HanYue – Auf mehreren EMA, ATR und RSI basierende Trendfolge-Strategie

Überblick

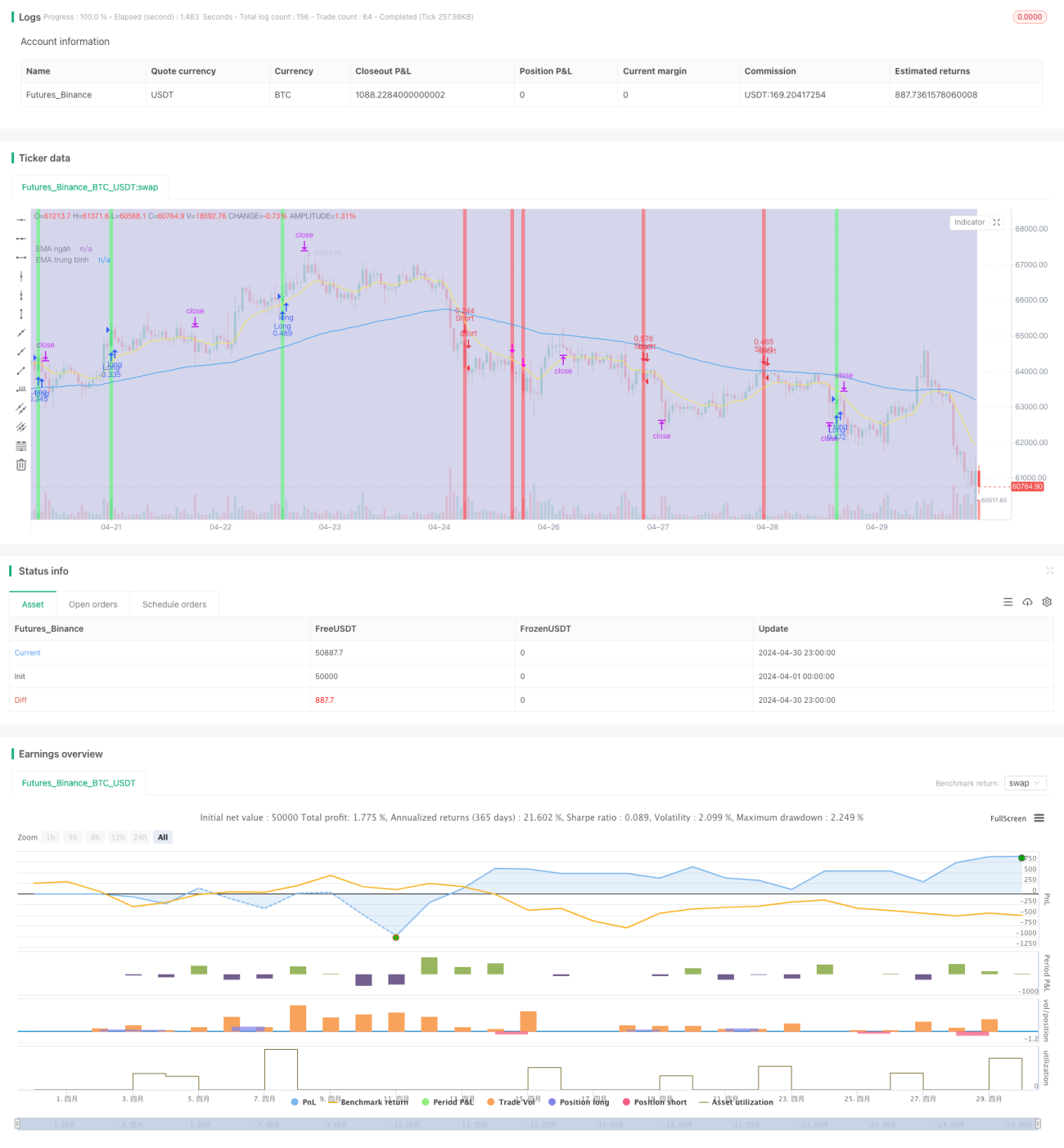

Diese Strategie verwendet drei exponentielle gleitende Durchschnitte (EMA) mit unterschiedlichen Perioden, um den Markttrend zu bestimmen, und kombiniert den Relative-Stärke-Index (RSI) und den Average True Range (ATR), um Einstiegspunkte sowie Stop-Loss- und Take-Profit-Niveaus zu ermitteln. Wenn der Preis den von den drei EMAs gebildeten Kanal durchbricht und gleichzeitig der RSI seinen gleitenden Mittelwert übersteigt, wird ein Eröffnungssignal ausgelöst. Gleichzeitig wird der ATR verwendet, um die Positionsgröße zu steuern und Stop-Loss-Niveaus festzulegen, während das Risiko-Ertrags-Verhältnis (RR) zur Bestimmung des Take-Profit-Niveaus dient. Der Hauptvorteil dieser Strategie liegt in ihrer Einfachheit und Effektivität, da sie Trends folgt und durch strenge Risikokontrollmaßnahmen potenzielle Verluste begrenzt.

Strategieprinzip

- Berechnung von drei EMAs mit unterschiedlichen Perioden (kurz-, mittel- und langfristig), um den Gesamttrend des Marktes zu bestimmen.

- Verwendung des RSI-Indikators zur Bestätigung der Trendstärke und -nachhaltigkeit; ein Überschreiten des gleitenden Mittelwerts des RSI signalisiert eine Trendänderung.

- Kombination des Verhältnisses zwischen Preis und EMA-Kanal mit dem RSI-Signal zur Generierung von Eröffnungssignalen: Wenn der Preis den EMA-Kanal durchbricht und der RSI ebenfalls seinen gleitenden Mittelwert übersteigt, wird in Trendrichtung eröffnet.

- Nutzung des ATR zur Bestimmung der Positionsgröße und des Stop-Loss-Niveaus, um das Risiko pro Trade zu kontrollieren.

- Festlegung des Take-Profit-Niveaus basierend auf einem vorgegebenen Risiko-Ertrags-Verhältnis (z. B. 1,5:1), um die Rentabilität der Strategie sicherzustellen.

Vorteilsanalyse

- Einfach und effektiv: Die Strategie verwendet nur einige gängige technische Indikatoren, die Logik ist klar und leicht verständlich sowie umsetzbar.

- Trendfolge: Durch die Kombination von EMA-Kanal und RSI kann die Strategie dem Markttrend folgen und größere Preisbewegungen einfangen.

- Risikokontrolle: Die Verwendung des ATR zur Festlegung von Stop-Loss-Niveaus und zur Steuerung der Positionsgröße begrenzt das Risiko pro Trade effektiv.

- Flexibilität: Die Parameter der Strategie (wie EMA-Perioden, RSI-Periode, ATR-Multiplikator usw.) können je nach Markt und Handelsstil angepasst werden, um die Leistung zu optimieren.

Risikoanalyse

- Parameteroptimierung: Die Performance der Strategie hängt stark von der Wahl der Parameter ab; ungeeignete Parametereinstellungen können zu Fehlfunktionen oder schlechter Performance führen.

- Marktrisiko: Bei unerwarteten Ereignissen oder extremen Marktbedingungen kann die Strategie erhebliche Verluste erleiden, insbesondere bei Trendumkehrungen oder Seitwärtsbewegungen.

- Überanpassung: Eine übermäßige Anpassung der Parameter an historische Daten kann dazu führen, dass die Strategie im Live-Handel schlecht abschneidet.

Optimierungsmöglichkeiten

- Dynamische Parameter: Anpassung der Strategieparameter an sich ändernde Marktbedingungen, z. B. längere EMA-Perioden bei starken Trends und kürzere Perioden in Seitwärtsmärkten.

- Kombination mit anderen Indikatoren: Einführung weiterer technischer Indikatoren (wie Bollinger-Bänder, MACD usw.), um die Zuverlässigkeit und Genauigkeit der Eröffnungssignale zu erhöhen.

- Einbeziehung der Marktstimmung: Kombination mit Stimmungsindikatoren (wie dem Angst-Gier-Index), um das Risiko und die Positionsverwaltung anzupassen.

- Multi-Timeframe-Analyse: Analyse von Markttrends und Signalen in verschiedenen Zeitrahmen, um eine umfassendere Marktperspektive und robustere Handelsentscheidungen zu erhalten.

Zusammenfassung

Diese Strategie baut durch die Kombination mehrerer gängiger technischer Indikatoren wie EMA, RSI und ATR ein einfaches und effektives Trendfolgesystem auf. Sie nutzt den EMA-Kanal zur Bestimmung des Markttrends, den RSI zur Bestätigung der Trendstärke und den ATR zur Risikosteuerung. Die Vorteile der Strategie liegen in ihrer Einfachheit und Anpassungsfähigkeit, da sie Trends unter verschiedenen Marktbedingungen folgen kann. Allerdings hängt die Performance stark von der Parameterwahl ab; ungeeignete Parameter können zu Fehlfunktionen oder schlechter Performance führen. Zudem kann die Strategie bei unerwarteten Ereignissen oder extremen Marktbedingungen erheblichen Risiken ausgesetzt sein. Zur weiteren Optimierung können dynamische Parameteranpassungen, die Kombination mit anderen Indikatoren, die Einbeziehung der Marktstimmung sowie Multi-Timeframe-Analysen in Betracht gezogen werden. Insgesamt bietet die Strategie eine gute Grundlage für den Trendfolgehandel, muss jedoch je nach tatsächlichen Marktbedingungen angepasst und optimiert werden.

- 1