Überblick

Diese Strategie verfolgt einen momentumgestützten Ansatz über mehrere Zeitrahmen hinweg, indem sie die 123-Umkehr und den MACD-Indikator kombiniert. Die 123-Umkehr identifiziert kurzfristige Trendumkehrpunkte, während der MACD den mittel- bis langfristigen Trend bewertet. Die Kombination ermöglicht Signale, die kurzfristige Umkehrungen mit einem langfristigen Trendausblick verbinden – sowohl für Long- als auch für Short-Positionen.

Strategieprinzip

Die Strategie besteht aus zwei Teilen:

-

123-Umkehr-Teil: Ein Kaufsignal wird erzeugt, wenn die letzten beiden Kerzen ein Hoch/Tief bilden und der Stochastik-Indikator unter/über 50 liegt. Ein Verkaufssignal entsprechend bei umgekehrter Konstellation.

-

MACD-Teil: Ein Kaufsignal entsteht, wenn die schnelle Linie die langsame Linie von unten kreuzt; ein Verkaufssignal bei einem Kreuz von oben nach unten.

Die endgültigen Signale werden nur dann ausgegeben, wenn sowohl die 123-Umkehr als auch der MACD in die gleiche Richtung zeigen.

Vorteile

Die Strategie vereint kurzfristige Umkehrsignale mit mittel- bis langfristigen Trends. So kann sie von kurzfristigen Schwankungen profitieren, während sie gleichzeitig den übergeordneten Trend im Auge behält, was zu einer höheren Gewinnrate führt. Besonders in Seitwärtsmärkten filtert die 123-Umkehr einen Teil des Rauschens heraus und erhöht die Stabilität.

Durch die Anpassung der Parameter lässt sich das Verhältnis zwischen Umkehr- und Trendsignalen je nach Marktumfeld justieren.

Risikoanalyse

Die Strategie weist eine gewisse zeitliche Verzögerung auf – vor allem bei Verwendung eines MACD mit langer Periode, sodass kurzfristige Bewegungen verpasst werden können. Zudem sind Umkehrsignale von Natur aus mit einer gewissen Zufälligkeit behaftet, was zu Fehlsignalen führen kann.

Abhilfe schaffen eine Verkürzung der MACD-Periode oder der Einsatz eines Stop-Loss zur Risikokontrolle.

Optimierungsmöglichkeiten

Die Strategie lässt sich in folgenden Bereichen verbessern:

- Anpassung der Parameter der 123-Umkehr zur Optimierung der Umkehrsignale.

- Anpassung der MACD-Parameter zur Verbesserung der Trendbewertung.

- Hinzunahme weiterer Filterindikatoren zur Steigerung der Treffsicherheit.

- Integration einer Stop-Loss-Strategie zur Risikobegrenzung.

Zusammenfassung

Diese Strategie kombiniert technische Indikatoren verschiedener Parameter und Zeitrahmen und vereint die Vorteile von Umkehr- und Trendhandel durch momentumgestütztes Tracking über mehrere Zeitebenen. Sie kann durch Parametereinstellungen an verschiedene Märkte angepasst und durch zusätzliche Indikatoren oder Stop-Loss weiter optimiert werden – ein vielversprechender Strategieansatz.

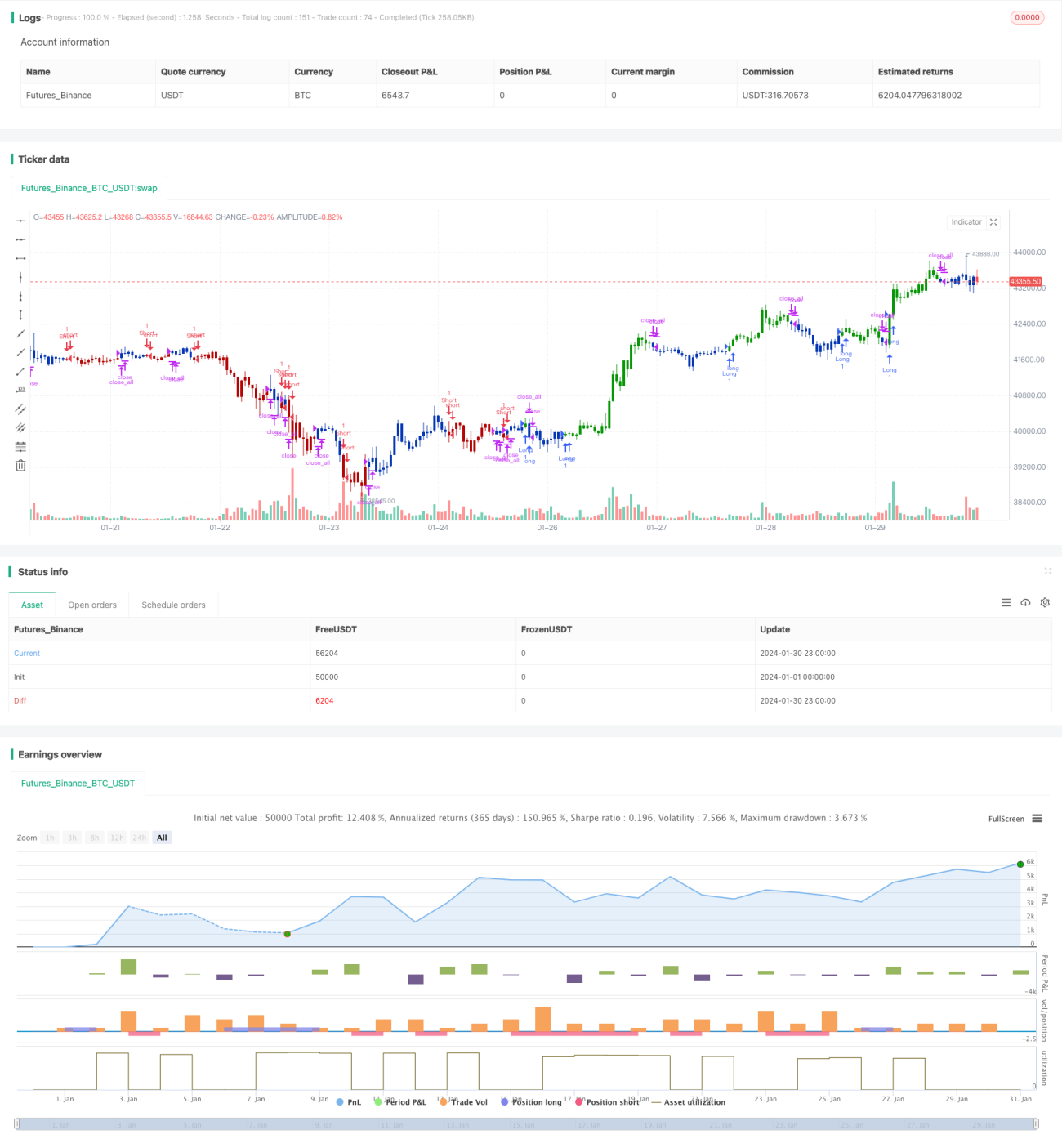

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 28/01/2021

// This is combo strategies for get a cumulative signal. - 1