Auf dem Average-Directional-Index-Filter basierte Moving-Average-Rejection-Strategie

Übersicht

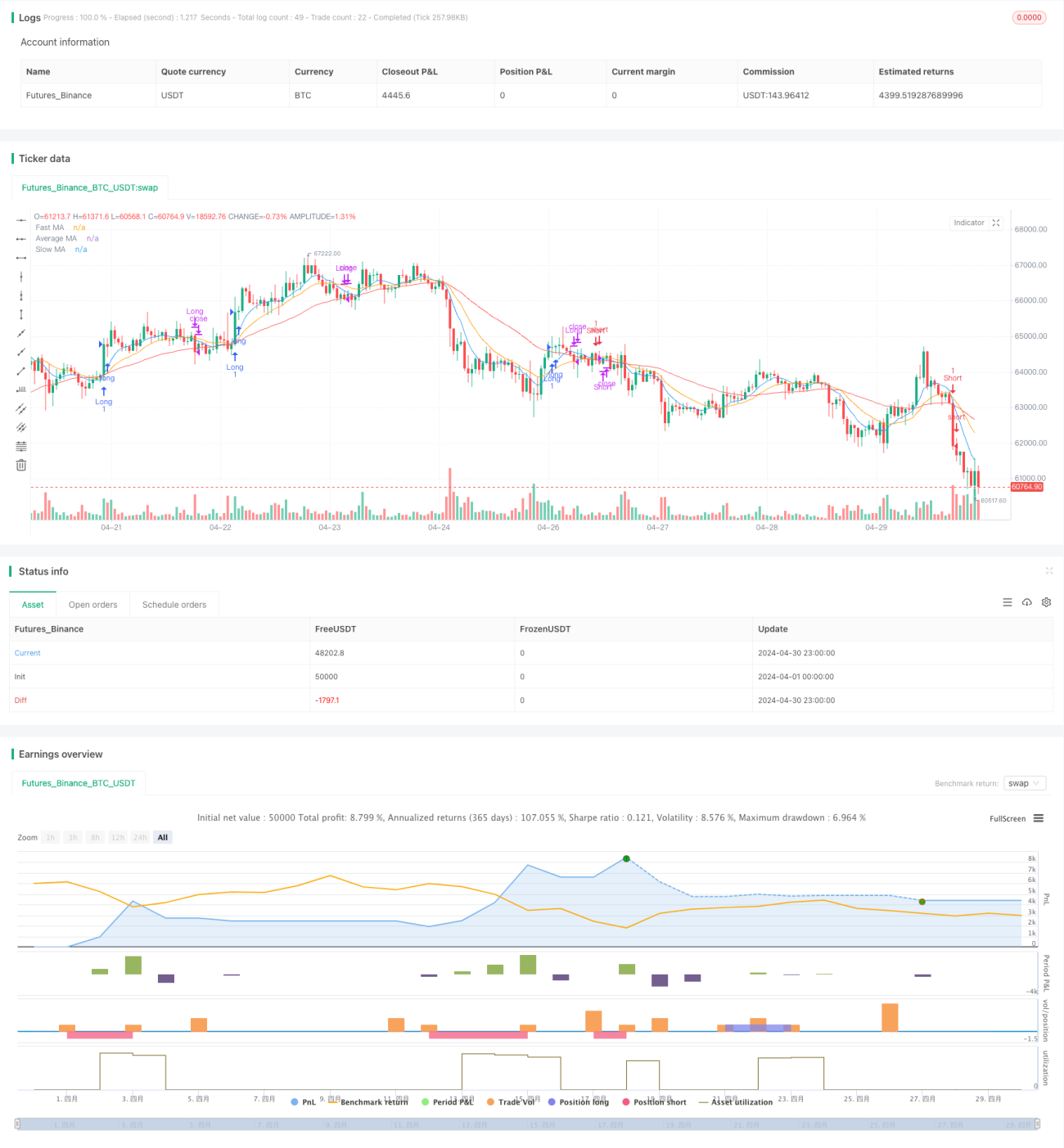

Diese Strategie verwendet mehrere gleitende Durchschnitte (MA) als primäre Handelssignale und kombiniert sie mit dem Average Directional Index (ADX) als Filter. Die Hauptidee der Strategie besteht darin, durch den Vergleich der schnellen MA, der langsamen MA und der durchschnittlichen MA potenzielle Long- und Short-Chancen zu identifizieren. Gleichzeitig wird der ADX-Indikator genutzt, um Marktumgebungen mit ausreichender Trendstärke herauszufiltern und so die Zuverlässigkeit der Handelssignale zu erhöhen.

Strategieprinzip

- Berechnung der schnellen MA, langsamen MA und durchschnittlichen MA.

- Identifizierung potenzieller Long- und Short-Niveaus durch Vergleich des Schlusskurses mit der langsamen MA.

- Bestätigung der Long- und Short-Niveaus durch Vergleich des Schlusskurses mit der schnellen MA.

- Manuelle Berechnung des ADX-Indikators zur Messung der Trendstärke.

- Wenn die schnelle MA die durchschnittliche MA von unten nach oben kreuzt, der ADX über dem festgelegten Schwellenwert liegt und das Long-Niveau bestätigt ist, wird ein Long-Einstiegssignal generiert.

- Wenn die schnelle MA die durchschnittliche MA von oben nach unten kreuzt, der ADX über dem festgelegten Schwellenwert liegt und das Short-Niveau bestätigt ist, wird ein Short-Einstiegssignal generiert.

- Wenn der Schlusskurs die langsame MA von oben nach unten kreuzt, wird ein Long-Ausstiegssignal generiert; wenn der Schlusskurs die langsame MA von unten nach oben kreuzt, wird ein Short-Ausstiegssignal generiert.

Strategievorteile

- Die Verwendung mehrerer MAs ermöglicht eine umfassendere Erfassung von Markttrend- und Momentumänderungen.

- Durch den Vergleich der schnellen MA, langsamen MA und durchschnittlichen MA können potenzielle Handelsmöglichkeiten identifiziert werden.

- Der Einsatz des ADX-Indikators als Filter hilft, übermäßige Fehlsignale in Seitwärtsmärkten zu vermeiden und erhöht die Zuverlässigkeit der Handelssignale.

- Die Strategielogik ist klar, leicht verständlich und umsetzbar.

Strategierisiken

- In wenig ausgeprägten Trends oder bei Seitwärtsbewegungen kann die Strategie viele Fehlsignale erzeugen, was zu häufigen Trades und Verlusten führt.

- Die Strategie ist auf nachlaufende Indikatoren wie MA und ADX angewiesen, wodurch frühe Trendbildungen möglicherweise verpasst werden.

- Die Parametereinstellungen (z. B. MA-Längen und ADX-Schwellenwert) haben erheblichen Einfluss auf die Strategieleistung und müssen je nach Markt und Instrument optimiert werden.

Optimierungsmöglichkeiten

- Einführung weiterer technischer Indikatoren wie RSI, MACD usw., um die Zuverlässigkeit und Vielfalt der Handelssignale zu erhöhen.

- Für verschiedene Marktumgebungen können unterschiedliche Parameterkombinationen festgelegt werden, um sich an Marktveränderungen anzupassen.

- Einführung von Risikomanagementmaßnahmen wie Stop-Loss und Positionsgrößenmanagement zur Begrenzung potenzieller Verluste.

- Kombination mit fundamentaler Analyse, z. B. Wirtschaftsdaten und politischen Änderungen, um eine umfassendere Marktperspektive zu erhalten.

Zusammenfassung

Die auf dem Average Directional Index-Filter basierende Gleitender-Durchschnitt-Ablehnungsstrategie nutzt mehrere MAs und den ADX-Indikator, um potenzielle Handelsmöglichkeiten zu identifizieren und minderwertige Signale auszufiltern. Die Strategielogik ist klar, leicht verständlich und umsetzbar, doch in der praktischen Anwendung müssen Marktveränderungen beachtet und die Strategie durch weitere technische Indikatoren und Risikomanagementmaßnahmen optimiert werden.

- 1