Basierend auf einer dualen Reversal-Momentum-Strategie

Überblick

Die Double-Reversal-Momentum-Strategie kombiniert Preisumkehrsignale mit Volatilitätsumkehrsignalen, um Trendhandel zu realisieren. Sie basiert hauptsächlich auf der 123-Formation zur Erkennung von Preisumkehrpunkten und nutzt ergänzend die Donchian-Kanal-Volatilität zur Filterung falscher Signale. Die Strategie eignet sich für mittel- bis langfristige Positionen und kann durch die doppelte Umkehrfilterung Marktwendepunkte effektiv erfassen und Überrenditen erzielen.

Strategieprinzip

Der Preisumkehrteil verwendet die 123-Formation zur Bewertung. Diese Formation bedeutet, dass die Preise der ersten beiden Kerzen eine Gegenbewegung (Anstieg oder Rückgang) zeigen, während die dritte Kerze wieder umkehrt (Rückgang oder Anstieg) – daher der Name 123-Formation. Wenn eine solche Drei-Kerzen-Umkehr auftritt, deutet dies in der Regel auf eine bevorstehende Trendwende hin. Um die Zuverlässigkeit der Preisumkehr weiter zu bestätigen, verwendet die Strategie auch den Stochastic-Indikator. Ein Handelssignal wird nur ausgelöst, wenn auch der Stochastic eine Umkehr zeigt (schnelle Linie fällt oder steigt schnell an).

Der Volatilitätsumkehrteil nutzt die Donchian-Kanal-Volatilität. Der Donchian-Kanal spiegelt hauptsächlich die Preisschwankungsbreite wider. Wenn die Preisvolatilität zunimmt, weitet sich die Donchian-Kanalbreite aus; wenn die Volatilität abnimmt, verengt sich die Kanalsbreite. Die Donchian-Kanal-Volatilität (Breite) kann effektiv das Marktvolatilitätsniveau und das Risiko messen. Die Strategie verwendet die Umkehr der Donchian-Kanal-Volatilität, um falsche Signale zu filtern. Ein Handelssignal wird nur ausgegeben, wenn sich sowohl die Volatilität als auch der Preis umkehren, wodurch verhindert wird, dass man in seitwärts gerichteten Bewegungen gefangen wird.

Zusammenfassend gewährleistet die Strategie durch die doppelte Umkehrüberprüfung sowohl die Zuverlässigkeit der Handelssignale als auch die Risikokontrolle und ist eine relativ robuste Trendstrategie.

Strategievorteile

- Doppelter Filtermechanismus, der die Zuverlässigkeit von Handelssignalen sicherstellt und falsche Ausbrüche vermeidet

- Risikokontrolle, die die Wahrscheinlichkeit von Verlusten verringert

- Geeignet für mittel- bis langfristige Positionen, um Marktrauschen zu vermeiden und Überrenditen zu erzielen

- Großer Optimierungsspielraum für Parameter, um einen optimalen Zustand zu erreichen

- Einzigartiger Stil, der in Kombination mit gängigen technischen Indikatoren gute Ergebnisse liefert

Strategierisiken

- Abhängigkeit von Parameteroptimierung; falsche Parameter beeinträchtigen die Strategieleistung

- Die Stop-Loss-Strategie muss weiter verbessert werden, der maximale Drawdown ist noch optimierbar

- Die Handelsfrequenz kann niedrig sein, was für hochfrequente algorithmische Strategien ungeeignet ist

- Erfordert die Auswahl geeigneter Instrumente und Zeitrahmen; der Anwendungsbereich ist begrenzt

- Optimale Parameter könnten durch maschinelles Lernen usw. gefunden werden

Optimierungsrichtungen

- Hinzufügen eines adaptiven Stop-Loss-Moduls kann den maximalen Drawdown erheblich reduzieren

- Einbeziehung von Volumenindikatoren, um den Einstieg bei hohem Volumenausbruch sicherzustellen

- Optimierung der Parameter für beste Stabilität

- Testen verschiedener Instrumente und Zeitrahmen, um die optimale Umgebung zu finden

- Kombination mit anderen Indikatoren oder Strategien, um Synergieeffekte von 1+1 > 2 zu erzielen

Zusammenfassung

Die Double-Reversal-Momentum-Strategie erreicht durch die doppelte Überprüfung von Preisumkehr und Volatilitätsumkehr eine gute Risikokontrolle. Im Vergleich zu einzelnen Indikatoren filtert sie viel Rauschen heraus und bietet eine bessere Stabilität. Durch Parameteroptimierung, Verbesserung des Stop-Loss-Moduls und Einbeziehung von Volumen kann die Strategie die Signalqualität und Ertragsstabilität weiter steigern. Sie eignet sich als Bestandteil mittel- bis langfristiger Strategien für Aktien, Kryptowährungen usw. und kann in sinnvoller Kombination mit anderen Modulen gute Überrenditen erzielen.

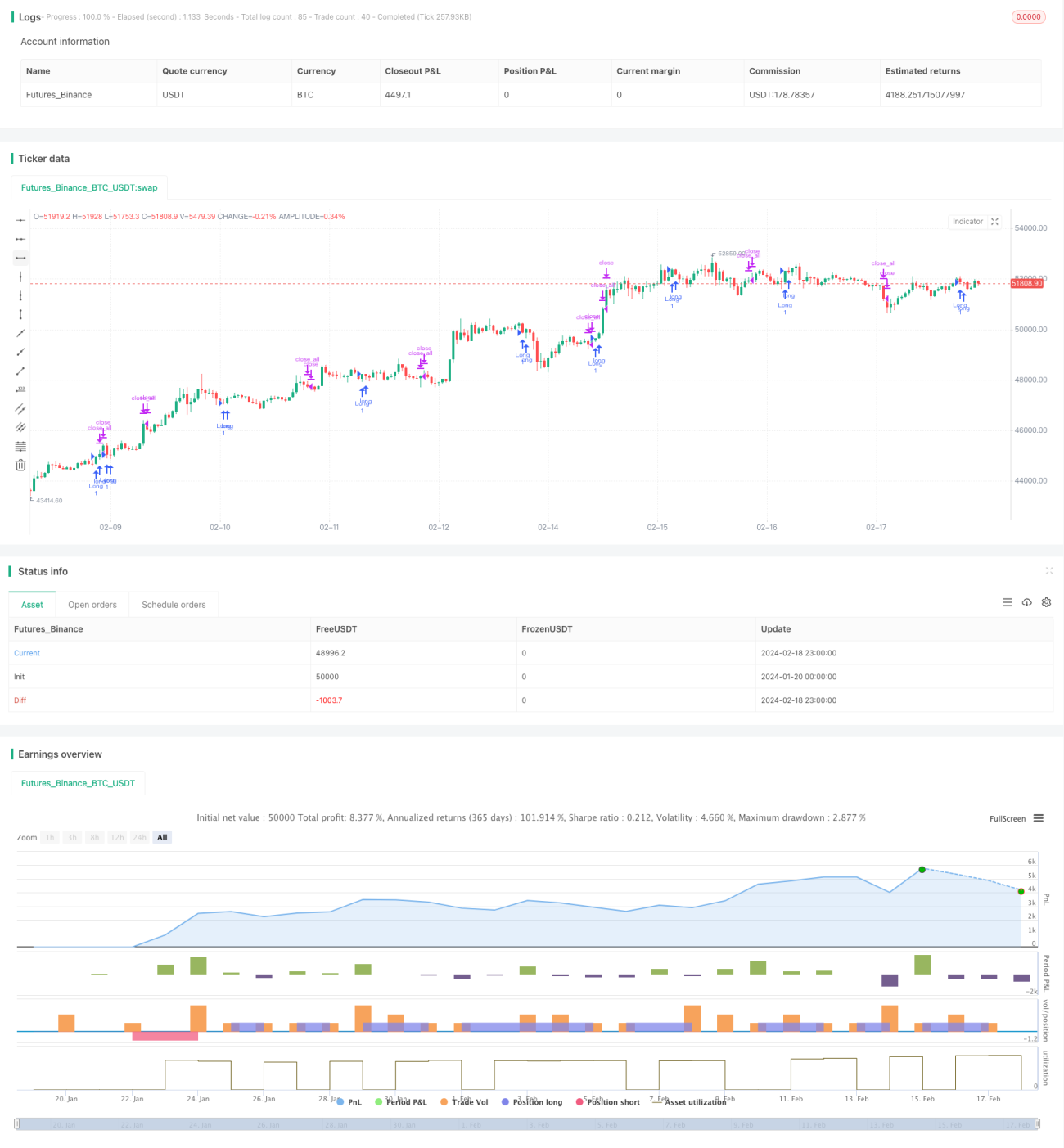

/*backtest

start: 2024-01-20 00:00:00

end: 2024-02-19 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 06/03/2020

// This is combo strategies for get a cumulative signal. - 1