Dynamische Stop-Loss-Bollinger-Bänder-Strategie

Überblick

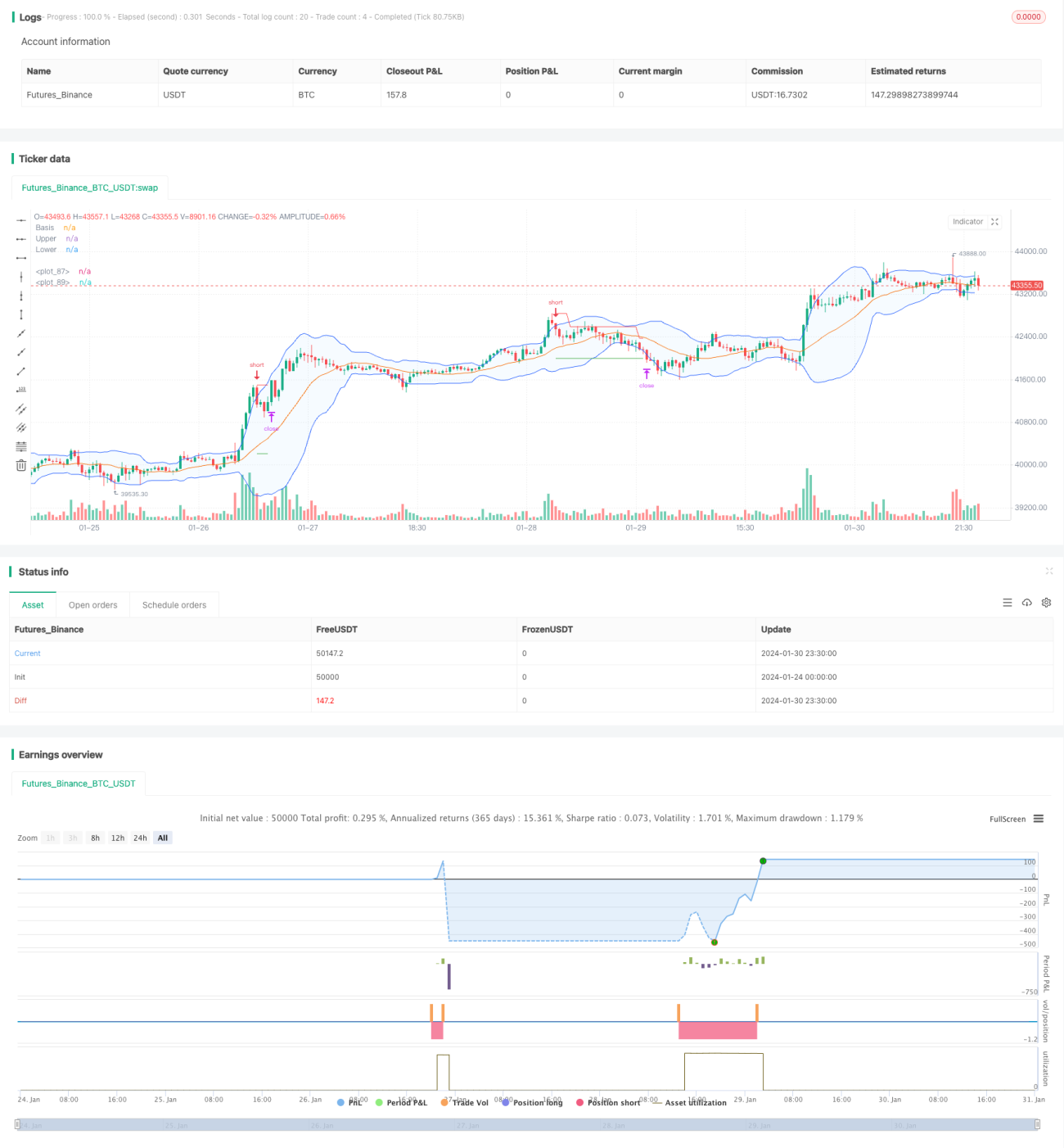

Diese Strategie nutzt die obere und untere Linie der Bollinger-Bänder, um eine dynamische Stop-Loss-Grenze zu realisieren. Wenn der Preis die obere Linie der Bollinger-Bänder durchbricht, wird eine Short-Position eröffnet; bei einem Durchbruch der unteren Linie wird eine Long-Position eröffnet. Es wird ein dynamischer Stop-Loss gesetzt, der der Kursbewegung folgt.

Prinzip

Der Kern dieser Strategie liegt in den oberen und unteren Linien der Bollinger-Bänder. Die mittlere Linie der Bollinger-Bänder ist der gleitende Durchschnitt über n Tage, die obere Linie ist die mittlere Linie plus k mal der Standardabweichung über n Tage, die untere Linie ist die mittlere Linie minus k mal der Standardabweichung über n Tage. Wenn der Preis von der unteren Linie nach oben abprallt, wird eine Long-Position eröffnet; wenn der Preis von der oberen Linie nach unten fällt, wird eine Short-Position eröffnet. Gleichzeitig wird in der Strategie eine Stop-Loss-Grenze festgelegt, die während der Kursentwicklung dynamisch angepasst wird. Zusätzlich wird ein Take-Profit gesetzt, um eine vorsichtige Risikosteuerung zu gewährleisten.

Vorteile

- Nutzt die starke Rückkehrneigung der Bollinger-Bänder zur Mittellinie, um mittel- bis langfristige Trends zu erfassen.

- Long- und Short-Signale sind klar und leicht umsetzbar.

- Dynamischer Gleit-Stop-Loss sichert Gewinne maximal und kontrolliert Risiken.

- Parameter können an die Marktbedingungen angepasst werden, um sich verschiedenen Marktlagen anzupassen.

Risiken und Lösungen

- In einer Seitwärtsbewegung (Ranging-Markt) können mehrfache Long- und Short-Signale auftreten, die zu Fehlsignalen führen. Lösung: Setzen Sie sinnvolle Stop-Loss-Grenzen, um Einzelverluste zu begrenzen.

- Eine ungünstige Parametereinstellung kann die Gewinnquote senken. Lösung: Optimieren Sie die Parameter entsprechend den verschiedenen Märkten.

Optimierungsmöglichkeiten

- Optimierung der Parameter des gleitenden Durchschnitts, um sie an die Eigenschaften des jeweiligen Instruments anzupassen.

- Integration eines Trendfilters, um Seitwärtsbewegungen zu vermeiden.

- Kombination mit anderen Indikatoren als Filterkriterien, um die Stabilität der Strategie zu erhöhen.

Zusammenfassung

Diese Strategie nutzt die Rückkehrneigung der Bollinger-Bänder in Kombination mit einem dynamischen Gleit-Stop-Loss, um unter kontrolliertem Risiko Gewinne aus mittel- bis langfristigen Trends zu erzielen. Es handelt sich um eine anpassungsfähige und stabile quantitative Strategie. Durch Parameteroptimierung und Regelanpassung kann sie an verschiedene Instrumente angepasst werden und im Live-Handel stabile Erträge erzielen.

/*backtest

start: 2024-01-24 00:00:00

end: 2024-01-31 00:00:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(shorttitle="BB Strategy", title="Bollinger Bands Strategy", overlay=true)

length = input.int(20, minval=1, group = "Bollinger Bands")

maType = input.string("SMA", "Basis MA Type", options = ["SMA", "EMA", "SMMA (RMA)", "WMA", "VWMA"], group = "Bollinger Bands")- 1