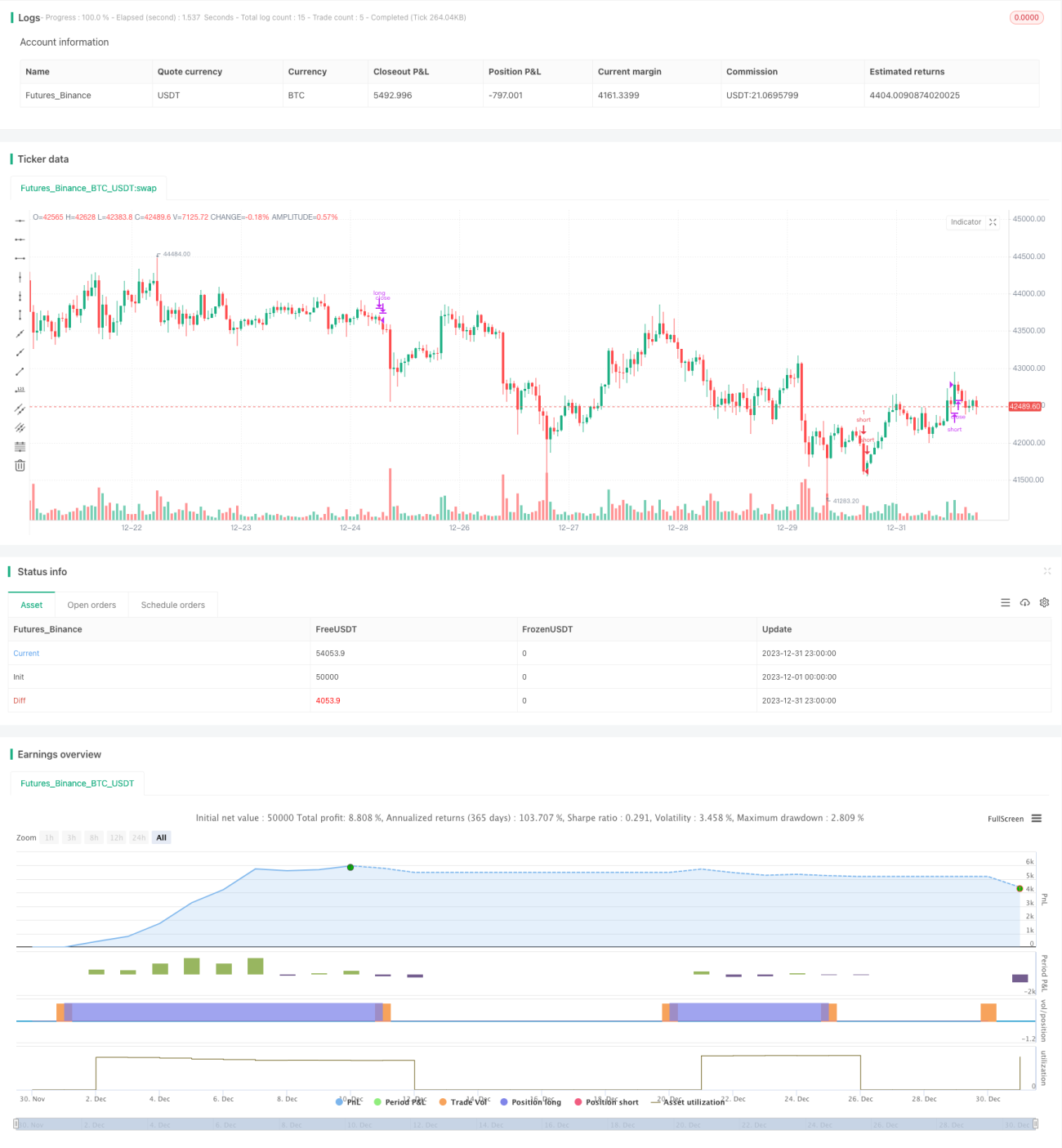

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Crypto MAX Trend", shorttitle="Crypto MAX", overlay = true )

Length = input(3, minval=1)

Length2 = input(15, minval=1)- 1