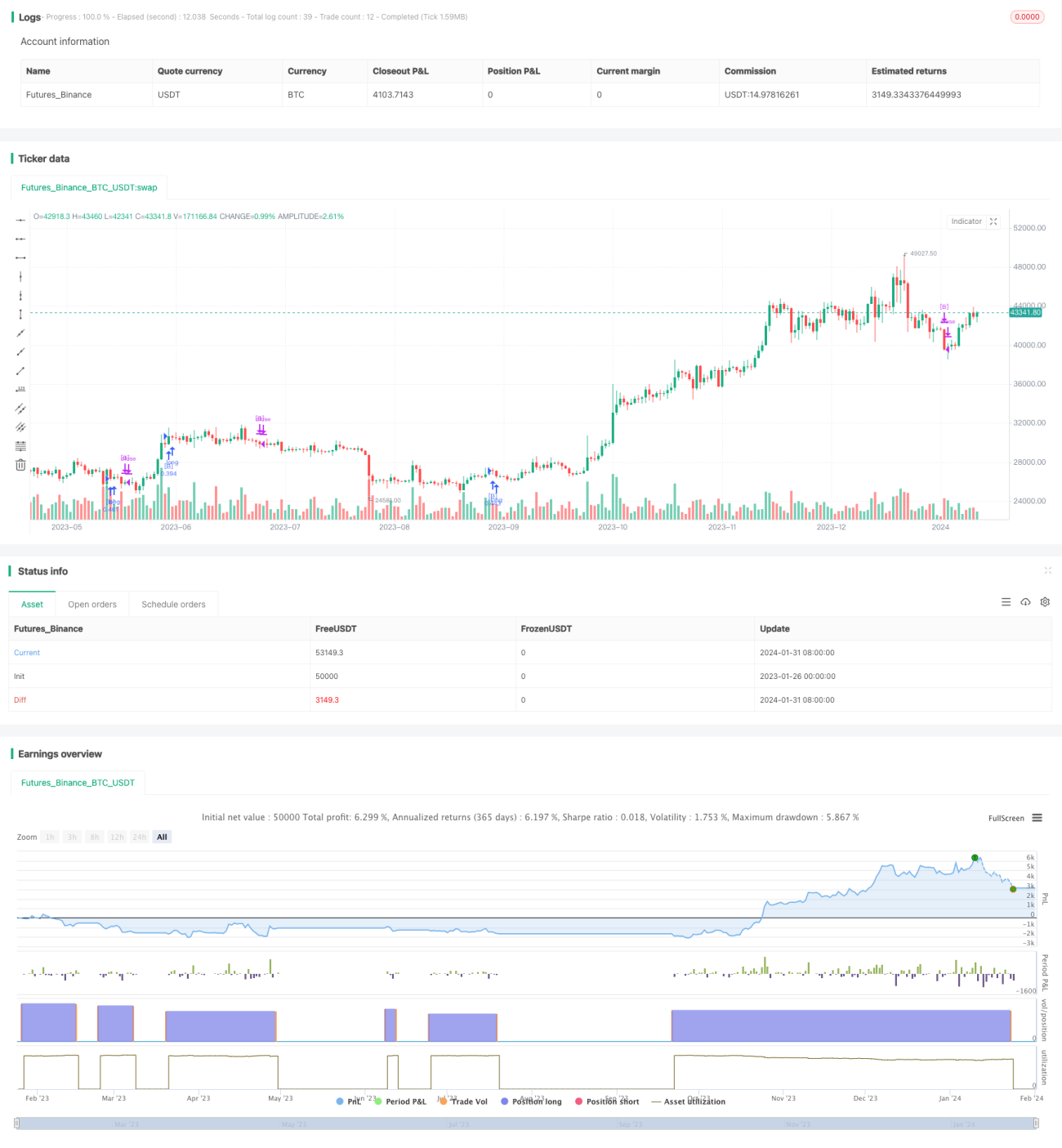

Langfristige Umkehrstrategie basierend auf zwei gleitenden Durchschnitten

Übersicht

Diese Strategie nutzt hauptsächlich die Goldenen Kreuze und Todeskreuze, die durch die einfachen gleitenden Durchschnitte der 14- und 28-Tage-Perioden gebildet werden, für Reverse-Operationen. Wenn die schnelle Linie von unten nach oben die langsame Linie durchbricht, deutet dies auf eine Trendumkehr hin, und es kann eine Long-Position eröffnet werden. Wenn die schnelle Linie von oben nach unten die langsame Linie durchbricht, deutet dies auf eine Trendumkehr hin, und es kann eine Short-Position eröffnet werden.

Aufgrund des Prinzips, dass sie einfache gleitende Durchschnitte zur Bestimmung von Markttrendänderungen nutzt, nenne ich diese Strategie „Langfristige Reversal-Strategie basierend auf zwei gleitenden Durchschnitten".

Strategieprinzip

Der Kernlogik dieser Strategie besteht darin, die einfachen gleitenden Durchschnitte der 14- und 28-Tage-Perioden zur Bestimmung des Markttrends zu nutzen. Die genauen Regeln sind wie folgt:

- Die schnelle Linie wird als 14-Tage einfacher gleitender Durchschnitt definiert, die langsame Linie als 28-Tage einfacher gleitender Durchschnitt.

- Wenn die schnelle Linie von unten nach oben die langsame Linie durchbricht, ist dies ein Long-Signal und es wird eine Long-Position eröffnet.

- Wenn die schnelle Linie von oben nach unten die langsame Linie durchbricht, ist dies ein Short-Signal und es wird eine Short-Position eröffnet.

- Nach Eröffnung einer Long/Short-Position, wenn die schnelle Linie erneut die langsame Linie nach unten durchbricht, ist dies ein Schließsignal.

Die Strategie kombiniert gleichzeitig Stop-Loss, Take-Profit und Trailing Take-Profit für das Risikomanagement. Für Long- und Short-Positionen werden jeweils der Long-Stop-Loss-Preis, der Long-Take-Profit-Preis, der Short-Take-Profit-Preis und der Long-Trailing-Take-Profit-Preis definiert. Diese Parameter werden in Prozentform festgelegt, was die Strategie flexibler macht.

Vorteile

- Die Strategie nutzt zwei gleitende Durchschnitte zur Bestimmung des Haupttrends des Marktes; das Prinzip ist einfach und klar, leicht zu verstehen und zu validieren.

- Die Perioden der schnellen und langsamen gleitenden Durchschnitte sind auf 14 und 28 Tage eingestellt, die jeweils kurzfristige und mittelfristige Trendwechsel darstellen, und ermöglichen eine gute Erkennung von Reversal-Chancen.

- Die Kombination von Take-Profit, Stop-Loss und Trailing Take-Profit kontrolliert das Risiko, sichert Gewinne und vermeidet Verlustausweitungen.

- Es können sowohl Long- als auch Short-Positionen eröffnet werden, um den Anforderungen verschiedener Marktumgebungen gerecht zu werden.

Risiken und Verbesserungen

- Der Crossover der zwei gleitenden Durchschnitte hat eine gewisse Verzögerung und könnte den besten Einstiegszeitpunkt verpassen.

- Der Crossover von langer und kurzer gleitender Durchschnitt neigt zu Fehlsignalen; zu kurze Perioden der gleitenden Durchschnitte sollten vermieden werden.

- Ein zu geringer Stop-Loss-Abstand kann die Wahrscheinlichkeit eines Auslösens durch Marktschwankungen erhöhen. Der Stop-Loss-Abstand sollte je nach Instrument angemessen festgelegt werden.

- Es können weitere Indikatoren zur Kombination hinzugefügt werden, um die Robustheit der Strategie zu erhöhen. Beispielsweise könnte man Bollinger-Bänder zur Trendbestimmung oder den MACD zur Überprüfung des Einstiegszeitpunkts einbeziehen.

Optimierungsrichtungen

- Testen verschiedener Parameterkombinationen der gleitenden Durchschnitte, um die für die Eigenschaften des Instruments am besten geeigneten Perioden zu finden.

- Testen verschiedener Stop-Loss-Abstandseinstellungen, um die optimale Stop-Loss-Position zu finden.

- Testen der Hinzunahme anderer Indikatoren zur Optimierung, um die optimale Parameterkombination zur Reduzierung von Fehlsignalen zu finden.

- Optimierung der Positionsmanagementregeln, um Gewinne zu maximieren.

Zusammenfassung

Insgesamt handelt es sich bei dieser Strategie um eine sehr klassische Strategie, die auf der Bestimmung von Trendumkehrungen mittels zwei gleitender Durchschnitte basiert. Sie hat die Vorteile eines einfachen Handelsprinzips und ist leicht zu erlernen; gleichzeitig gibt es einige Richtungen, die später kontinuierlich optimiert werden können. Insgesamt ist die Strategie sowohl in der Theorie als auch in der Praxis recht ausgereift und eine gute Einstiegsstrategie für den quantitativen Handel.

- 1