Multi-Timeframe-Trendfolgestrategie

Überblick

Die Multi-Timeframe-Trendfolgestrategie ist eine Trendfolgestrategie, die eine Vielzahl unterschiedlicher gleitender Durchschnitte und Regressionslinien kombiniert. Die Strategie kann unter mehr als 20 verschiedenen Trendindikatoren auswählen und automatische Kauf- und Verkaufssignale generieren.

Strategieprinzip

Der Kern der Strategie besteht darin, anhand des vom Benutzer gewählten Trendindikators zu beurteilen, ob sich der Preis in einem Aufwärts- oder Abwärtstrend befindet. Zunächst berechnet die Strategie über 20 gleitende Durchschnitte und Regressionslinien. Zu diesen Indikatoren gehören einfache gleitende Durchschnitte, gewichtete gleitende Durchschnitte, exponentielle gleitende Durchschnitte aus der Standardbibliothek der Pine-Script-Sprache sowie benutzerdefinierte Indikatoren aus der Pine-Community. Anschließend fragt die Strategie den aktuellen Wert eines bestimmten Indikators ab und vergleicht ihn mit dem Wert des vorherigen Zeitraums. Ist der aktuelle Wert größer als der vorherige, gilt der Trend als aufwärts gerichtet; ist der aktuelle Wert kleiner als der vorherige, gilt der Trend als abwärts gerichtet. Schließlich entscheidet die Strategie anhand der Trendrichtung, ob eine Long-Position eröffnet werden soll. In einem Aufwärtstrend wird eine Long-Position eröffnet, in einem Abwärtstrend wird die Position geschlossen.

Vorteilsanalyse

Die Strategie kombiniert über 20 Indikatoren zur Trendbestimmung und vermeidet so Fehleinschätzungen durch einen einzelnen Indikator. Zudem wurden diese Indikatoren von der Community-Entwicklern validiert. Sie können mit verschiedenen Parametern an unterschiedliche Marktbedingungen angepasst werden.

Im Vergleich zu einer einfachen Zwei-gleitenden-Durchschnitte-Strategie verlässt sich diese Strategie nur auf einen einzigen Indikator zur Bestimmung der Trendrichtung, was den Trend besser abbildet und falsche Signale, die bei gegensätzlichen Indikatoren auftreten, vermeidet.

Risikoanalyse

Die Strategie verlässt sich auf Indikatoren zur Trendbestimmung und kann nicht erkennen, ob der Trend bereits eine Wende vollzogen hat. Dies führt zu einer gewissen Verzögerung, die zu Verlusten oder verpassten Chancen führen kann. Dieses Problem kann durch Anpassung der Indikatorparameter gemildert werden.

Nach unerwarteten Ereignissen (z. B. Black-Swan-Ereignissen) erleiden alle trendfolgenden Strategien erhebliche Verluste. Es ist notwendig, einen Stop-Loss zur Risikobegrenzung festzulegen.

Optimierungsmöglichkeiten

Es kann in Betracht gezogen werden, andere Indikatoren zur Vorhersage von Trendwendungen zu kombinieren, um das Verzögerungsproblem zu reduzieren. Beispielsweise könnte der Bollinger-Band-Indikator verwendet werden, um zu beurteilen, ob der Preis übermäßig ausgedehnt ist.

Für unerwartete Ereignisse könnte ein Notfall-Stop-Loss-Mechanismus entwickelt werden, z. B. ein erzwungener Stop-Loss bei einem Tagesverlust von mehr als 5 %.

Zusammenfassung

Die Multi-Timeframe-Trendfolgestrategie kombiniert über 20 Indikatoren zur Trendbestimmung, kann Markttrends vollständig abbilden und falsche Signale vermeiden. Gleichzeitig bietet sie eine hohe Anpassbarkeit, sodass sie für stark unterschiedliche Marktbedingungen geeignet ist. Es handelt sich um eine sehr effektive Trendfolgestrategie. Durch die Festlegung geeigneter Stop-Loss-Werte und die Optimierung der Indikatorparameter können bei kontrolliertem Risiko gute Renditen erzielt werden.

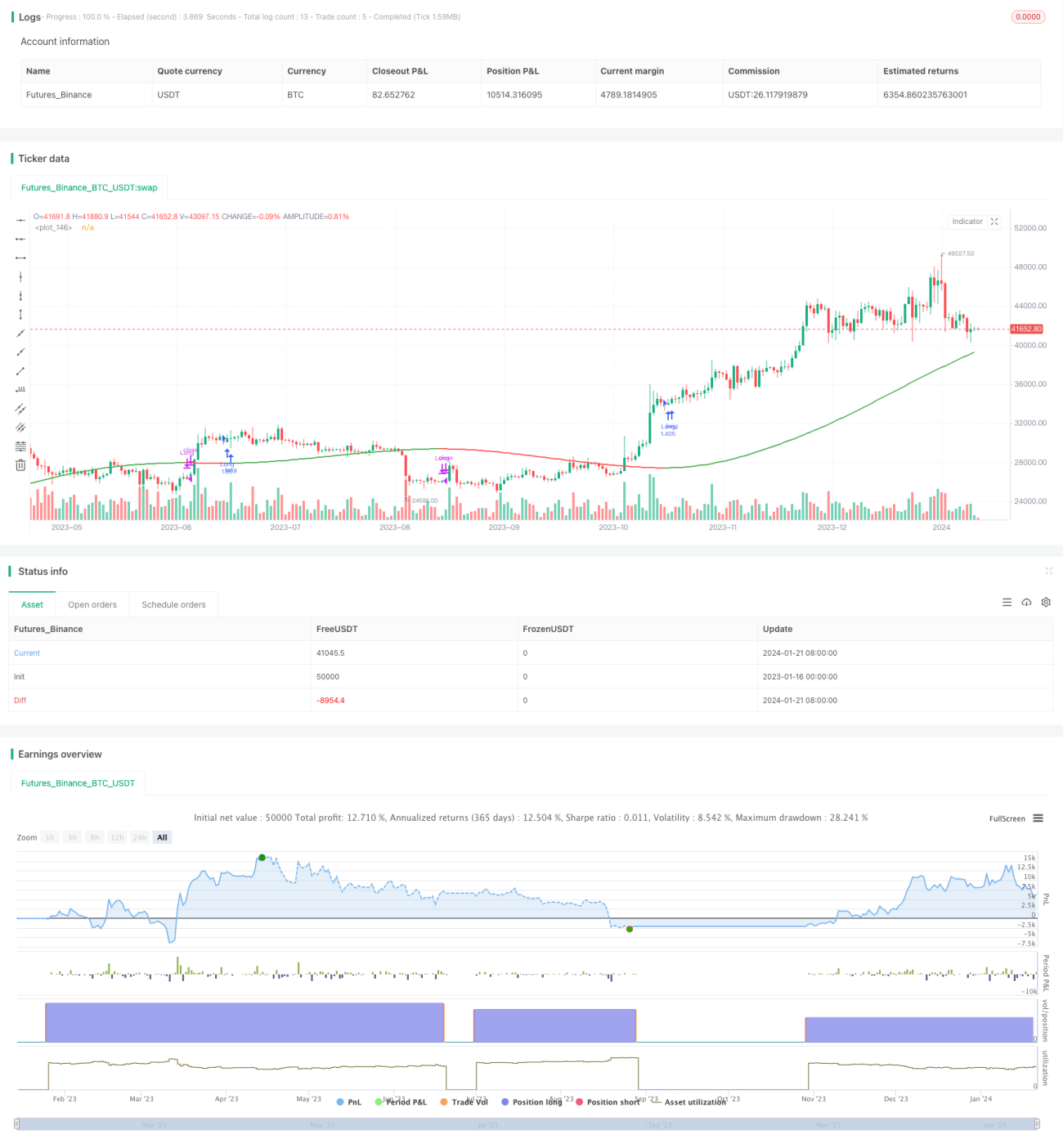

/*backtest

start: 2023-01-16 00:00:00

end: 2024-01-22 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// @version=5

// Author = TradeAutomation

- 1