AlphaTradingBot Handelsstrategie

Überblick

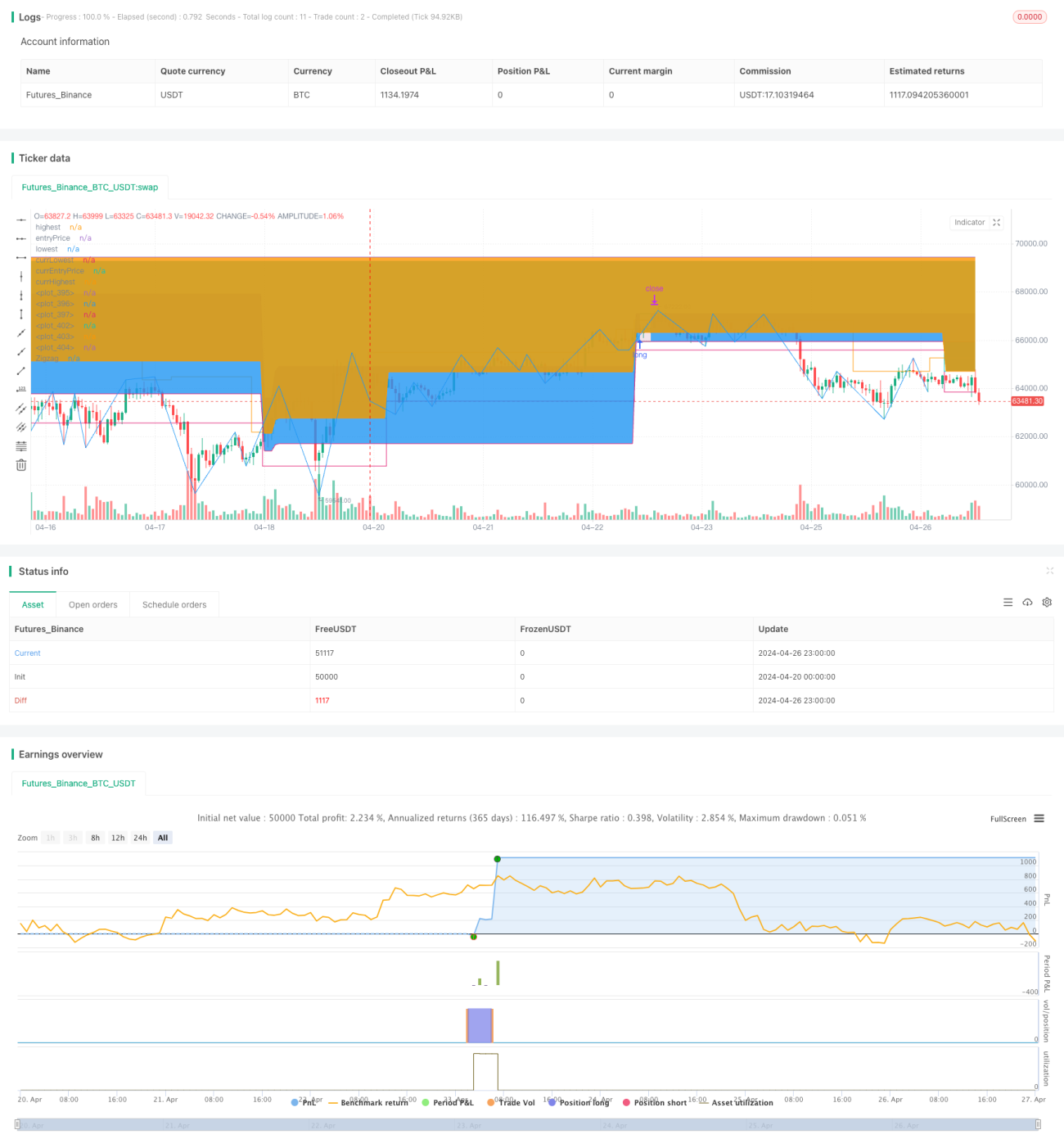

AlphaTradingBot ist eine Intraday-Handelsstrategie, die auf dem Zigzag-Indikator und der Fibonacci-Folge basiert. Die Strategie erkennt Trends durch die Identifizierung von Markthochs (HH) und Markttiefs (LL) und setzt Einstiegspunkte, Take-Profit und Stop-Loss unter Verwendung von Fibonacci-Retracements und -Extensions. Die Strategie wird nur innerhalb eines festgelegten Datumsbereichs ausgeführt, kann sowohl Long- als auch Short-Positionen eröffnen und bietet eine gewisse Fähigkeit zur Trendbestimmung sowie ein gutes Risiko-Ertrags-Verhältnis.

Strategieprinzip

- Identifizierung von Markthochs (HH), Markttiefs (LL), höheren Tiefs (HL) und niedrigeren Hochs (LH) mithilfe des Zigzag-Indikators.

- Bei Auftreten eines HH wird dies als Beginn eines Aufwärtstrends betrachtet und es wird nach Long-Einstiegsmöglichkeiten gesucht. Bei Auftreten eines LL wird dies als Beginn eines Abwärtstrends betrachtet und es wird nach Short-Einstiegsmöglichkeiten gesucht.

- Im Aufwärtstrend: Wenn ein HL auftritt, wird das Intervall zwischen diesem HL und dem vorherigen LL als Fibonacci-Retracement-Bereich für Long-Positionen verwendet. Wenn der Kurs das vorherige Hoch durchbricht, wird eine Long-Position im Bereich des Retracements von 23,6 % – 38,2 % (einstellbar) eröffnet. Der Stop-Loss wird bei 61,8 % Retracement gesetzt, der Take-Profit basiert auf dem RR-Wert (einstellbar).

- Im Abwärtstrend: Wenn ein LH auftritt, wird das Intervall zwischen diesem LH und dem vorherigen HH als Fibonacci-Retracement-Bereich für Short-Positionen verwendet. Wenn der Kurs das vorherige Tief durchbricht, wird eine Short-Position im Bereich des Retracements von 61,8 % – 76,4 % (einstellbar) eröffnet. Der Stop-Loss wird bei 38,2 % Retracement gesetzt, der Take-Profit basiert auf dem RR-Wert (einstellbar).

- Orderverwaltung: Pro Signal wird nur eine Position eröffnet, bis diese geschlossen wird. Wenn der Verlust einer einzelnen Position X % (einstellbar) des Gesamtkontos erreicht, wird die Strategie gestoppt.

Vorteilsanalyse

- Starke Trendverfolgungsfähigkeit. Durch die effektive Erkennung von Trends mithilfe des Zigzag-Indikators kann frühzeitig in den Trend eingestiegen werden.

- Klare Retracement-Logik. Die Nutzung von Fibonacci-Retracements zur Festlegung des Einstiegsbereichs ermöglicht einen Einstieg bei Trendkorrekturen mit relativ hoher Erfolgsquote.

- Kontrollierbares Risiko. Durch die Festlegung eines maximalen Verlustprozentsatzes pro Trade wird das Risiko jedes einzelnen Geschäfts begrenzt, und das strenge Stop-Loss-System stellt sicher, dass das Gesamtrisiko kontrollierbar bleibt.

- Optimierbares Risiko-Ertrags-Verhältnis. Der RR-Wert kann je nach Marktcharakteristik und persönlichen Präferenzen angepasst werden, um das Risiko-Ertrags-Verhältnis der Strategie zu optimieren.

Risikoanalyse

- Häufiger Handel. Aufgrund der hohen Empfindlichkeit des Zigzag-Indikators können häufig Signale generiert werden, was zu übermäßigem Handel führen kann.

- Ungenaue Trendbestimmung. Die durch den Zigzag-Indikator identifizierten Trends können dennoch Abweichungen aufweisen, was zu suboptimalen Einstiegszeitpunkten führen kann.

- Schwache Performance in Seitwärtsmärkten. In einem Seitwärtsmarkt kann die Strategie zu vielen Verlusttrades führen.

- Begrenzter Laufzeitbereich. Die Strategie läuft nur innerhalb eines festgelegten Datumsbereichs, sodass möglicherweise Teile des Kursverlaufs verpasst werden.

Optimierungsmöglichkeiten

- Einführung weiterer technischer Indikatoren wie MA, MACD usw. zur Verbesserung der Genauigkeit der Trendbestimmung.

- Optimierung des Positionsmanagements, z. B. dynamische Anpassung der Positionsgröße basierend auf dem ATR.

- Optimierung der Take-Profit- und Stop-Loss-Logik, z. B. dynamische Anpassung des Stop-Loss-Levels an die Marktvolatilität.

- Einführung von Marktstimmungsindikatoren, um bei extremer Optimismus oder Pessimismus den Einstieg zu vermeiden.

- Lockerung der Datumsbeschränkung, um die Allgemeingültigkeit der Strategie zu erhöhen.

Zusammenfassung

AlphaTradingBot ist eine trendfolgende Intraday-Strategie, die auf dem Zigzag-Indikator und Fibonacci-Retracements basiert. Sie erkennt Trends anhand von Hochs und Tiefs und steigt bei Trendkorrekturen ein, um eine höhere Erfolgsquote und ein besseres Risiko-Ertrags-Verhältnis zu erzielen. Die Stärken der Strategie liegen in der guten Trendbestimmung, der klaren Retracement-Logik und dem messbaren Risiko. Gleichzeitig bestehen jedoch Risiken wie übermäßiger Handel, Abweichungen in der Trendbestimmung und schwache Performance in Seitwärtsmärkten. Zukünftig kann die Strategie durch den Einsatz weiterer technischer Indikatoren, verbessertes Positionsmanagement, optimierte Take-Profit-/Stop-Loss-Logik und Marktstimmungsindikatoren optimiert werden, um ihre Stabilität und Rentabilität zu steigern.

- 1