Gleichgewichtsstrategie für die psychologische Kontrolle im Handel

Übersicht

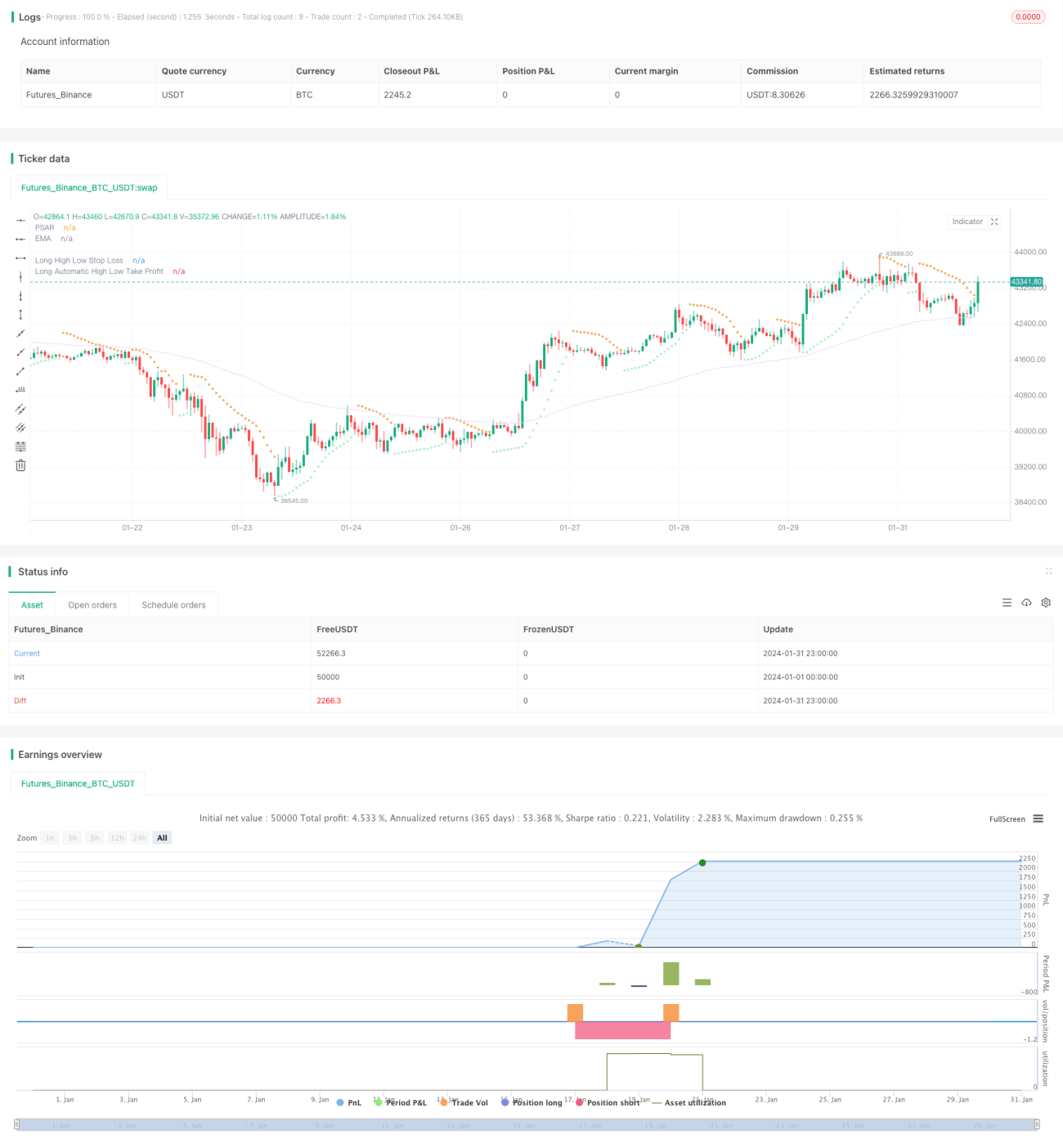

Der Zweck dieser Strategie ist es, durch die Einstellung verschiedener Parameter die Psychologie und die Handelsleistung des Händlers auszugleichen, um stabilere Renditen zu erzielen. Sie verwendet Indikatoren wie gleitende Durchschnitte, Bollinger-Bänder und Keltner-Kanäle, um Markttrends und Volatilität zu beurteilen, kombiniert mit dem PSAR-Indikator zur Erkennung von Umkehrsignalen und dem TTM-Squeeze-Indikator zur Beurteilung des Momentums. Die Handelssignale werden aus einer Kombination dieser Indikatoren generiert. Gleichzeitig verwendet die Strategie High-Low-Stopps und Risk-Reward-Take-Profit zur Risikosteuerung.

Strategieprinzip

Die Hauptlogik dieser Strategie ist wie folgt:

-

Trendbewertung: Verwendung des EMA (exponentiell gleitender Durchschnitt) zur Bestimmung der Preisrichtung. Liegt der Preis über dem EMA, ist der Trend aufwärts, darunter abwärts.

-

Umkehrbewertung: Verwendung des PSAR zur Erkennung von Preisumkehrpunkten. Ein PSAR-Punkt oberhalb des Preises ist ein bullisches Signal, unterhalb ein bärisches Signal.

-

Momentumbewertung: Verwendung des TTM-Squeeze-Indikators zur Beurteilung von Marktvolatilität und Momentum. Der TTM-Squeeze misst die Volatilität, indem er die Breite der Bollinger-Bänder und der Keltner-Kanäle vergleicht. Ein Squeeze bedeutet extrem niedrige Volatilität. Die Auflösung des Squeezes signalisiert eine Zunahme der Volatilität und eine bevorstehende größere Richtungsbewegung des Preises.

-

Erzeugung von Handelssignalen: Ein bullisches Signal wird erzeugt, wenn der Preis den EMA und den PSAR-Punkt nach oben durchbricht und der TTM-Squeeze-Indikator den Squeeze auflöst. Ein bärisches Signal wird erzeugt, wenn der Preis den EMA und den PSAR-Punkt nach unten durchbricht und der TTM-Squeeze-Indikator in den Squeeze eintritt.

-

Stop-Loss-Methode: Verwendung eines High-Low-Stopps. Der Stop-Loss-Punkt basiert auf dem höchsten oder niedrigsten Preis eines bestimmten aktuellen Zeitraums multipliziert mit einem eingestellten Faktor.

-

Take-Profit-Methode: Verwendung eines automatischen Risk-Reward-Take-Profit. Der Take-Profit-Punkt wird berechnet, indem das Verhältnis des Stop-Loss-Abstands zum aktuellen Preis mit dem eingestellten Risk-Reward-Verhältnis multipliziert wird.

Durch die Parametereinstellung können die Handelsfrequenz, das Positionsmanagement, die Stop-Loss- und Take-Profit-Punkte kontrolliert werden, um die Handelspsychologie auszugleichen.

Vorteilsanalyse

-

Mehrere Indikatoren zur Beurteilung erhöhen die Signalgenauigkeit.

-

Umkehrungsorientiert, mit Trendfolge als Ergänzung, um Umkehrpunkte zu erfassen und die Wahrscheinlichkeit von Kaufen zu hohen oder Verkaufen zu niedrigen Kursen zu reduzieren.

-

Der TTM-Squeeze-Indikator kann effektiv Korrekturen im Trend erkennen und ineffektive Trades während der Korrekturphase vermeiden.

-

Die High-Low-Stop-Loss-Methode ist einfach und praktisch und kann je nach Markt angepasst werden.

-

Die Risk-Reward-Take-Profit-Methode quantifiziert das Verhältnis von Gewinn zu Verlust und erleichtert Anpassungen.

-

Verschiedene Parametereinstellungen sind flexibel und können je nach persönlicher Risikobereitschaft feinjustiert werden.

Risikoanalyse

-

Die Kombination mehrerer Indikatoren erhöht zwar die Signalgenauigkeit, kann aber auch dazu führen, dass Einstiegspunkte übersprungen werden.

-

Eine umkehrungsorientierte Strategie kann in Trendmärkten schlecht abschneiden.

-

High-Low-Stopps können manchmal durchbrochen werden und bieten keinen vollständigen Risikoschutz.

-

Das Risk-Reward-Take-Profit kann aufgrund von Preissprüngen oder Anpassungen unwirksam werden.

-

Falsche Parametereinstellungen können zu Verlusten oder häufigen Stopps führen.

Optimierungsmöglichkeiten

-

Hinzufügen oder Anpassen von Indikatorgewichten, um die Signale genauer zu machen.

-

Optimieren der Parameter für Umkehr- und Trendindikatoren, um die Gewinnwahrscheinlichkeit zu erhöhen.

-

Optimieren der Parameter für High-Low-Stopps, um die Stopps sinnvoller zu gestalten.

-

Testen verschiedener Risk-Reward-Verhältnisse, um optimale Ergebnisse zu erzielen.

-

Anpassen der Positionsgrößenparameter, um die Auswirkungen einzelner Verluste zu reduzieren.

Zusammenfassung

Insgesamt kann diese Strategie durch die Kombination von Indikatoren und die Anpassung von Parametern die Handelspsychologie effektiv ausgleichen und stabile positive Renditen erzielen. Obwohl noch Verbesserungspotenzial besteht, hat sie bereits einen praktischen Anwendungswert. Durch Marktfeedback und Feinabstimmung der Parameter hat diese Strategie das Potenzial, ein wirksames Instrument zur Kontrolle der Handelspsychologie und zur Erzielung langfristig stabiler Gewinne zu werden.

- 1