Quantitative Handelsstrategie basierend auf mehreren Faktoren

Übersicht

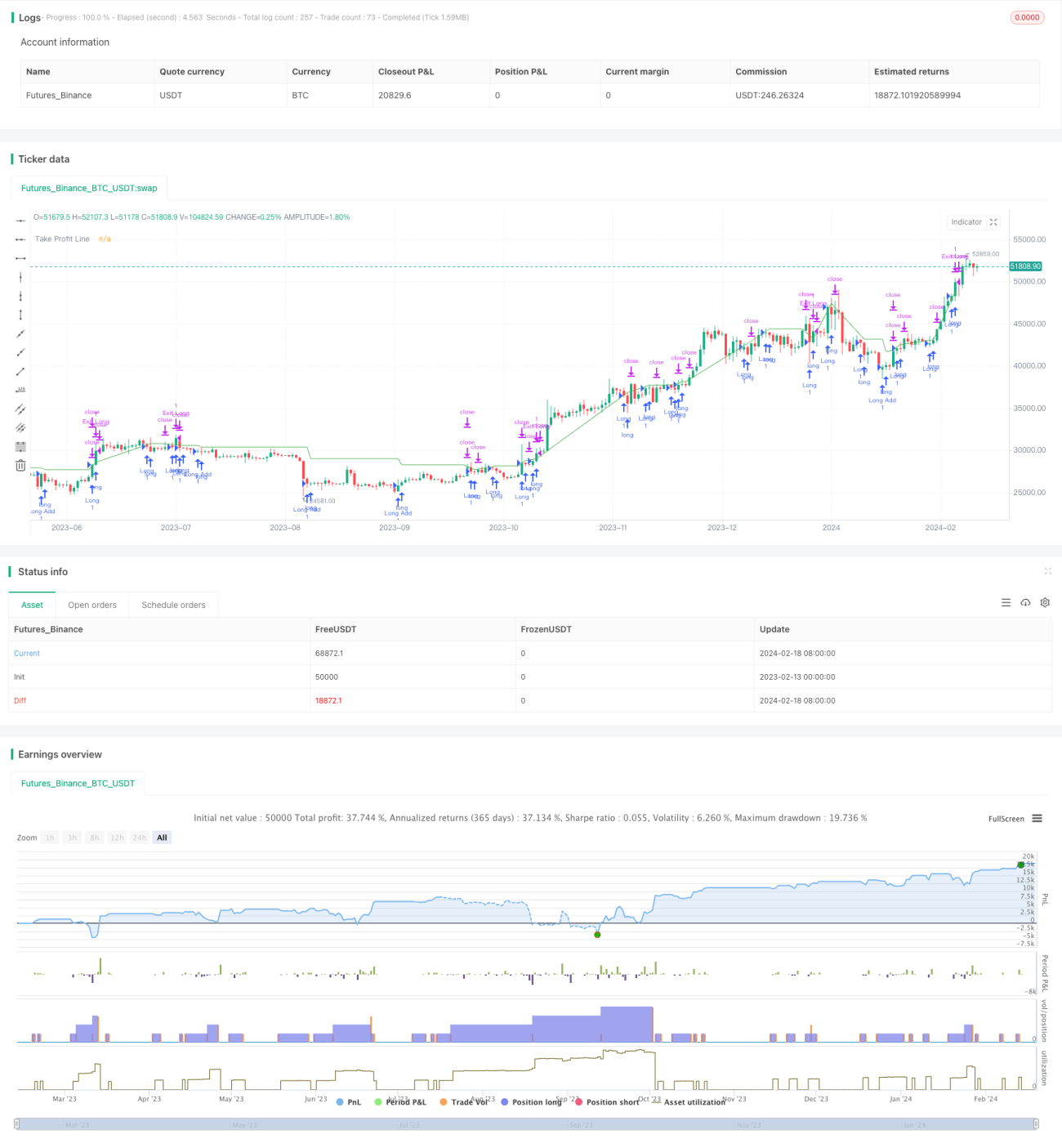

Diese Strategie kombiniert mehrere technische Indikatoren wie RSI, MACD, OBV, CCI, CMF, MFI und VWMACD, um Divergenzen zwischen Preis und Volumen zu erkennen und potenzielle Einstiegspunkte zu identifizieren. Gleichzeitig wird ein benutzerdefinierter Dip-Erkennungsindikator eingesetzt, der Handelssignale auslöst, wenn hohe Volatilität sowie tiefe oder VFI-Bedingungen erfüllt sind. Die Strategie geht nur Long, baut Positionen schrittweise auf und verwendet einen Trailing-Stop.

Strategieprinzip

-

Berechnung der Indikatoren RSI, MACD, OBV, CCI, CMF, MFI und VWMACD. Mittels adaptiver linearer Regression werden Divergenzen zwischen den Indikatoren und dem historischen Preis erkannt. Wenn ein Indikator ein neues Tief erreicht, der Preis jedoch nicht entsprechend fällt, wird ein Kaufsignal generiert.

-

Basierend auf benutzerdefinierten Schwellenwerten für Volatilität und Tiefenprozentsatz sowie einer VFI-Filterung werden Signale auf Kerzen ausgegeben, die hohe Volatilität und Tiefentests erfüllen.

-

Nach dem initialen Long-Einstieg wird die Position erneut aufgestockt, wenn der Preis um einen bestimmten (konfigurierbaren) Prozentsatz unter den letzten Long-Einstiegspreis fällt.

-

Verwendung eines Trailing-Stops: Bei Erreichen des konfigurierten Gewinnziels wird die Position geschlossen.

Vorteile

-

Multi-Faktor-Kombination aus Preis- und Volumenindikatoren erhöht die Zuverlässigkeit der Signale.

-

Die adaptive lineare Regression zur Divergenzerkennung vermeidet subjektive menschliche Einschätzungen.

-

Die Kombination von Volatilität und Tiefen-/VFI-Indikatoren hilft, Umkehrchancen zu identifizieren.

-

Mehrfaches Nachkaufen während Preiskorrekturen und der Trailing-Stop begünstigen die Gewinnsicherung.

Risikoanalyse

-

Die komplexe Multi-Faktor-Beurteilung kann durch Parameteroptimierung und Divergenzerkennung die tatsächliche Performance beeinflussen.

-

Hohes Risiko durch einseitige Long-Positionen – bei Fehleinschätzungen können erhebliche Verluste entstehen.

-

Der wiederholte Nachkauf vergrößert mögliche Verluste, daher ist eine vorsichtige Positionskontrolle erforderlich.

-

Die Auswirkungen von Transaktionskosten auf die tatsächliche Rentabilität müssen berücksichtigt werden.

Optimierungsmöglichkeiten

-

Testen verschiedener Parameterkombinationen und Indikatorvarianten zur Auswahl der optimalen Konfiguration.

-

Hinzufügen einer Stop-Loss-Strategie zur Begrenzung von Einzel- und Maximalverlusten.

-

Berücksichtigung von Handelssignalen in beide Richtungen zur Risikostreuung.

-

Einsatz von maschinellen Lernmethoden zur automatischen Parameteroptimierung.

Zusammenfassung

Diese Strategie nutzt mehrere technische Indikatoren zur Identifizierung von Einstiegszeitpunkten, während benutzerdefinierte Bedingungen und der VFI-Indikator als Filter gegen Fehlsignale dienen. Durch wiederholtes Nachkaufen bei Preiskorrekturen wird die Teilnahme an Trendbewegungen begünstigt. Allerdings besteht das Risiko von Fehleinschätzungen und einseitigen Positionen. Eine angemessene Optimierung der Indikatorparameter und Stop-Loss-Strategien ist erforderlich, um Risiken zu reduzieren und das Gewinnpotenzial zu steigern.

- 1