MACD RSI Ichimoku Momentum-Trend-Long-Strategie

Übersicht

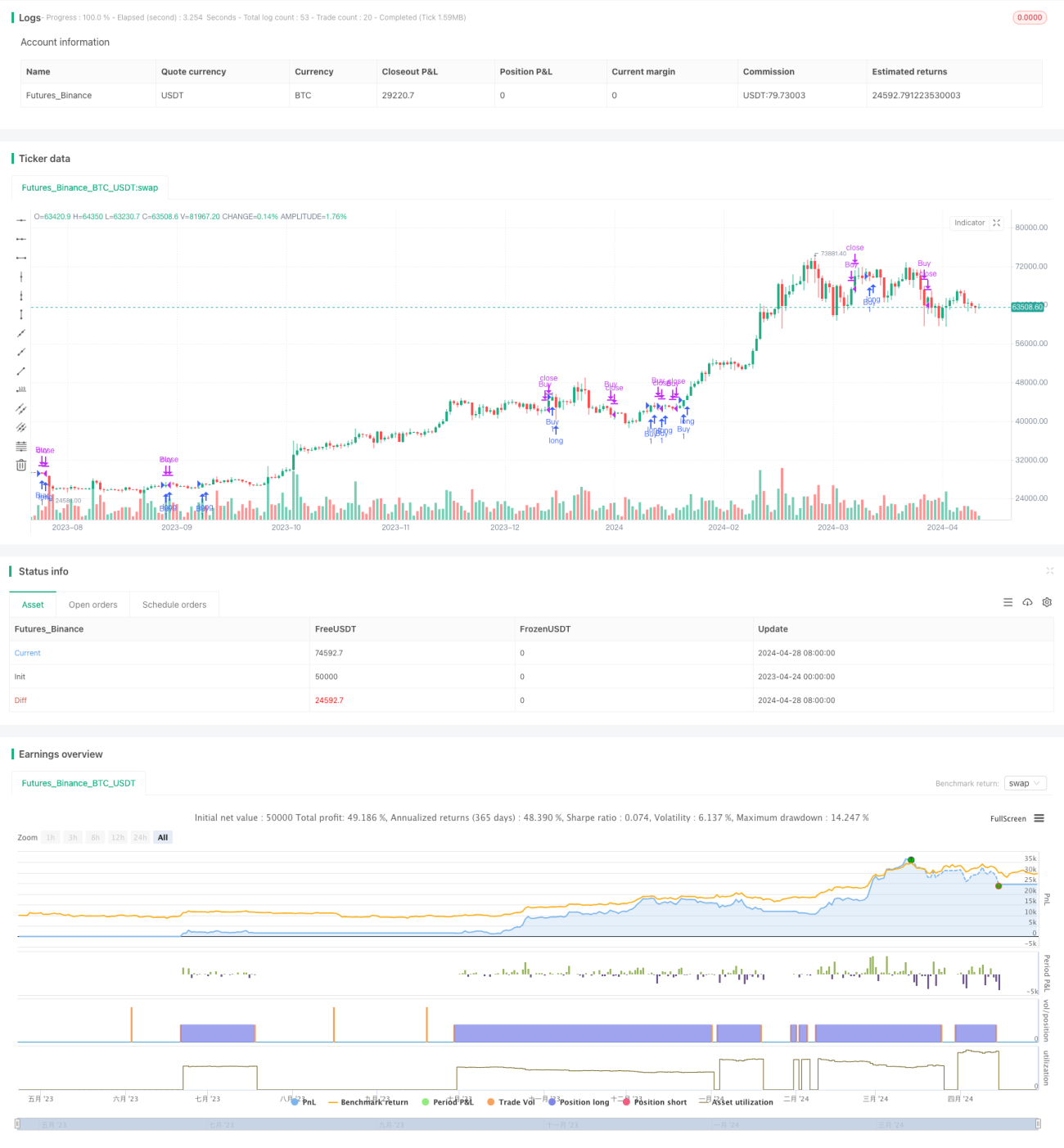

Die „MACD RSI Ichimoku Momentum-Trend-Long-Strategie“ ist eine quantitative Handelsstrategie, die MACD, RSI und Ichimoku-Indikatoren kombiniert. Durch die Analyse der Signale von MACD, RSI und der Ichimoku-Wolke erfasst die Strategie Markttrends und -dynamik, um Trends zu verfolgen und günstige Ein- und Ausstiegszeitpunkte zu bestimmen. Die Strategie ermöglicht flexible Einstellungen für Indikatorparameter und Handelszeiträume und eignet sich für verschiedene Handelsstile und Märkte.

Strategieprinzip

Der Kern der Strategie ist die kombinierte Nutzung von MACD, RSI und Ichimoku-Indikatoren:

- MACD setzt sich aus der Differenz zwischen einem schnellen und einem langsamen gleitenden Durchschnitt zusammen und dient zur Bestimmung der Trendrichtung und der Dynamikänderungen. Wenn die schnelle MACD-Linie die langsame Linie von unten kreuzt, wird ein Kaufsignal generiert; bei einem Kreuz von oben nach unten entsteht ein Verkaufssignal.

- RSI misst das Ausmaß der Kurssteigerungen und -rückgänge innerhalb eines bestimmten Zeitraums und zeigt überkaufte oder überverkaufte Zustände an. Liegt der RSI unter 30, könnte der Markt überverkauft sein; über 70 deutet auf Überkauftheit hin.

- Ichimoku-Wolke besteht aus der Tenkan-Sen, Kijun-Sen, Senkou Span A und Senkou Span B und liefert Informationen zu Unterstützung, Widerstand und Trendstärke.

Die Strategie eröffnet eine Long-Position, wenn der MACD bullisch ist, der Kurs über der Wolke liegt und der RSI nicht überkauft ist. Die Position wird geschlossen, wenn der MACD bärisch wird (Kreuz nach unten) oder der Kurs unter die Wolke fällt.

Strategievorteile

- Mehrere Indikatoren zur Bestätigung: Erhöht die Genauigkeit der Trendbewertung. MACD erfasst die Trendrichtung, RSI hilft bei der Timing-Wahl, und Ichimoku bietet eine umfassendere Marktübersicht, was die Zuverlässigkeit der Strategie erhöht.

- Flexible Parameter: Die Einstellungen von MACD, RSI und Ichimoku können an verschiedene Handelsstile und Marktbedingungen angepasst werden.

- Risikomanagement: Stop-Loss und Take-Profit begrenzen Verluste; schrittweiser Positionsaufbau reduziert das Einstiegsrisiko.

- Breite Anwendbarkeit: Einsetzbar in verschiedenen Märkten und für verschiedene Instrumente, um verschiedene Trendchancen zu nutzen.

Strategierisiken

- Widersprüchliche Indikatorsignale: MACD, RSI und Ichimoku können gelegentlich gegensätzliche Signale liefern, was zu Fehlentscheidungen führen kann.

- Ungeeignete Parametereinstellungen: Falsche Parameter können die Funktionsfähigkeit der Strategie beeinträchtigen; eine Optimierung basierend auf Markteigenschaften und Backtesting ist erforderlich.

- Schlechte Performance in Seitwärtsmärkten: Trendstrategien neigen in Seitwärtsmärkten zu häufigen Trades, wobei hohe Transaktionskosten die Gewinne schmälern können.

- Risiko unerwarteter Ereignisse: Bestimmte Ereignisse können zu abnormalen Kursbewegungen führen, die den Indikatorsignalen widersprechen.

Optimierungsansätze

- Verstärkte Trendbestätigung: Zusätzliche Bedingungen wie anhaltender Kursanstieg innerhalb der Wolke oder MACD-Divergenzen können die Eröffnungsqualität verbessern.

- Integration von Stop-Loss, Take-Profit und Positionsmanagement: Zur Begrenzung von Verlusten und Verbesserung des Risiko-Ertrags-Verhältnisses.

- Parameteroptimierung: Anpassung an verschiedene Instrumente und Zeitrahmen zur Steigerung der Robustheit.

- Trailing-Stop: Nutzung eines nachlaufenden Stopps, um Gewinne zu sichern und Vorteile auszubauen.

Zusammenfassung

Die „MACD RSI Ichimoku Momentum-Trend-Long-Strategie“ ist eine leistungsstarke quantitative Handelsstrategie, die MACD, RSI und Ichimoku-Indikatoren kombiniert, um Trends und Dynamiken umfassend zu bewerten. In trendstarken Märkten zeigt sie eine gute Fähigkeit, Trends zu erfassen und das Timing zu steuern. Durch Parameteroptimierung und Risikomanagementmaßnahmen kann diese Strategie ein wirksames Werkzeug sein, um Marktchancen zu nutzen und stabile Renditen zu erzielen.

- 1