Aktienhandel mit bidirektionaler Pyramidenstrategie basierend auf dem RSI-Indikator

Überblick

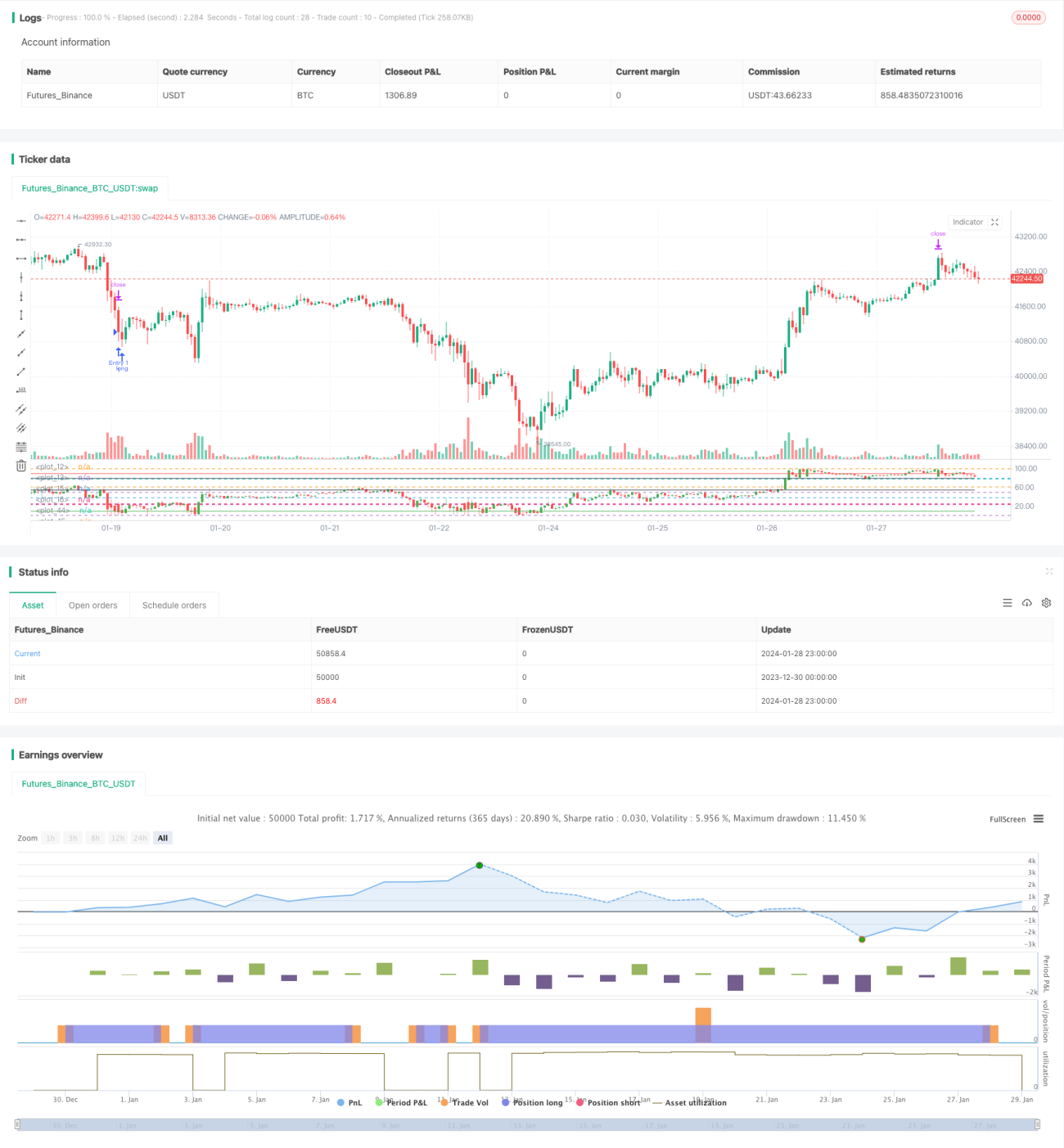

Dieser Artikel stellt eine auf dem Relative-Stärke-Index (RSI) basierende bilaterale Pyramid-Trading-Strategie für Aktien vor. Die Strategie nutzt den RSI zur Bestimmung überkaufter und überverkaufter Bereiche von Aktien und kombiniert diese mit dem Prinzip der Pyramiden-Nachkaufstrategie, um Gewinne zu erzielen.

Strategieprinzip

- Der RSI wird verwendet, um festzustellen, ob eine Aktie in den überkauften oder überverkauften Bereich eintritt. Ein RSI unter 25 gilt als überverkauft, über 80 als überkauft.

- Wenn der RSI in den überverkauften Bereich eintritt, wird eine Long-Position eröffnet. Wenn der RSI in den überkauften Bereich eintritt, wird eine Short-Position eröffnet.

- Es wird eine pyramidenförmige Nachkaufstrategie mit maximal 7 Nachkäufen verwendet. Nach jedem Nachkauf werden Take-Profit- und Stop-Loss-Punkte gesetzt.

Vorteile

- Durch die Verwendung des RSI zur Erkennung überkaufter und überverkaufter Gebiete können größere Kursumkehrchancen erfasst werden.

- Die Pyramiden-Nachkaufstrategie ermöglicht bei richtiger Marktbewegung eine höhere Rendite.

- Die Festlegung von Take-Profit und Stop-Loss nach jedem Nachkauf hilft, das Risiko zu kontrollieren.

Risikoanalyse

- Die Wirksamkeit des RSI bei der Erkennung von überkauften/überverkauften Zonen ist nicht stabil; es können Fehlsignale auftreten.

- Die Anzahl der Nachkäufe muss angemessen festgelegt werden; zu viele Nachkäufe erhöhen das Risiko.

- Der Stop-Loss-Punkt sollte unter Berücksichtigung der Volatilität gesetzt werden und darf nicht zu eng sein.

Optimierungsmöglichkeiten

- Es kann in Betracht gezogen werden, weitere Indikatoren zur Filterung der RSI-Signale zu kombinieren, um die Genauigkeit der Erkennung von Überkauf/Überverkauf zu verbessern, z. B. in Kombination mit KDJ, Bollinger-Bändern usw.

- Es kann ein nachlaufender Stop-Loss zur Kursverfolgung eingerichtet werden, der dynamisch an Volatilität und Risikokontrollanforderungen angepasst wird.

- Je nach Marktlage (Bullenmarkt, Bärenmarkt usw.) können adaptive Parameter verwendet werden.

Zusammenfassung

Diese Strategie kombiniert den RSI mit der Pyramiden-Nachkaufstrategie und kann bei der Erkennung von Überkauf/Überverkauf durch Nachkäufe zusätzliche Gewinne erzielen. Obwohl die Genauigkeit der RSI-Signale verbesserungswürdig ist, kann durch angemessene Parameteroptimierung und Kombination mit anderen Indikatoren eine stabile Handelsstrategie entwickelt werden. Die Strategie weist eine gewisse Allgemeingültigkeit auf und stellt eine relativ einfache und direkte Methode des quantitativen Handels dar.

- 1