Dreifach bestätigte Trendfolgestrategie

Übersicht

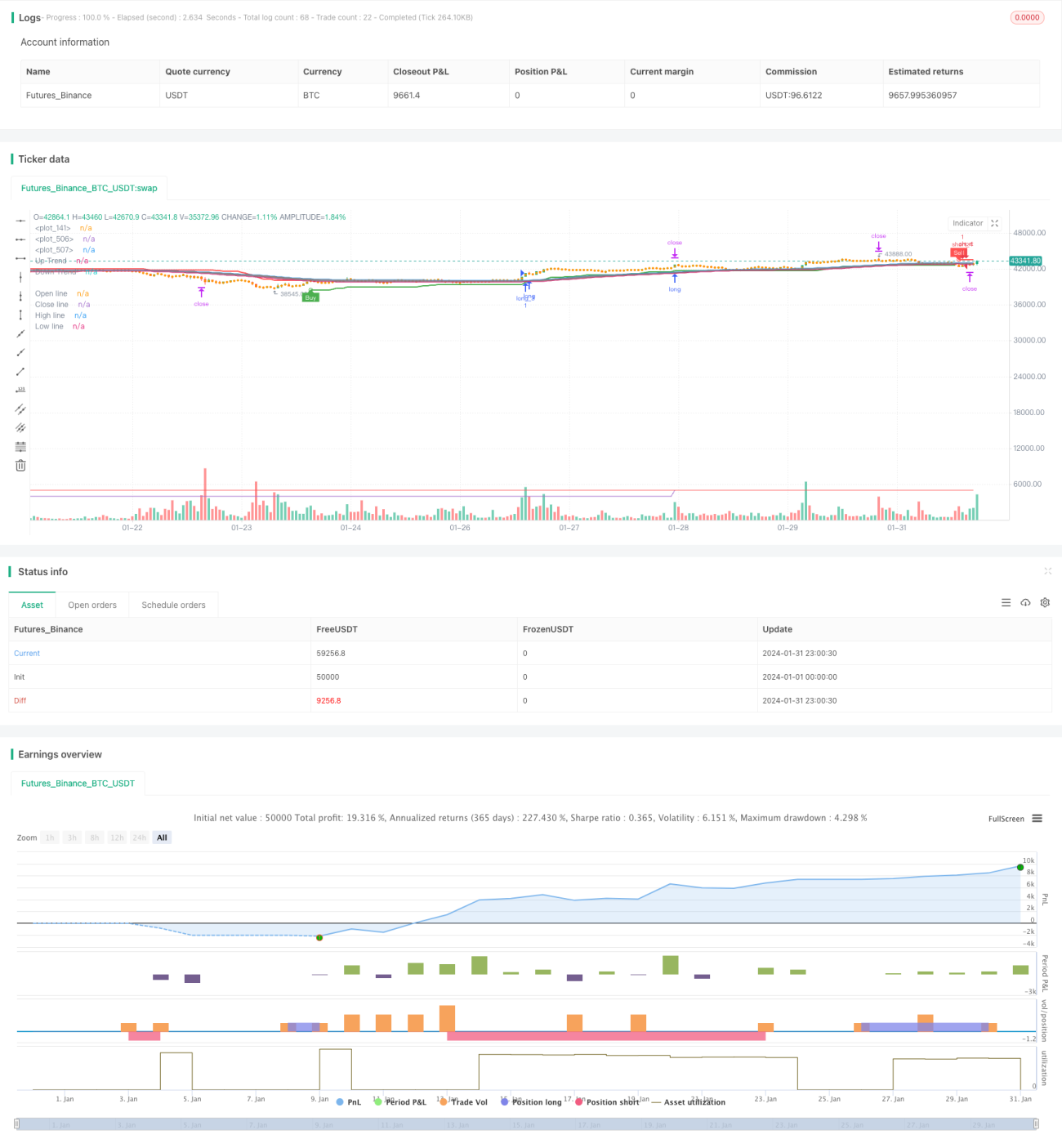

Die Dreifachbestätigungs-Trendfolgestrategie kombiniert die Signale von drei wichtigen Indikatoren – gleitendem Mittelwert, Vergessenslinie und SuperTrend –, um Trends mit hoher Wahrscheinlichkeit zu erfassen. Wenn alle drei Indikatoren gleichzeitig ein Kauf- oder Verkaufssignal ausgeben, steigt die Strategie rechtzeitig ein und folgt dem Trend. Sobald der Trend umkehrt, stoppt die Strategie schnell und eröffnet eine Short-Position.

Strategieprinzip

Gleitender Mittelwert zur Bestimmung des Haupttrends

Die Strategie verwendet einen gleitenden Mittelwert mit einer Periode von 52, um die Richtung des Haupttrends zu bestimmen. Wenn der Kurs den gleitenden Mittelwert von unten nach oben durchbricht, wird ein Aufwärtstrend angenommen; bei einem Durchbruch von oben nach unten ein Abwärtstrend.

Vergessenslinie zur Erkennung sekundärer Umkehrungen

Gleichzeitig wird die Vergessenslinie verwendet, um kurzfristige sekundäre Umkehrungen zu identifizieren. Die Berechnung der Vergessenslinie ähnelt der des gleitenden Mittelwerts, jedoch wird der Schlusskurs durch den Eröffnungskurs ersetzt, was eine schnellere Reaktion auf Kursumkehrungen ermöglicht. Wenn der Kurs die fallende Vergessenslinie von unten nach oben durchbricht, deutet dies auf eine kurzfristige Stabilisierung und Erholung der Kurse hin; bei einem Durchbruch der steigenden Vergessenslinie von oben nach unten signalisiert dies einen kurzfristigen Rückgang der Kurse.

SuperTrend zur Bestimmung von Umkehrpunkten

Die Strategie kombiniert zusätzlich den SuperTrend-Indikator, um entscheidende Umkehrpunkte zu ermitteln. Der SuperTrend nutzt den ATR-Fensterzeitraum und die Kursdaten, um die oberen und unteren Kanäle dynamisch anzupassen und den Zeitpunkt der Umkehrung zu bestimmen.

Dreifachbestätigung der Signale

Die Strategie geht nur dann long, wenn der gleitende Mittelwert, die Vergessenslinie und der SuperTrend gleichzeitig ein Kaufsignal ausgeben; nur dann short, wenn alle drei gleichzeitig ein Verkaufssignal ausgeben. Durch die Dreifachbestätigung der Indikatoren werden Fehlsignale effektiv herausgefiltert und die Einstiegswahrscheinlichkeit erhöht.

Vorteile

Mehrdimensionale Bewertung, hohe Wahrscheinlichkeit

Durch die Kombination von gleitendem Mittelwert, Vergessenslinie und SuperTrend beurteilt die Strategie Trends und Schlüsselpunkte aus verschiedenen Dimensionen und gewährleistet so einen Einstieg mit hoher Wahrscheinlichkeit.

Schnelle Reaktion, Echtzeitverfolgung

Die Einführung der Vergessenslinie stellt sicher, dass die Strategie schnell auf kurzfristige Kursumkehrungen reagieren kann; der SuperTrend mit ATR-angepasstem Kanal verfolgt Kursänderungen ebenfalls in Echtzeit.

Automatisches Take-Profit und Stop-Loss, effektive Risikokontrolle

Die Strategie verfügt über eine integrierte Take-Profit- und Stop-Loss-Logik, die die Take-Profit- und Stop-Loss-Punkte dynamisch an den ATR anpasst und so den Verlust pro Trade effektiv begrenzt.

Risiken und Lösungen

Risiko zu hoher Handelsfrequenz

Aufgrund der häufigen Handelssignale kann es zu übermäßigem Handel kommen. Dies kann durch eine angemessene Vergrößerung der MA-Periode reduziert werden, um die Handelsfrequenz zu senken.

Risiko der Umkehrungsunsicherheit

Die Wirksamkeit der Vergessenslinie und des SuperTrend bei der Erkennung von Umkehrpunkten ist nicht garantiert; es besteht das Risiko von Fehleinschätzungen. Zusätzliche Filterbedingungen für die Indikatorparameter können eingeführt werden, um Umkehrsignale mit höherer Wahrscheinlichkeit zu gewährleisten.

Verlustrisiko in Seitwärtsmärkten

In Seitwärtsmärkten führt die wiederholte Überschneidung der Indikatoren zu häufigen Eröffnungen und anschließenden Stop-Loss-Verlusten. Dieses Risiko kann durch die Identifizierung von Seitwärtsmärkten und das vorübergehende Aussetzen der Strategie in diesen Phasen gemindert werden.

Optimierungsmöglichkeiten

Einbeziehung von Volatilitätsindikatoren

Die Verwendung von Volatilitätsindikatoren wie den Bollinger Bändern könnte in Betracht gezogen werden. Wenn sich der Kurs den oberen oder unteren Bändern nähert, sollte die Eröffnung neuer Positionen vermieden werden, um das Risiko von Seitwärtsmärkten effektiv zu umgehen.

Zusätzliche Einstiegsfilter

Es könnten weitere unterstützende Indikatoren wie KDJ oder MACD hinzugefügt werden. Ein Einstieg erfolgt nur, wenn diese ebenfalls gleichzeitig Signale ausgeben. Dies filtert Fehlsignale weiter heraus und reduziert unnötige Trades.

Optimierung der Take-Profit- und Stop-Loss-Strategie

Die Take-Profit- und Stop-Loss-Strategie kann optimiert werden, z. B. durch einen nachlaufenden Take-Profit, einen exponentiell nachlaufenden Take-Profit oder einen gestaffelten Teil-Take-Profit, um Gewinne stabiler und höher zu gestalten.

Zusammenfassung

Die Dreifachbestätigungs-Trendfolgestrategie nutzt die Stärken der drei Indikatoren – gleitender Mittelwert, Vergessenslinie und SuperTrend –, um Trends mit hoher Wahrscheinlichkeit zu erkennen und zu verfolgen. Gleichzeitig sorgt der automatische Take-Profit- und Stop-Loss-Mechanismus für eine effektive Begrenzung der Einzelverluste. Eine weitere Optimierung durch zusätzliche Hilfsindikatoren zur Einstiegsfilterung sowie Verbesserungen der Take-Profit- und Stop-Loss-Strategie sind empfehlenswert, um die Strategie noch praktikabler zu machen.

- 1