Eine auf dem Hull-Indikator und dem LSMA-Indikator basierende Trendfolge-Quantitativstrategie.

Übersicht

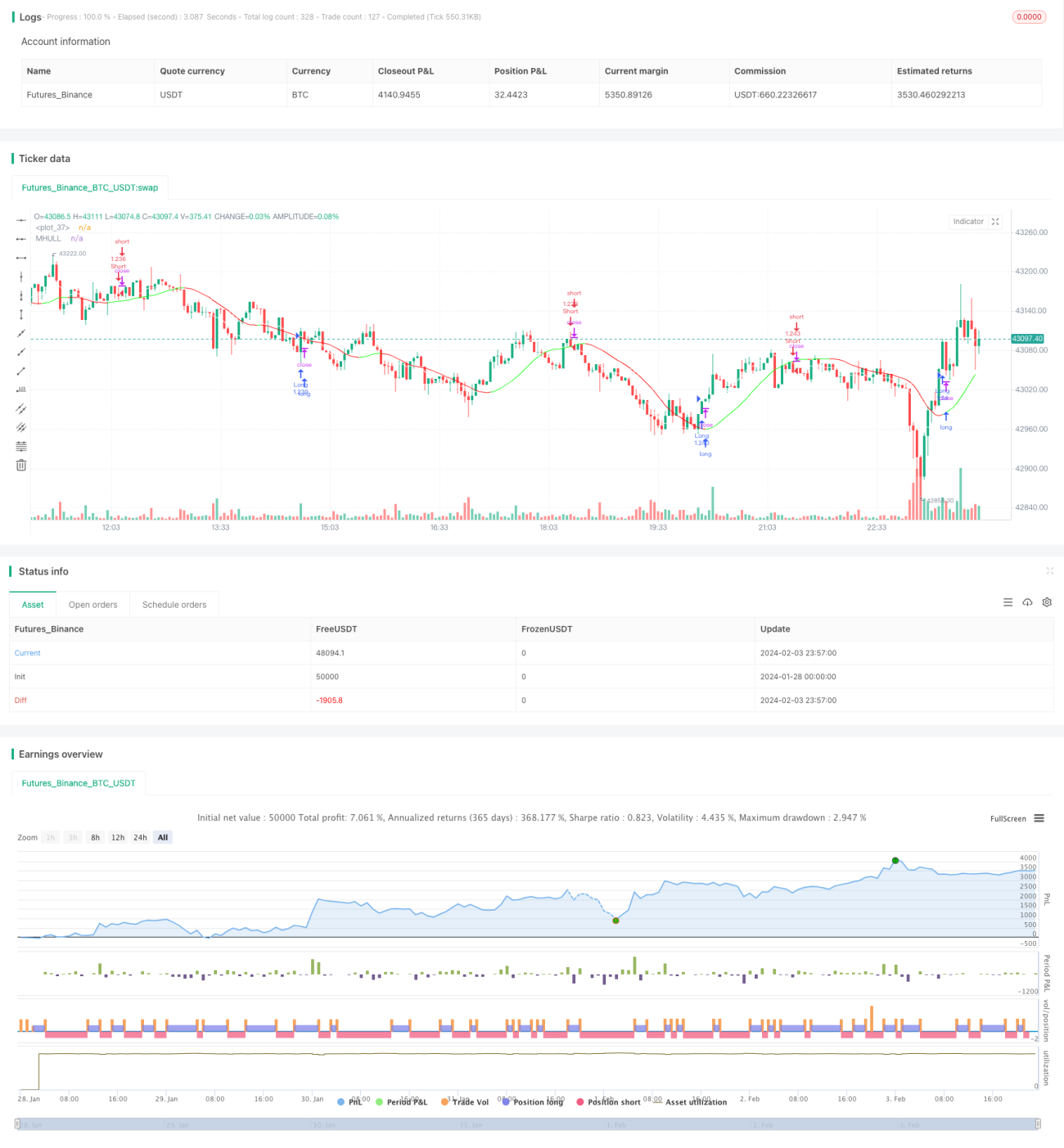

Die Strategie kombiniert den Hull-Indikator und den LSMA (Least Squares Moving Average), um Trendrichtung und Trendwenden zu identifizieren und den Trend zu verfolgen. Wenn der Hull-Indikator einen Aufwärtstrend anzeigt und der LSMA den Hull-Indikator nach oben kreuzt, wird eine Long-Position eröffnet; wenn der Hull-Indikator einen Abwärtstrend anzeigt und der LSMA den Hull-Indikator nach unten kreuzt, wird eine Short-Position eröffnet. Die Strategie eignet sich für den mittel- bis niederfrequenten Handel und kann im 1-Minuten-Zeitrahmen eingesetzt werden.

Strategieprinzip

-

Der Hull-Indikator dient zur Bestimmung der Trendrichtung des Werts. Wenn die mittlere Linie (MHULL) über der unteren Linie (LHULL) liegt, zeigt dies einen Aufwärtstrend an; im umgekehrten Fall einen Abwärtstrend.

-

Der LSMA-Indikator wird verwendet, um Trendwendepunkte zu erkennen. Wenn der LSMA die MHULL nach oben kreuzt, deutet dies auf die Bildung oder Beschleunigung eines Aufwärtstrends hin; kreuzt der LSMA die MHULL nach unten, deutet dies auf die Bildung oder Beschleunigung eines Abwärtstrends hin.

-

Kombination beider: Wenn der Hull-Indikator einen Aufwärtstrend anzeigt (MHULL > LHULL) und der LSMA die MHULL nach oben kreuzt, wird eine Long-Position eröffnet. Wenn der Hull-Indikator einen Abwärtstrend anzeigt (MHULL < LHULL) und der LSMA die MHULL nach unten kreuzt, wird eine Short-Position eröffnet.

-

Der Stop-Loss wird auf den letzten Schwankungspunkt gesetzt. Der Stop-Loss für Long-Positionen ist das jüngste Tief, der Stop-Loss für Short-Positionen das jüngste Hoch.

Vorteile

Die Strategie bietet folgende Vorteile:

-

Der Hull-Indikator reagiert schnell und erfasst Trendwechsel rechtzeitig; der LSMA ist glättend und erkennt Umkehrsignale zuverlässig. Die Kombination beider liefert gute Ergebnisse.

-

Durch die Kreuzung des LSMA werden Fehlsignale des Hull-Indikators gefiltert, wodurch die Wahrscheinlichkeit von Fehltrades reduziert wird.

-

Die Verwendung von Schwankungspunkten als Stop-Loss schützt das Kapital bestmöglich.

-

Geeignet für den mittel- bis niederfrequenten Handel und kann im 1-Minuten- oder sogar niedrigeren Zeitrahmen eingesetzt werden – breite Anwendbarkeit.

Risikoanalyse

Die Strategie birgt auch einige Risiken:

-

In Seitwärtsmärkten können Hull-Indikator und LSMA mehrfach kreuzen, was zu übermäßig vielen Trades führt. Die Parameter sollten angepasst werden, um die Handelsfrequenz zu senken.

-

Der auf Schwankungspunkten basierende Stop-Loss könnte durch kurzfristige Kursanpassungen ausgelöst werden; der Abstand der Stop-Loss-Positionen sollte daher etwas vergrößert werden.

-

Aufgrund der Verzögerung des LSMA-Indikators besteht ein geringes Risiko von Fehleinschätzungen. Dies sollte durch die Kombination mit anderen Indikatoren wie Kerzenformationen bestätigt werden.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen optimiert werden:

-

Optimierung der Parameter von Hull-Indikator und LSMA, um die Kombination besser an verschiedene Instrumente und Zeitrahmen anzupassen.

-

Hinzufügen von Filtern basierend auf Volatilität, Handelsvolumen usw., um Fehltrades in Seitwärtsmärkten zu vermeiden.

-

Integration von Machine-Learning-Algorithmen zur unterstützenden Beurteilung der Trendneigung.

-

Einsatz von Deep-Learning-Techniken zur Bestimmung wichtiger Unterstützungs- und Widerstandszonen, um den Stop-Loss sinnvoller zu gestalten.

Zusammenfassung

Die Strategie nutzt die Kombination aus Hull-Indikator und LSMA, um Trendrichtungsänderungen zu beurteilen und Trendfolgegeschäfte durchzuführen. Zu den Vorteilen zählen die einfache Handhabung, die schnelle Reaktion und die breite Anwendbarkeit im mittel- bis niederfrequenten quantitativen Handel. Durch weitere Optimierung der Filter, der unterstützenden Beurteilung und der Stop-Loss-Algorithmen können voraussichtlich bessere Strategieergebnisse erzielt werden.

- 1