Ruda Momentum-Trend-Handelsstrategie

Übersicht

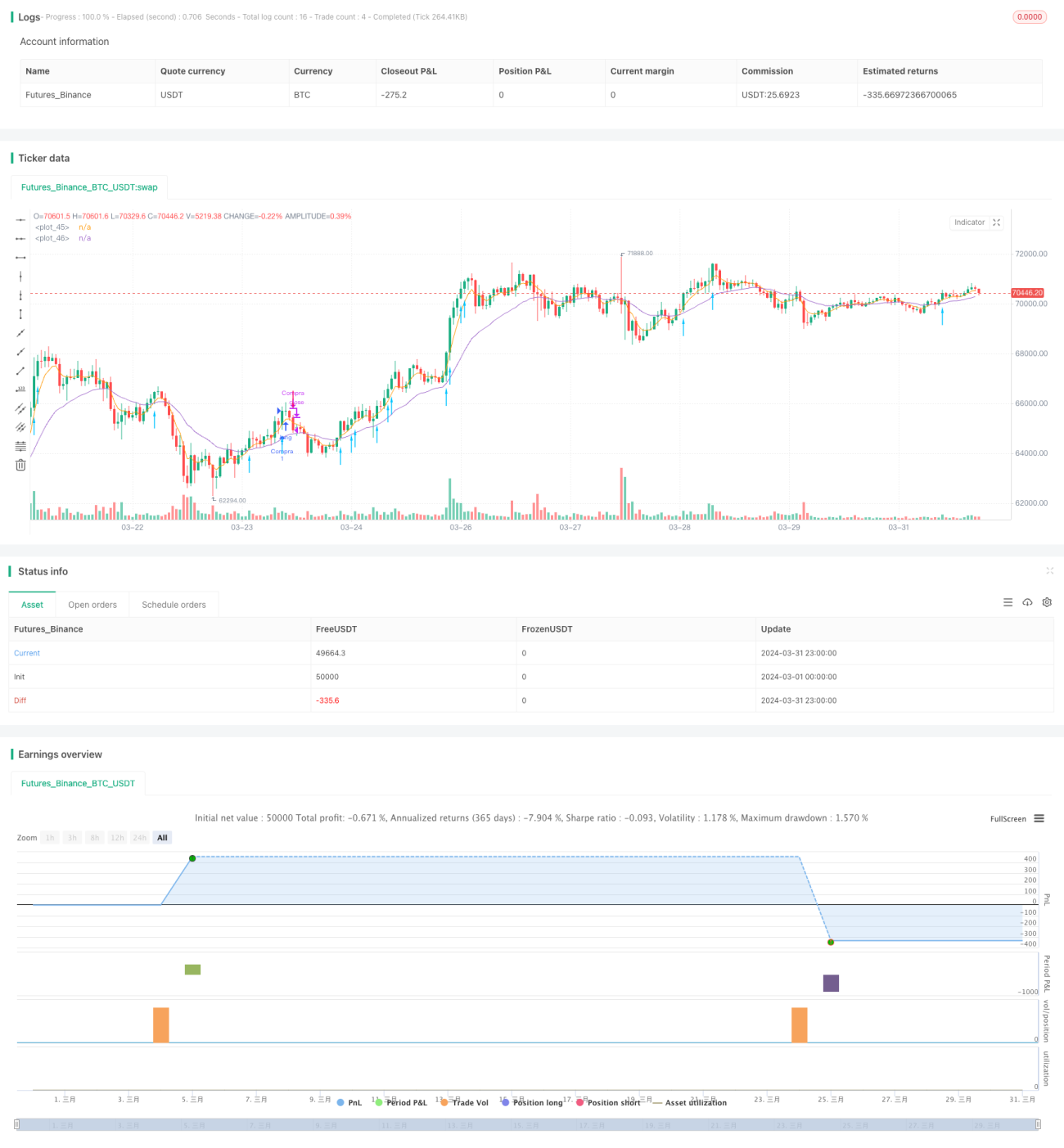

Die Ruda-Momentum-Trend-Handelsstrategie ist eine quantitative Handelsstrategie, die auf Momentum- und Trendindikatoren basiert. Die Strategie verwendet Indikatoren wie OBV (On Balance Volume), EMA (Exponential Moving Average) und die Kerzenkörper-Verhältnisse, um Kauf- und Verkaufssignale zu bestimmen. Wenn die kurzfristige EMA die langfristige EMA von unten nach oben kreuzt, der OBV ein neues 10-Tage-Hoch erreicht und das Kerzenkörper-Verhältnis über dem festgelegten Schwellenwert (Standard 50 %) liegt, wird die Strategie am nächsten Tag zum Eröffnungskurs kaufen. Wenn der Preis unter den Stop-Loss-Kurs fällt oder der Schlusskurs unter die kurzfristige EMA fällt, wird die Position geschlossen.

Strategieprinzip

- Berechnung von zwei EMA-Linien: kurzfristige EMA mit Parameter 5, langfristige EMA mit Parameter 21. Wenn die kurzfristige EMA die langfristige EMA von unten nach oben kreuzt, gilt der Trend als aufwärts gerichtet, andernfalls als abwärts.

- Berechnung des OBV-Indikators. Wenn der OBV ein 10-Tage-Hoch erreicht, gilt die bullische Dynamik als stark.

- Berechnung des Kerzenkörper-Anteils. Wenn der Anteil über dem festgelegten Schwellenwert (Standard 50 %) liegt, gilt der Trend als bestätigt.

- Wenn der Trend aufwärts gerichtet ist, die bullische Dynamik stark ist und der Trend bestätigt ist, kauft die Strategie am nächsten Tag zum Eröffnungskurs. Der Stop-Loss-Kurs ist das Minimum aus dem Tagestief und dem Eröffnungskurs minus 1 %.

- Wenn der Preis unter den Stop-Loss-Kurs fällt oder der Schlusskurs unter die kurzfristige EMA fällt, wird die Position geschlossen.

Vorteilsanalyse

- Kombination von Trend- und Momentumindikatoren ermöglicht das Erfassen starker Instrumente.

- Der Kauf zum Eröffnungskurs am nächsten Tag und der dynamische Stop-Loss können teilweise falsche Ausbrüche vermeiden.

- Klare Stop-Loss- und Take-Profit-Bedingungen, kontrolliertes Risiko.

Risikoanalyse

- Trend- und Momentumindikatoren haben eine Verzögerung, was zu Nachkauf zu hohen Kursen und vorzeitigem Stop-Loss führen kann.

- Feste Parameter ohne Anpassungsfähigkeit, die Performance kann in verschiedenen Marktzuständen stark variieren.

- Backtesting nur auf einem Markt und einem Instrument, die Stabilität und Anwendbarkeit der Strategie muss weiter validiert werden.

Optimierungsrichtungen

- Optimierung der Parameter der Trend- und Momentumindikatoren zur Verbesserung der Sensitivität und Effektivität.

- Einführung einer Marktzustandsbewertung, um Parameter dynamisch an die aktuellen Marktcharakteristika anzupassen.

- Erweiterung des Backtesting-Bereichs auf verschiedene Märkte und Instrumente, um die Robustheit der Strategie zu erhöhen.

- Berücksichtigung von Positionsmanagement- und Risikokontrollmodulen zur Verbesserung des Risiko-Ertrags-Verhältnisses.

Zusammenfassung

Die Ruda-Momentum-Trend-Handelsstrategie ist eine einfach anwendbare quantitative Handelsstrategie, die durch die Kombination von Trend- und Momentumindikatoren starke Instrumente und Trendchancen erfassen kann. Die Strategie weist jedoch auch gewisse Einschränkungen auf, wie z. B. Indikatorverzögerungen und feste Parameter. Zukünftige Optimierungen könnten die Verbesserung der Indikatorparameter, die Einführung adaptiver Mechanismen, die Erweiterung des Backtesting-Bereichs und die Stärkung des Risikomanagements umfassen, um die Robustheit und Rentabilität der Strategie zu steigern.

- 1