DEMA-Kreuz-Trendfolge-Strategie

Überblick

Die Strategie basiert auf dem Crossover der Double Exponential Moving Averages (DEMA) als Handelssignal und folgt dem Trend. Sie setzt Stop-Loss und Take-Profit automatisch. Ihre Vorteile sind klare Handelssignale, flexible Stop-Loss- und Take-Profit-Einstellungen und eine effektive Risikokontrolle.

Strategieprinzip

-

Berechnung der schnellen DEMA (8 Tage), der langsamen DEMA (24 Tage) und der Hilfs-DEMA (konfigurierbar).

-

Wenn die schnelle Linie die langsame Linie von unten nach oben kreuzt (Golden Cross), wird eine Long-Position eröffnet; kreuzt die schnelle Linie die langsame Linie von oben nach unten (Death Cross), wird eine Short-Position eröffnet.

-

Hinzufügen eines Filters: Ein Signal wird nur generiert, wenn der aktuelle Wert der Hilfslinie höher ist als der des Vortages, um Fehlsignale zu vermeiden.

-

Verwendung eines Trailing-Stop-Loss-Mechanismus: Die Stop-Loss-Linie wird in Abhängigkeit von der Kursentwicklung angepasst, um einen Teil der Gewinne zu sichern.

-

Gleichzeitige Festlegung eines festen prozentualen Stop-Loss und Take-Profit, um den maximalen Verlust und Gewinn pro Trade zu begrenzen.

Strategievorteile

-

Klare Handelssignale, einfache Bestimmung der Ein- und Ausstiegszeitpunkte.

-

Der doppelte DEMA-Algorithmus ist glatter, vermeidet Überoptimierung und liefert zuverlässigere Signale.

-

Der Filter der Hilfslinie verbessert die Signalerfassung und reduziert Fehlsignale.

-

Der Trailing-Stop-Loss sichert einen Teil der Gewinne und kontrolliert das Risiko effektiv.

-

Festlegung eines festen prozentualen Stop-Loss und Take-Profit begrenzt den maximalen Verlust pro Trade und verhindert, dass das Risiko außer Kontrolle gerät.

Strategierisiken

-

In Seitwärtsmärkten kann es zu häufigen Trades kommen, was leicht zu einer erhöhten Exposure und damit zu Verlusten der Strategie führen kann.

-

Ein zu groß eingestellter fester Stop-Loss-Prozentsatz kann in außergewöhnlichen Marktphasen zu einem großen Stop-Loss-Verlust führen.

-

DEMA-Cross-Signale sind verzögert; bei schnellen Kursbewegungen kann der Einstieg nahe dem Hoch des Marktes zu erhöhtem Verlustrisiko führen.

-

Bei der Implementierung im Live-Handel beeinflusst der Slippage die Rentabilität, daher müssen die Take-Profit- und Stop-Loss-Parameter angepasst werden.

Strategieoptimierung

-

Die DEMA-Parameter können je nach Marktlage angepasst werden, um den optimalen Balancepunkt zu finden.

-

Im Live-Handel sollte der Slippage berücksichtigt und der feste Stop-Loss-Bereich entsprechend erweitert werden.

-

Es können weitere Hilfsindikatoren wie MACD hinzugefügt werden, um die Signalqualität zu verbessern.

-

Es kann eine Schrittweite für den Trailing-Stop-Loss festgelegt werden, um die Stop-Loss-Logik zu optimieren.

Zusammenfassung

Diese Strategie nutzt die Trendbestimmungsfähigkeit der DEMA in Kombination mit einem Trailing-Mechanismus zur Risikokontrolle und ist ein sehr typischer Vertreter im System der Handelsstrategien, die die Trendrichtung bestimmen (Determine trend direction). Insgesamt bietet die Strategie klare Signale und sinnvolle Stop-Loss- und Take-Profit-Einstellungen. Sie ist eine leicht zu erlernende Handelsstrategie mit kontrolliertem Risiko. Im Live-Handel können durch die Optimierung der Slippage-Kosten und die Verwendung von Hilfsindikatoren gute Anlagerenditen erzielt werden.

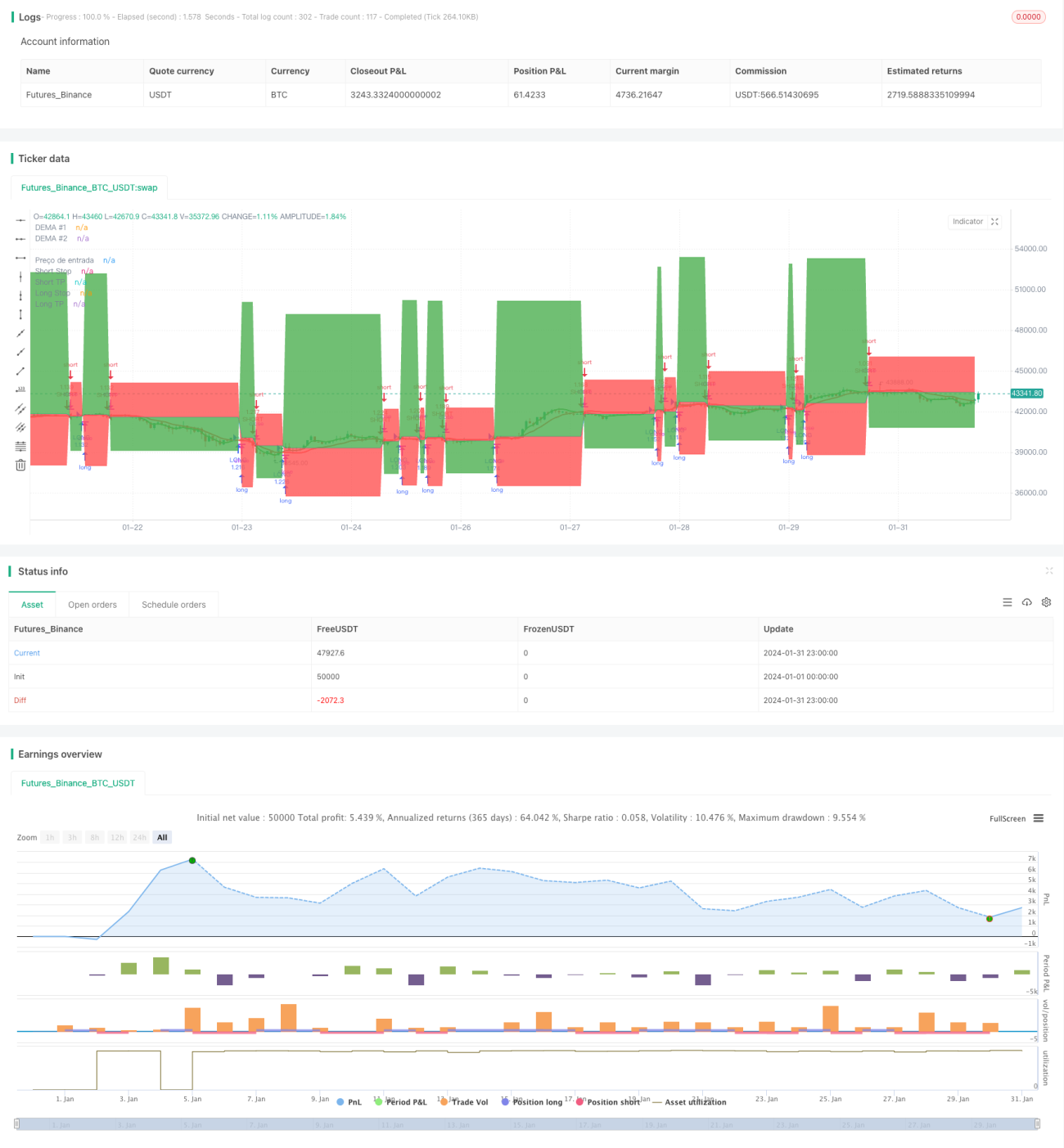

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © zeguela

//@version=4

strategy(title="ZEGUELA DEMABOT", commission_value=0.063, commission_type=strategy.commission.percent, initial_capital=100, default_qty_value=90, default_qty_type=strategy.percent_of_equity, overlay=true, process_orders_on_close=true)- 1