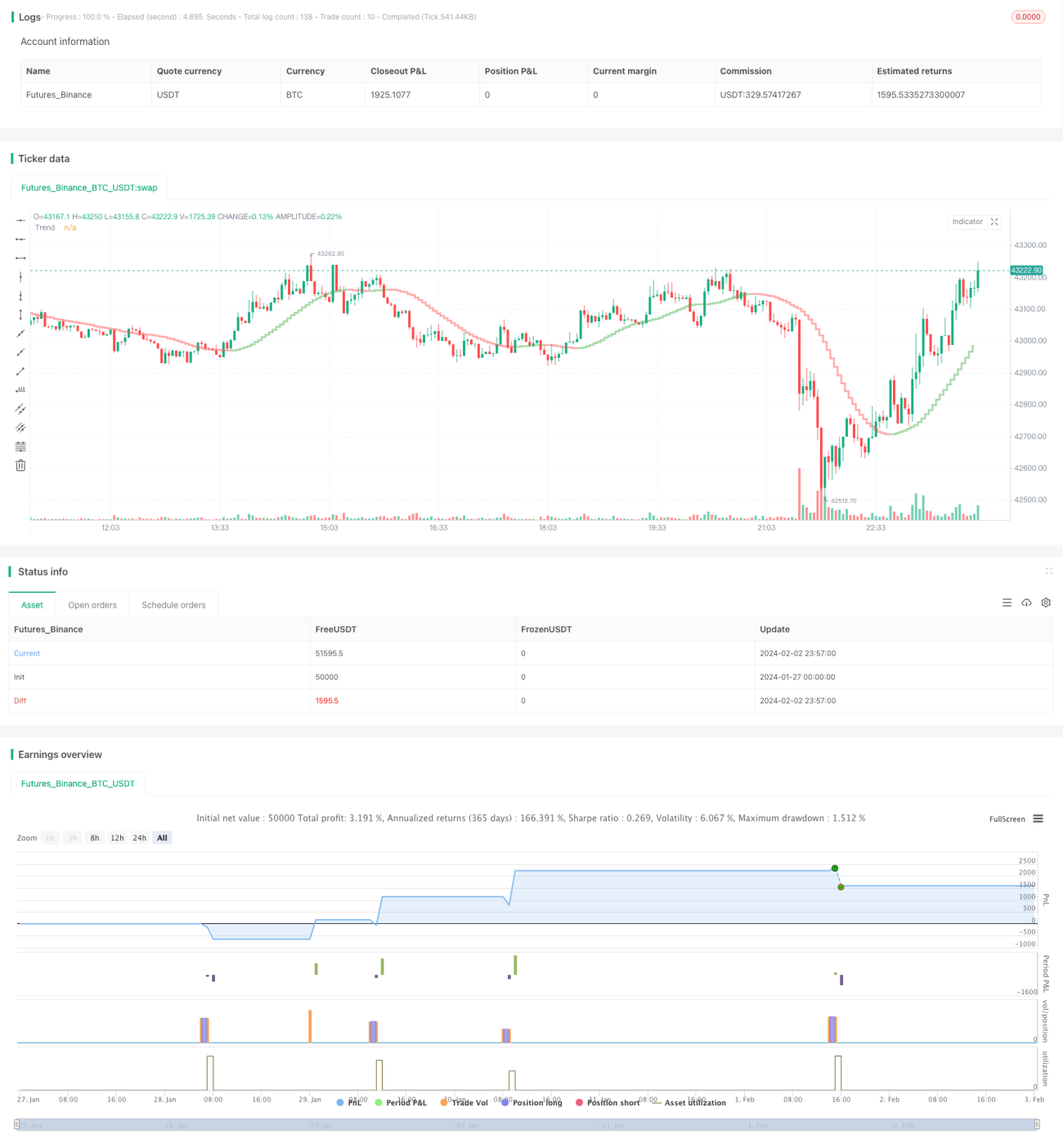

Ripple-Strategie basierend auf dem Coral Trend-Indikator im Backtest-Zeitraum

Übersicht

Diese Strategie nutzt den Coral Trend Indikator von LazyBear, um die Preistrendrichtung zu bestimmen. Durch die Erkennung von Umkehrungen der Coral Trend Indikatorrichtung werden potenzielle Einstiegspunkte identifiziert. Um Fehldurchbrüche zu filtern, wird eine Kombination aus dem ADX-Indikator oder dem Absolute Strength Histogram und dem HawkEye Volume Indikator als Bestätigungsindikator verwendet, um zuverlässigere Einstiege zu ermöglichen.

Der Ausstiegsmechanismus verwendet den höchsten/niedrigsten Preis der letzten N Kerzen multipliziert mit einem konfigurierbaren Risiko-Ertrags-Verhältnis, um Stop-Loss- und Take-Profit-Niveaus festzulegen.

Strategieprinzip

Nach der Bestimmung der Haupttrendrichtung auf Basis des Coral Trend Indikators tritt ein kleiner Pullback in die entgegengesetzte Richtung auf, während die Farbe des Indikators unverändert bleibt. Wenn das Pullback endet und der Preis wieder in die vom Coral Trend angezeigte Haupttrendrichtung zurückkehrt, kann dies als ein guter Einstiegszeitpunkt angesehen werden.

Die Einstiegsbedingungen umfassen:

-

Die Coral Trend Indikatorrichtung stimmt mit der Handelsrichtung überein (long = grün, short = rot).

-

Seit dem letzten vollständigen Durchbruch des Preises durch den Coral Trend (das Hoch des letzten Balkens liegt vollständig über der Coral Trend-Linie) gab es mindestens eine Kerze, deren Tiefstände vollständig über dem Coral Trend (long) bzw. deren Hochstände vollständig unter dem Coral Trend (short) liegen.

-

Es tritt ein kleiner Pullback in die entgegengesetzte Richtung auf; während dieses Pullbacks bleibt der Schlusskurs stets auf der gegenüberliegenden Seite des Coral Trends.

-

Nach dem Ende des kleinen Pullbacks kehrt der Schlusskurs wieder in die vom Coral Trend angezeigte Haupttrendrichtung zurück.

Die obigen Bedingungen sind die Hauptbedingungen. Gleichzeitig werden der ADX-Indikator oder eine Kombination aus Absolute Strength Histogram und HawkEye Volume als Bestätigungsbedingung für den Einstieg verwendet.

Der ADX-Indikator erfordert einen Wert > 20 und einen Anstieg der letzten Kerze. Außerdem muss die Reihenfolge der grünen und roten DI-Linien mit der Handelsrichtung übereinstimmen.

Absolute Strength Histogram erfordert, dass seine Farbe mit der Handelsrichtung übereinstimmt (long = blau, short = rot). HawkEye Volume erfordert, dass seine Farbe mit der Handelsrichtung übereinstimmt (long = grün, short = rot).

Der Ausstiegsmechanismus verwendet den höchsten oder niedrigsten Preis der letzten N Kerzen multipliziert mit dem Risiko-Ertrags-Verhältnis, um Stop-Loss und Take-Profit zu setzen. Der N-Wert und das Risiko-Ertrags-Verhältnis sind über Parameter konfigurierbar.

Vorteilsanalyse

Der größte Vorteil dieser Strategie liegt darin, dass sie nach der Bestimmung der Haupttrendrichtung mit dem Coral Trend Indikator durch Erkennung seiner Umkehr Einstiegsmöglichkeiten findet, sodass sie nicht in trendlosen Märkten mitschwimmt. Gleichzeitig können durch den Einsatz von Bestätigungsindikatoren viele Fehldurchbrüche gefiltert werden, was die Erfolgsquote der Einstiege erhöht.

Darüber hinaus bietet die Strategie einen vollständigen Risikokontrollmechanismus, einschließlich der Einstellung von Stop-Loss-Spannen und der prozentualen Begrenzung des Risiko-Exposures, sodass selbst einzelne Verlusttrades das Gesamtkapital nicht wesentlich beeinträchtigen.

Risikoanalyse

Das größte Risiko dieser Strategie besteht darin, dass die Einstiegsentscheidung auf Indikatoren basiert, was zu der Illusion führen kann, dass man sich vollständig auf Parameterkonfigurationen verlassen kann, um automatisch Gewinne zu erzielen. Tatsächlich erfordern Parameteroptimierung und Regelkonfiguration ein Verständnis der zugrunde liegenden Preisbewegungsgesetze und eine intuitive Beurteilung der Wechselwirkung zwischen Indikator und Preis, um eine Konfiguration zu finden, die besser zum eigenen Handelsstil und den gehandelten Instrumenten passt.

Darüber hinaus müssen Stop-Loss- und Take-Profit-Niveaus angemessen eingestellt werden. Ein zu hohes Take-Profit-Verhältnis kann dazu führen, dass ein Ausstieg nicht erreicht wird, während ein zu enger Stop-Loss ein zu hohes Risiko darstellt. Dies muss je nach Volatilität des Instruments und der persönlichen Risikotoleranz eingestellt werden.

Optimierungsmöglichkeiten

Zu den Optimierungsmöglichkeiten dieser Strategie gehören:

-

Anpassung der Parameter des Coral Trend Indikators, um seine Reaktion auf Preisänderungen verschiedener Instrumente zu verbessern.

-

Ausprobieren verschiedener Bestätigungsindikatoren oder Indikatorkombinationen wie KDJ, MACD usw., um die Einstiegssignale genauer zu machen.

-

Anpassung der Berechnungsmethode für Stop-Loss und Take-Profit basierend auf der Volatilität verschiedener Instrumente, um eine bessere Risikokontrolle zu erreichen.

-

Hinzufügen eines Geldmanagementmoduls, das die Auftragsgröße basierend auf der Positionsgröße anpasst, um Gesamtverluste effektiv zu begrenzen.

-

Hinzufügen eines Handelszeitkontrollmoduls, sodass die Strategie nur zu bestimmten Zeiten läuft, um Verluste in stark volatilen Phasen zu vermeiden.

Zusammenfassung

Diese Strategie nutzt zunächst den Coral Trend Indikator, um den mittel- bis langfristigen Preistrend zu bestimmen, und erkennt dann dessen Umkehr. In Kombination mit Bestätigungssignalen zur Filterung von Fehldurchbrüchen wird eine relativ zuverlässige Trendfolgestrategie entwickelt. Gleichzeitig ermöglicht die umfassende Risikokontrolle einen langfristigen Betrieb mit stabilem Kapital. Durch weitere Optimierung von Parametern und Modulen kann die Strategie voraussichtlich an eine größere Anzahl von Instrumenten angepasst werden und eine bessere Stabilität und Rentabilität aufweisen.

- 1