Chan-Theorie-Strategie mit zwei gleitenden Durchschnitten

Überblick

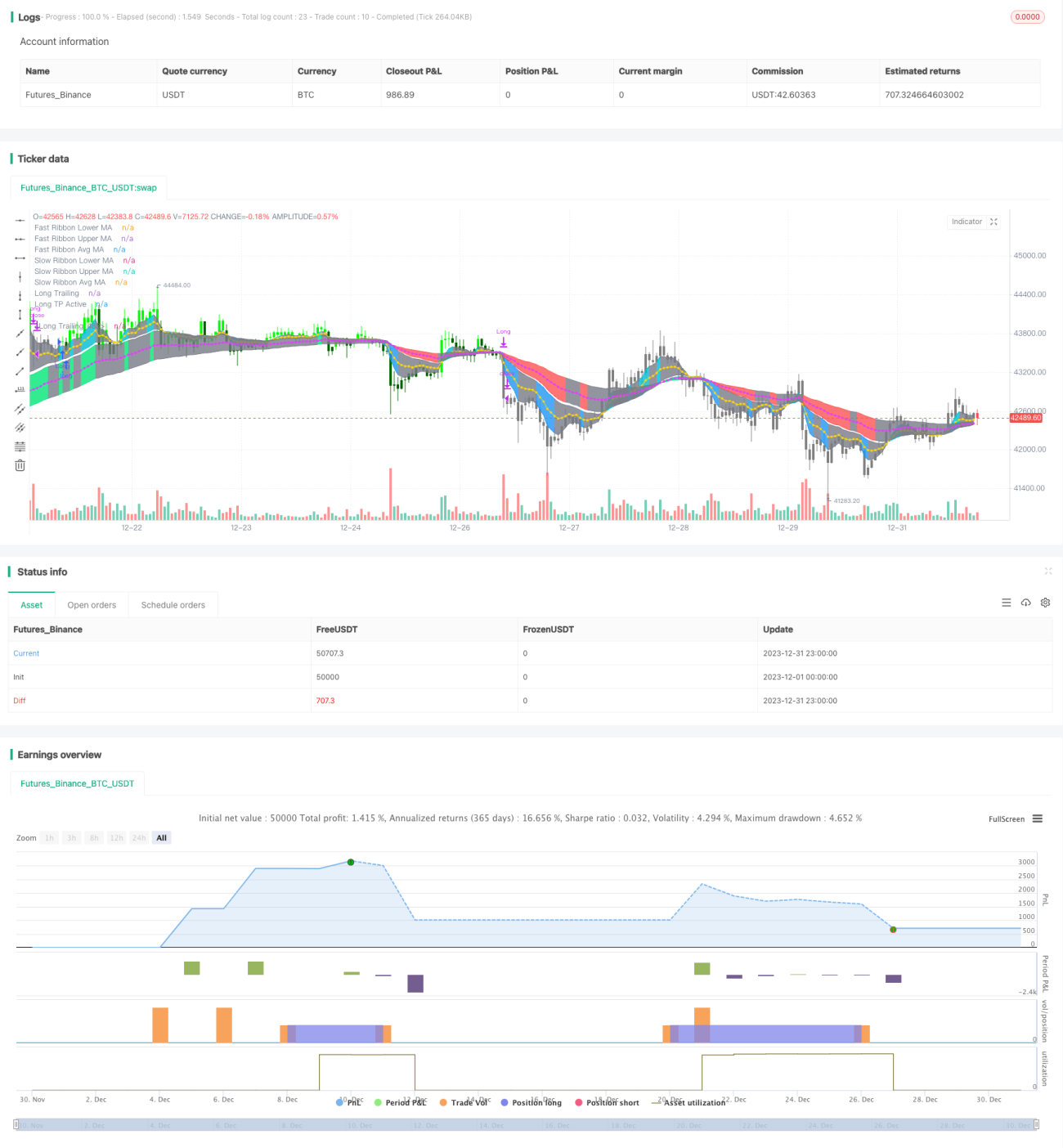

Die Doppel-Gleitenden-Durchschnitte-Chan-Theorie-Strategie (Double Moving Average Chan Theory Strategy) ist eine Trendfolgestrategie. Sie berechnet zwei Gruppen von gleitenden Durchschnitten, um eine schnelle und eine langsame Linie zu bilden, und kombiniert die Beziehung zwischen dem Preis und den gleitenden Durchschnitten, um die Trendrichtung zu bestimmen.

Wenn der schnelle gleitende Durchschnitt den langsamen von unten nach oben kreuzt, ist dies ein bullisches Signal. Wenn der schnelle gleitende Durchschnitt den langsamen von oben nach unten kreuzt, ist dies ein bärisches Signal. Die Strategie nutzt die Richtung der schnellen und langsamen gleitenden Durchschnitte sowie die Anzahl der Kerzen (Candles) des Preisausbruchs, um die genauen Ein- und Ausstiegszeitpunkte zu bestimmen.

Strategieprinzip

Die Doppel-Gleitenden-Durchschnitte-Chan-Theorie-Strategie berechnet zwei Gruppen von gleitenden Durchschnitten, die als Kriterien für die kurzfristige bzw. langfristige Trendbewertung dienen. Konkret definiert die Strategie:

- Eine schnelle Gruppe gleitender Durchschnitte, bestehend aus dem unteren Band und dem oberen Band des schnellen gleitenden Durchschnitts, repräsentiert den kurzfristigen Trend.

- Eine langsame Gruppe gleitender Durchschnitte, bestehend aus dem unteren Band und dem oberen Band des langsamen gleitenden Durchschnitts, repräsentiert den langfristigen Trend.

Die Strategie bestimmt die Plausibilität des kurz- und langfristigen Trends sowie die genauen Ein- und Ausstiegszeitpunkte anhand der Preisbeziehung zwischen der schnellen und der langsamen Gruppe gleitender Durchschnitte.

Einstiegsbedingungen:

- Wenn die obere Linie des schnellen gleitenden Durchschnitts die obere Linie des langsamen gleitenden Durchschnitts für mindestens zwei Kerzen (Candles) nach oben durchbricht, wird eine Long-Position eröffnet.

- Wenn die untere Linie des schnellen gleitenden Durchschnitts die untere Linie des langsamen gleitenden Durchschnitts für mindestens zwei Kerzen nach unten durchbricht, wird eine Short-Position eröffnet.

Ausstiegsbedingungen:

- Während einer Long-Position wird diese geschlossen, wenn der schnelle gleitende Durchschnitt den langsamen gleitenden Durchschnitt von oben nach unten kreuzt.

- Während einer Short-Position wird diese geschlossen, wenn der schnelle gleitende Durchschnitt den langsamen gleitenden Durchschnitt von unten nach oben kreuzt.

Zusätzlich enthält die Strategie Funktionen wie Take-Profit, Stop-Loss und Trailing-Stop zur Risikokontrolle.

Vorteilsanalyse

Die Hauptvorteile der Doppel-Gleitenden-Durchschnitte-Chan-Theorie-Strategie sind:

- Durch die Verwendung von zwei gleitenden Durchschnitten wird Marktrauschen effektiv gefiltert und die Trendrichtung präzise erfasst.

- Die Kombination von schnellen und langsamen gleitenden Durchschnitten mit der Preisbeziehung erhöht die Zuverlässigkeit der Signale.

- Die Strategie ist einfach und klar aufgebaut, leicht verständlich und umsetzbar, ideal für den quantitativen Handel.

- Die integrierten Instrumente zur Risikokontrolle wie Take-Profit, Stop-Loss und Trailing-Stop können Transaktionsrisiken effektiv begrenzen.

Risikoanalyse

Die Doppel-Gleitenden-Durchschnitte-Chan-Theorie-Strategie birgt jedoch auch gewisse Risiken, die sich wie folgt äußern:

- In Seitwärtsmärkten können falsche Signale entstehen, die unnötige Trades auslösen.

- Das System gleitender Durchschnitte reagiert träge auf unerwartete Ereignisse (z. B. stark positive/negative Nachrichten) und kann zu erheblichen Verlusten führen.

- Ein Trailing-Stop kann in bestimmten Marktphasen durchbrochen werden, was die Verluste vergrößert.

Um diese Risiken zu kontrollieren, können die Parameter der gleitenden Durchschnitte optimiert oder zusätzliche Indikatoren zur Filterung eingesetzt werden.

Optimierungsmöglichkeiten

Die Doppel-Gleitenden-Durchschnitte-Chan-Theorie-Strategie kann in folgenden Dimensionen optimiert werden:

- Optimierung der Parameter der gleitenden Durchschnitte durch Anpassung der Periodenlängen, um sie an unterschiedliche Marktzyklen anzupassen.

- Hinzufügen weiterer Indikatoren als Filter, um eine Multi-Indikator-Kombinationsstrategie zu schaffen und die Signalgenauigkeit zu erhöhen.

- Optimierung der Stop-Loss- und Take-Profit-Einstellungen durch Festlegung von Drawdown-Schwellenwerten zur Begrenzung maximaler Verluste.

- Einführung von Machine-Learning-Modellen zur Trendvorhersage, um den Einstiegszeitpunkt besser zu bestimmen.

Zusammenfassung

Insgesamt ist die Doppel-Gleitenden-Durchschnitte-Chan-Theorie-Strategie eine sehr praktische Trendfolgestrategie. Ihre Entscheidungsregeln sind einfach, die Logik klar, und sie nutzt das Zweilinien-System zur Risikokontrolle mit einer soliden theoretischen Grundlage. In Zukunft kann die Strategie durch Parameteroptimierung, verbesserte Risikokontrolle und andere Anpassungen weiter verbessert werden, um die Rentabilität und Stabilität zu steigern.

- 1