Auf dem Z-Wert basierende Trendfolgestrategie

Überblick

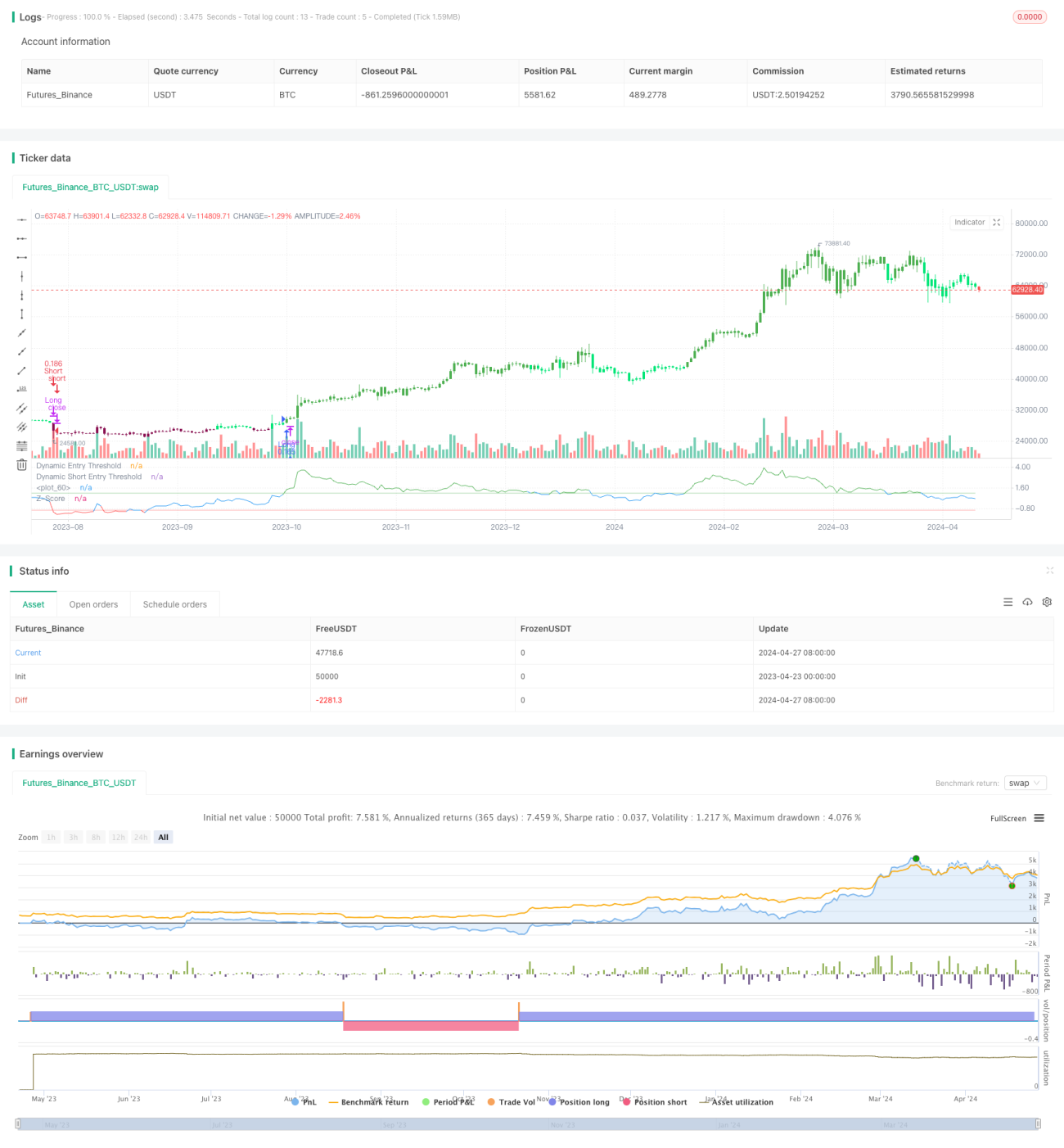

Die „Z-Score-basierte Trendfolgestrategie“ nutzt den statistischen Indikator Z-Score, um Trendchancen zu erfassen, indem das Ausmaß der Abweichung des Preises von seinem gleitenden Durchschnitt gemessen und die Standardabweichung als Normalisierungsskala verwendet wird. Die Strategie zeichnet sich durch ihre Einfachheit und Effektivität aus, insbesondere in Märkten, in denen Preisbewegungen häufig zur Mittellinie zurückkehren. Im Gegensatz zu komplexen Systemen, die auf mehreren Indikatoren basieren, konzentriert sich die „Z-Score-Trendstrategie“ auf klare, statistisch signifikante Preisbewegungen und eignet sich daher ideal für Händler, die einen schlanken, datengesteuerten Ansatz bevorzugen.

Funktionsweise der Strategie

Das Kernstück der Strategie ist die Berechnung des Z-Scores. Der Z-Score wird berechnet, indem die Differenz zwischen dem aktuellen Preis und einem vom Benutzer definierten exponentiell gleitenden Durchschnitt (EMA) des Preises durch die Standardabweichung des Preises über denselben Zeitraum geteilt wird:

z = (x - μ) / σ

wobei x der aktuelle Preis, μ der EMA-Mittelwert und σ die Standardabweichung ist.

Handelssignale werden generiert, wenn der Z-Score vordefinierte Schwellenwerte überschreitet:

- Long-Einstieg: Wenn der Z-Score einen positiven Schwellenwert von unten nach oben durchbricht.

- Long-Ausstieg: Wenn der Z-Score einen negativen Schwellenwert von oben nach unten durchbricht.

- Short-Einstieg: Wenn der Z-Score einen negativen Schwellenwert von oben nach unten durchbricht.

- Short-Ausstieg: Wenn der Z-Score einen positiven Schwellenwert von unten nach oben durchbricht.

Vorteile der Strategie

- Einfach und effektiv: Die Strategie basiert auf wenigen Parametern, ist leicht zu verstehen und umzusetzen und gleichzeitig wirksam bei der Identifizierung von Trendchancen.

- Statistische Grundlage: Der Z-Score als bewährtes statistisches Instrument bietet eine solide theoretische Grundlage für die Strategie.

- Anpassungsfähigkeit: Durch Anpassung der Parameter wie Schwellenwerte, EMA-Berechnungszeitraum und Standardabweichung kann die Strategie flexibel an verschiedene Handelsstile und Marktbedingungen angepasst werden.

- Klare Signale: Die auf dem Durchbrechen von Schwellenwerten basierenden Handelssignale sind eindeutig und ermöglichen schnelle Entscheidungen und Ausführungen.

Risiken der Strategie

- Parameterempfindlichkeit: Ungeeignete Parametereinstellungen (z. B. zu hohe oder zu niedrige Schwellenwerte) können zu verzerrten Handelssignalen führen, Chancen verpassen oder Verluste verursachen.

- Trendidentifikation: In Seitwärts- oder Konsolidierungsmärkten kann die Strategie häufige Fehlsignale erzeugen und eine schlechte Performance aufweisen.

- Verzögerungseffekt: Als Trendfolgestrategie weisen sowohl Ein- als auch Ausstiegssignale eine gewisse Verzögerung auf, was dazu führen kann, dass der optimale Zeitpunkt verpasst wird.

Die genannten Risiken können durch kontinuierliche Marktanalyse, Parameteroptimierung und sorgfältige Umsetzung auf der Grundlage von Backtests kontrolliert und gemindert werden.

Optimierungsmöglichkeiten

- Dynamische Schwellenwerte: Die Einführung von volatilitätsabhängigen dynamischen Schwellenwerten kann sich effektiv an verschiedene Marktzustände anpassen und die Signalqualität verbessern.

- Kombinierte Indikatoren: Die Integration anderer technischer Indikatoren wie RSI, MACD usw. zur sekundären Bestätigung von Handelssignalen erhöht die Zuverlässigkeit.

- Positionsmanagement: Die Einbeziehung von Positionskontrollmechanismen wie ATR, um in Seitwärtsmärkten rechtzeitig die Position zu reduzieren und in Trendmärkten die Position aufzustocken, optimiert das Risiko-Ertrags-Verhältnis.

- Mehrere Zeitrahmen: Die Berechnung des Z-Scores über mehrere Zeitrahmen hinweg erfasst Trends auf verschiedenen Ebenen und erweitert die strategische Dimension.

Zusammenfassung

Die „Z-Score-basierte Trendfolgestrategie“ bietet mit ihrer Einfachheit, Robustheit und Flexibilität eine einzigartige Perspektive zur Erfassung von Trendchancen. Durch angemessene Parametereinstellungen, sorgfältiges Risikomanagement und kontinuierliche Optimierung kann die Strategie zu einem wertvollen Werkzeug für quantitative Trader werden, um in sich verändernden Märkten stabil voranzukommen.

/*backtest

start: 2023-04-23 00:00:00

end: 2024-04-28 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// This strategy employs a statistical approach by using a Z-score, which measures the deviation of the price from its moving average normalized by the standard deviation.- 1