Übersicht

Diese Strategie nutzt mehrere gleitende Durchschnitte (VWMA), den Average Directional Index (ADX) sowie den Directional Movement Index (DMI), um Long-Chancen im Bitcoin-Markt zu identifizieren. Durch die Kombination mehrerer technischer Indikatoren wie Preismomentum, Trendrichtung und Handelsvolumen zielt die Strategie darauf ab, Einstiegspunkte mit starkem Aufwärtstrend und ausreichendem Momentum zu finden, während das Risiko streng kontrolliert wird.

Funktionsweise der Strategie

- Verwendung von 9- und 14-Tage-VWMA zur Beurteilung des Long-Trends: Ein Long-Signal entsteht, wenn der kurzfristige gleitende Durchschnitt den langfristigen nach oben kreuzt.

- Einführung einer adaptiven gleitenden Linie, die aus dem 89-Tage-Höchst- und Tiefstpreis-VWMA konstruiert wird, als Trendfilter: Eine Position wird nur eröffnet, wenn der Schluss- oder Eröffnungskurs über dieser Linie liegt.

- Bestätigung der Trendstärke durch ADX- und DMI-Indikatoren: Eine Position wird nur dann als ausreichend stark erachtet, wenn der ADX größer als 18 ist und die Differenz zwischen +DI und -DI größer als 15 beträgt.

- Verwendung einer Volumen-Perzentil-Funktion, um nur Kerzen mit einem Handelsvolumen zwischen 60 % und 95 % zu filtern und Zeiten mit niedrigem Volumen zu vermeiden.

- Setzen eines Stop-Loss bei 0,96–0,99 des Hochs der vorherigen Kerze, wobei der Faktor mit größerem Zeitrahmen abnimmt, um das Risiko zu kontrollieren.

- Schließen der Position bei Erreichen der vorgegebenen Haltedauer oder wenn der Preis unter die adaptive gleitende Linie fällt.

Vorteile

- Kombination mehrerer technischer Indikatoren, um den Markt aus verschiedenen Dimensionen wie Trend, Momentum und Volumen zu bewerten, was die Zuverlässigkeit der Signale erhöht.

- Der adaptive gleitende Durchschnitt und der Volumenfilter können falsche Signale effektiv herausfiltern und ineffiziente Trades reduzieren.

- Strenge Stop-Loss-Einstellungen und Haltedauerbegrenzung reduzieren das Risiko der Strategie erheblich.

- Modulare Codestruktur mit guter Lesbarkeit und Wartbarkeit, die eine weitere Optimierung und Erweiterung erleichtert.

Risikoanalyse

- In Seitwärtsbewegungen oder unklaren Trends kann die Strategie viele falsche Signale erzeugen.

- Der Stop-Loss ist relativ eng, sodass er bei hoher Volatilität vorzeitig ausgelöst werden kann, was zu Verlusten führen kann.

- Fehlende Berücksichtigung makroökonomischer Faktoren und bedeutender Ereignisse; die Strategie kann bei „Black Swan“-Ereignissen versagen.

- Die Parameter sind relativ fest eingestellt und nicht adaptiv, was in verschiedenen Marktumgebungen zu instabilen Ergebnissen führen kann.

Optimierungsmöglichkeiten

- Einführung weiterer Indikatoren zur Charakterisierung des Marktumfelds, wie z. B. Relative Strength Index (RSI) oder Bollinger-Bänder, um die Zuverlässigkeit der Signale zu verbessern.

- Dynamische Optimierung der Stop-Loss-Position, z. B. durch ATR oder prozentuale Stop-Loss, um sich an unterschiedliche Marktvolatilitäten anzupassen.

- Kombination mit makroökonomischen Daten und Stimmungsanalysen, um das Risikomanagement der Strategie zu verbessern.

- Automatisierte Parameteroptimierung mit maschinellen Lernalgorithmen, um die Anpassungsfähigkeit und Stabilität der Strategie zu steigern.

Zusammenfassung

Die VWMA-ADX-Bitcoin-Long-Strategie berücksichtigt mehrere technische Indikatoren wie Preistrend, Momentum und Handelsvolumen und kann Aufwärtschancen im Bitcoin-Markt relativ effektiv identifizieren. Gleichzeitig sorgen strenge Risikomanagementmaßnahmen und klare Ausstiegsbedingungen für eine gute Kontrolle des Risikos. Allerdings hat die Strategie auch Einschränkungen, wie eine unzureichende Anpassungsfähigkeit an veränderte Marktbedingungen und Optimierungsbedarf bei der Stop-Loss-Strategie. Zukünftige Verbesserungen könnten sich auf die Zuverlässigkeit der Signale, das Risikomanagement und die Parameteroptimierung konzentrieren, um die Robustheit und Rentabilität weiter zu steigern. Insgesamt bietet die VWMA-ADX-Bitcoin-Long-Strategie Anlegern einen systematischen Handelsansatz, der auf Momentum und Trend basiert und eine weitere Erforschung und Verbesserung verdient.

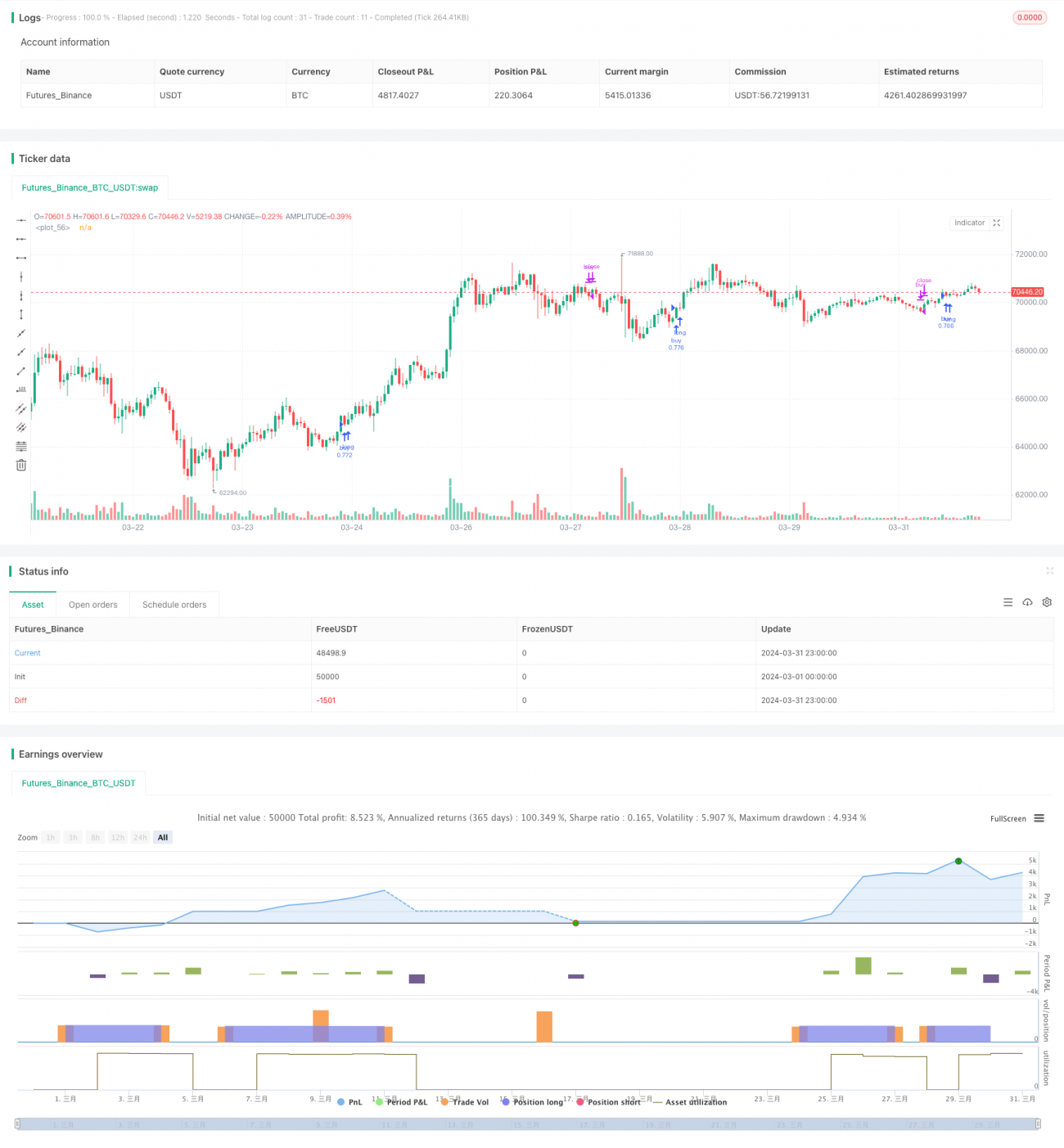

/*backtest

start: 2024-03-01 00:00:00

end: 2024-03-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Q_D_Nam_N_96

//@version=5

- 1