Quantitative Trading-Strategie mit mehreren technischen Indikatoren

Überblick

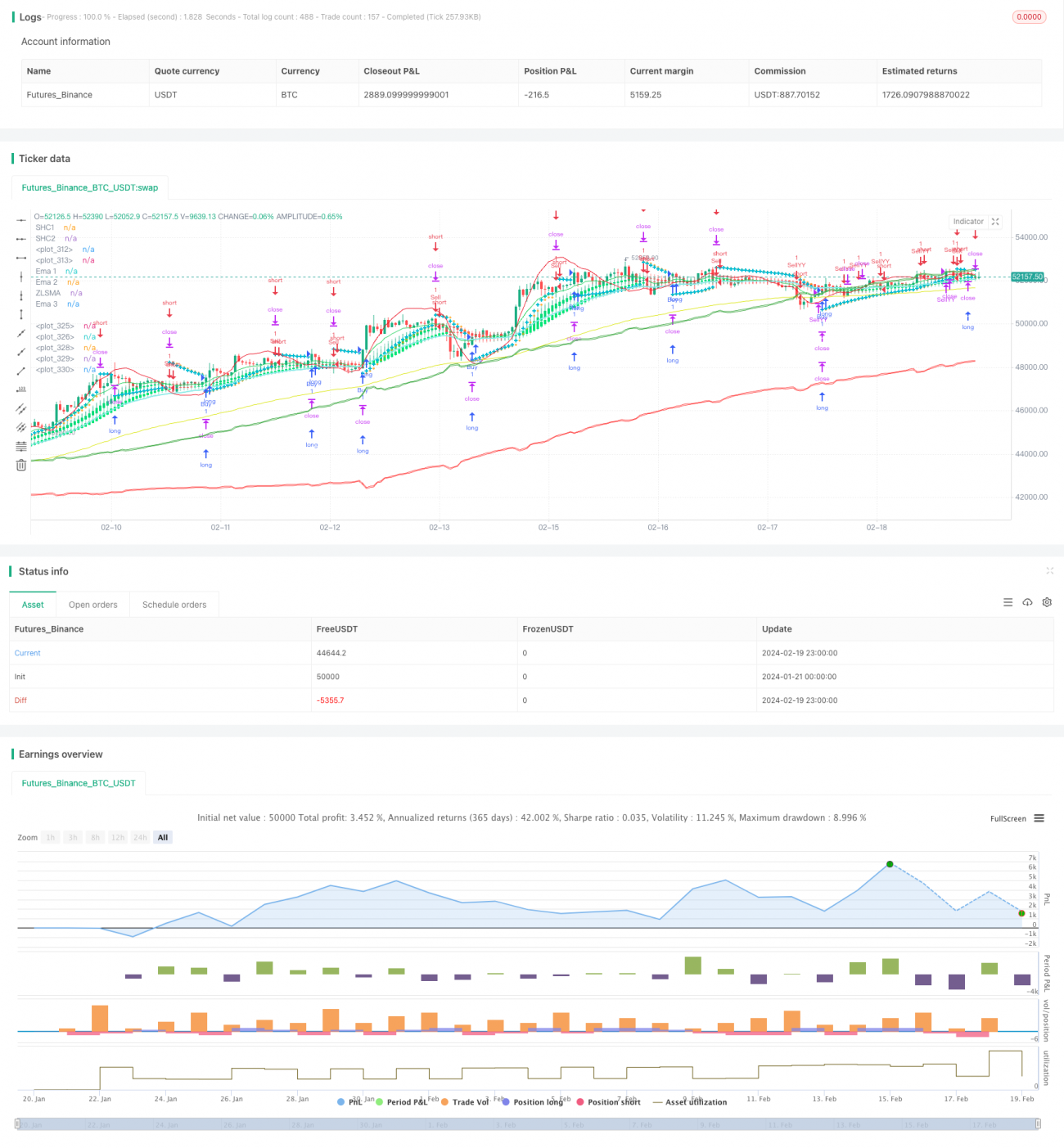

Diese Strategie nutzt eine Kombination mehrerer technischer Indikatoren, darunter das Parabolic-SAR-System, die Chanlun-Exit-Strategie, den gleitenden Durchschnitt mit Nullverzögerung, den exponentiellen gleitenden Durchschnitt sowie den geglätteten gleitenden Durchschnitt, um potenzielle Kauf- und Verkaufspunkte im Chart zu identifizieren.

Strategieprinzip

Hauptindikatoren

- Parabolic-SAR-System: Dient zur Bestimmung von Stop-Loss-Punkten und potenziellen Einstiegspunkten.

- Chanlun-Exit-Strategie: Wird zur Bestimmung der Trendrichtung verwendet.

- Gleitender Durchschnitt mit Nullverzögerung: Bietet einen gleitenden Durchschnitt mit geringer Verzögerung.

- Exponentieller gleitender Durchschnitt: Verfolgt Preis-Trends und -Volatilität.

- Geglätteter gleitender Durchschnitt: Erzeugt einen gleichmäßigeren gleitenden Durchschnitt.

Handelssignale

- Gehe long, wenn das Parabolic-SAR-System einen Aufwärtstrend anzeigt und der Preis über dem 99. exponentiellen gleitenden Durchschnitt liegt; gehe short, wenn ein Abwärtstrend angezeigt wird und der Preis unter dem 99. exponentiellen gleitenden Durchschnitt liegt.

- Bestätige die Trendrichtung durch Signale der Chanlun-Exit-Strategie.

- Der geglättete gleitende Durchschnitt arbeitet mit den Parabolic-Signalen zusammen, um Fehlausbrüche zu vermeiden.

Risikomanagement

- Setze Stop-Loss und Take-Profit fest.

- Berücksichtige die Bedingungen für den Kaufwiederaufnahmemechanismus, um die Positionen flexibel anzupassen.

Vorteile

Der größte Vorteil dieser Strategie liegt in der umfassenden Kombination von Indikatoren, die eine effektive Identifizierung der Trendrichtung ermöglicht. Das Parabolic-System bestimmt potenzielle Umkehrpunkte; die Chanlun-Exit-Strategie beurteilt den Haupttrend; die gleitenden Durchschnitte filtern Fehlsignale heraus. Die gegenseitige Bestätigung durch mehrere Indikatoren erhöht die Signalgenauigkeit erheblich.

Darüber hinaus sind Stop-Loss und Take-Profit in die Strategie integriert, um Risiken zu kontrollieren. Der geglättete gleitende Durchschnitt hilft zudem, Störungen durch kurzfristiges Rauschen zu vermeiden. All dies verleiht der Strategie eine hohe Stabilität.

Risikoanalyse

Da die Strategie auf einer Vielzahl von Indikatoren basiert, kann es zu Schwierigkeiten kommen, wenn diese widersprüchliche Signale liefern. Zudem können falsch eingestellte Parameter die Handelsergebnisse negativ beeinflussen.

Außerdem birgt der rein technische Handel inhärente Risiken, sodass Verluste nicht vollständig vermieden werden können. Eine vorsichtige Vorgehensweise ist erforderlich, blindes Folgen sollte vermieden werden.

Optimierungsmöglichkeiten

- Testen und optimieren Sie die Indikatorparameter, um die beste Kombination zu finden.

- Integrieren Sie Algorithmen des maschinellen Lernens, um mit großen Datenmengen Modelle zu trainieren und die Signalgenauigkeit weiter zu verbessern.

- Beziehen Sie Stimmungsindikatoren und Nachrichteninformationen ein, um die Marktbedingungen zu beurteilen und Positionen sowie Stop-Loss-Linien dynamisch anzupassen.

- Optimieren Sie die Logik der Kauf-Wiederaufnahme-Bedingungen, um die Signalerfassung flexibler und kontinuierlicher zu gestalten.

Zusammenfassung

Diese Strategie integriert mehrere technische Indikatoren und identifiziert Handelssignale durch deren Kombination. Ihre Stärken liegen in der hohen Signalgenauigkeit und der stabilen Performance. Gleichzeitig sind die Risikomanagementmaßnahmen angemessen. Insgesamt handelt es sich um einen bedenkenswerten Handelsansatz. Durch Parameteroptimierung, Modelltraining und die Einführung von Stimmungsindikatoren kann die Strategie weiter verbessert werden.

- 1